Stocks really ain’t cheap

We’ve said it before, and we’ll say it again. The stock market’s post-election romp is increasingly untethered to investing fundamentals, as the gambling impulse — always present in the Jekyll-and-Hyde nature of trading markets — is clearly in control.

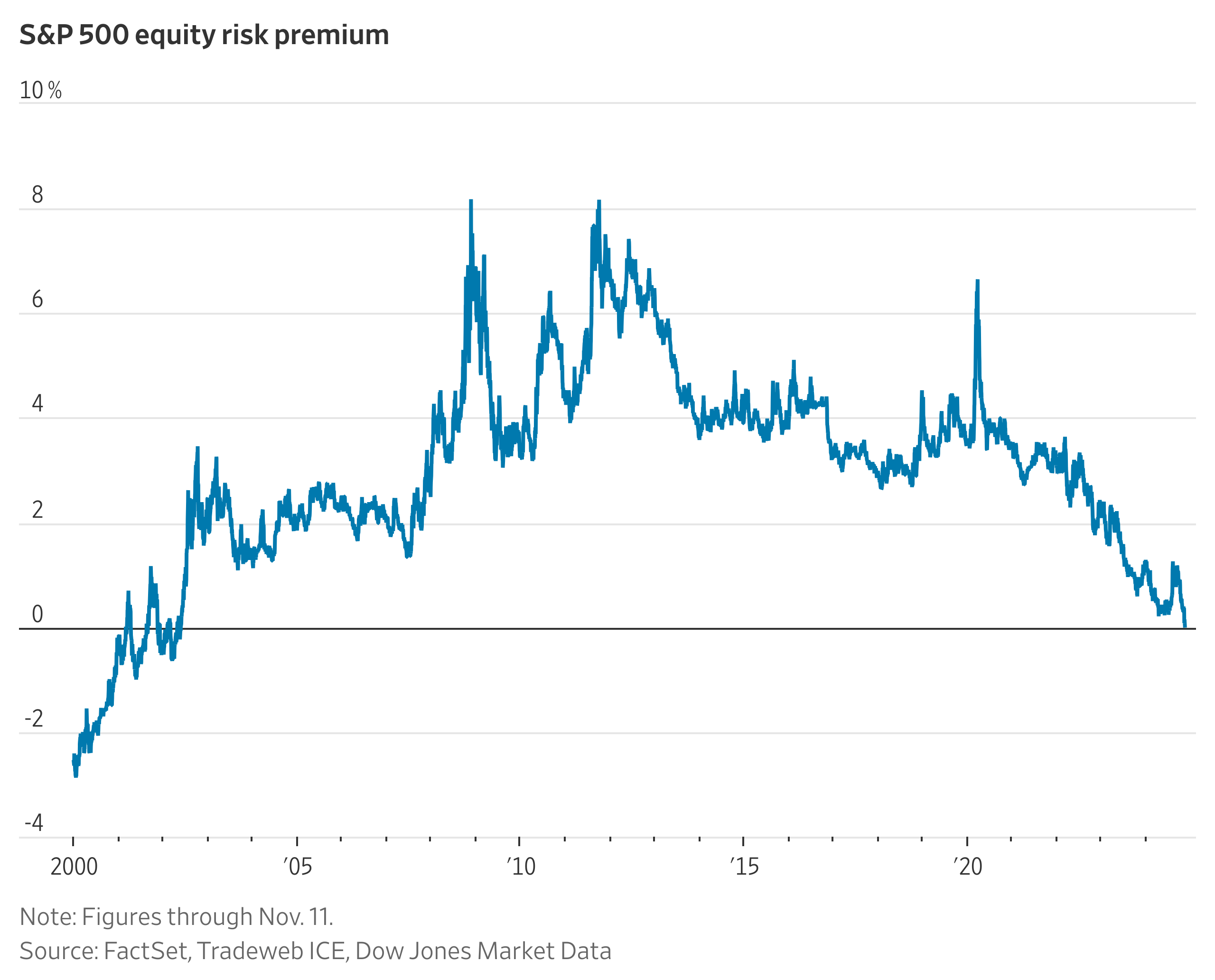

The WSJ spotlights the skimpy cushion expected earnings for the S&P 500 now provide, versus the guaranteed yields of US government bonds, as evidence that this rally is getting a bit unreasonable.

This so-called equity-risk premium shows that those buying the stock market are getting compensated virtually nothing for the risk they’re taking on at the moment, at least in terms of expected earnings.

A couple caveats here: first off, the post-election rise in stocks and bond yields at least partially reflects more optimism on the growth outlook. Sell-side analysts are never as nimble in adjusting their earnings estimates for companies as the stock and bond markets are in adjusting prices. So, expected profits are likely to see a boost as Wall Street plays catch-up.

Also, anchoring to the past 20 years — and especially the period following the global financial crisis — as a good gauge of what the ERP “should” be is difficult. That’s a period in which bond yields were very low relative to nominal economic growth; that is, stocks were a pretty good deal.

Of course, stock prices can — and, especially recently, have — run far ahead of those expected earnings. On an individual level stock level, this is pretty clear. Some of the year’s big winners like Palantir, Nvidia or CrowdStrike look insanely overvalued according metrics like price-to-sales ratios.

And that’s why the market is on track for its best two-year run since the dot-com boom of the 1990s, ERP be damned.

This so-called equity-risk premium shows that those buying the stock market are getting compensated virtually nothing for the risk they’re taking on at the moment, at least in terms of expected earnings.

A couple caveats here: first off, the post-election rise in stocks and bond yields at least partially reflects more optimism on the growth outlook. Sell-side analysts are never as nimble in adjusting their earnings estimates for companies as the stock and bond markets are in adjusting prices. So, expected profits are likely to see a boost as Wall Street plays catch-up.

Also, anchoring to the past 20 years — and especially the period following the global financial crisis — as a good gauge of what the ERP “should” be is difficult. That’s a period in which bond yields were very low relative to nominal economic growth; that is, stocks were a pretty good deal.

Of course, stock prices can — and, especially recently, have — run far ahead of those expected earnings. On an individual level stock level, this is pretty clear. Some of the year’s big winners like Palantir, Nvidia or CrowdStrike look insanely overvalued according metrics like price-to-sales ratios.

And that’s why the market is on track for its best two-year run since the dot-com boom of the 1990s, ERP be damned.