The stock market’s in love with small, weaker companies. The credit market still detests them.

Give me your tired, your poor, your huddled masses...unless we’re talking about corporate bonds.

The July 11 CPI report showing a welcome cooling in US inflation unlocked a major shift in market leadership, where the baton was flung from megacap tech to small-cap stocks.

The basic thinking underpinning strength in smalls is simple: if inflation has slowed enough so the Federal Reserve doesn’t have to keep trying to slow the economy with higher interest rates, the weaker, smaller companies that were most in danger of being victims of the central bank’s quest to help bring supply and demand into better alignment get a reprieve.

There is, of course, more to it than that. As Apollo chief economist Torsten Slok flagged, about half the debt owed by non-financial companies in the Russell 2000 Index of small-cap stocks is floating rate — so those firms will be paying less interest on those obligations as the Federal Reserve lowers its policy rate.

The best performing “factor” in the equity market over the past couple of weeks has been volatility — the more your stock tends to gyrate, the better it’s done over the past couple of weeks. For shorthand, even Cathie Wood’s ARKK ETF — a speculative, tech-centric investment vehicle if there ever was one — is up almost 4% since the last CPI report, while the S&P 500 (led by megacap tech) is down about 1.5%.

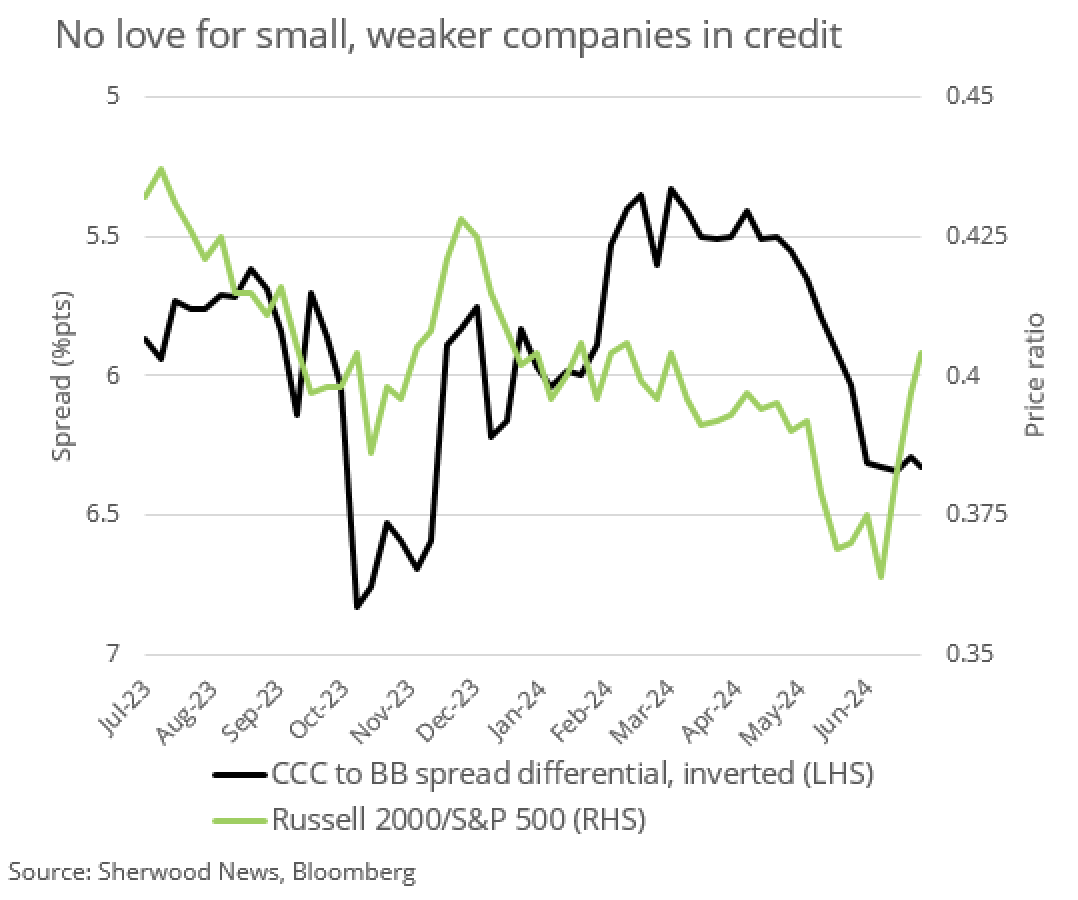

A preference for small over large, weak over strong, and speculative over secure is what we’ve been seeing in the stock market. But we haven’t seen it in the credit market.

The spread between the interest rates on bonds rated CCC by credit agencies (the junkiest of junk bonds) versus BB (the cleanest dirty shirts in the high-yield space) remains very elevated despite a record outperformance of small versus large companies in the equity market.

“But somewhat surprisingly, the bid for ‘low quality’ in credit has remained weak, with CCC-rated bonds moving roughly in line with their beta to the broader index, which has kept their historically wide valuation gap largely in place,” wrote a team of Goldman Sachs analysts led by Lofti Karoui in a note to clients last week.

While CCC’s capital structures are by no means monolithic, in this case, too, half of the companies have both bonds (where their interest payments won’t reprice immediately) and loans (where they will benefit from Federal Reserve easing), according to analysts at Goldman Sachs.

“The main takeaway from this exercise is that the upcoming Fed cuts will likely provide relief to some parts of the CCC bond universe,” they conclude. This doesn’t leave Goldman’s team banging the table on a big catch-up trade in CCCs, however. They maintain a neutral rating on that segment of the market and say that “good” CCCs will eventually catch a bid.

Even though the credit quality of the Russell 2000 isn’t as low as CCC in aggregate, the fact that even micro-caps (think small caps, but even smaller) have outperformed small caps since June 10 makes the lackluster response in the weakest credits all the more head-scratching.

I guess there’s always some companies that bankers and investors loaned money to that are inevitably going to suck no matter how good the economy is, or might become.