Spotify soars as Q4 monthly average user growth and gross margins set records

Music streamer — and soon to be physical book seller — Spotify reported impressive Q4 results on Tuesday that are sending shares up 15% in premarket trading.

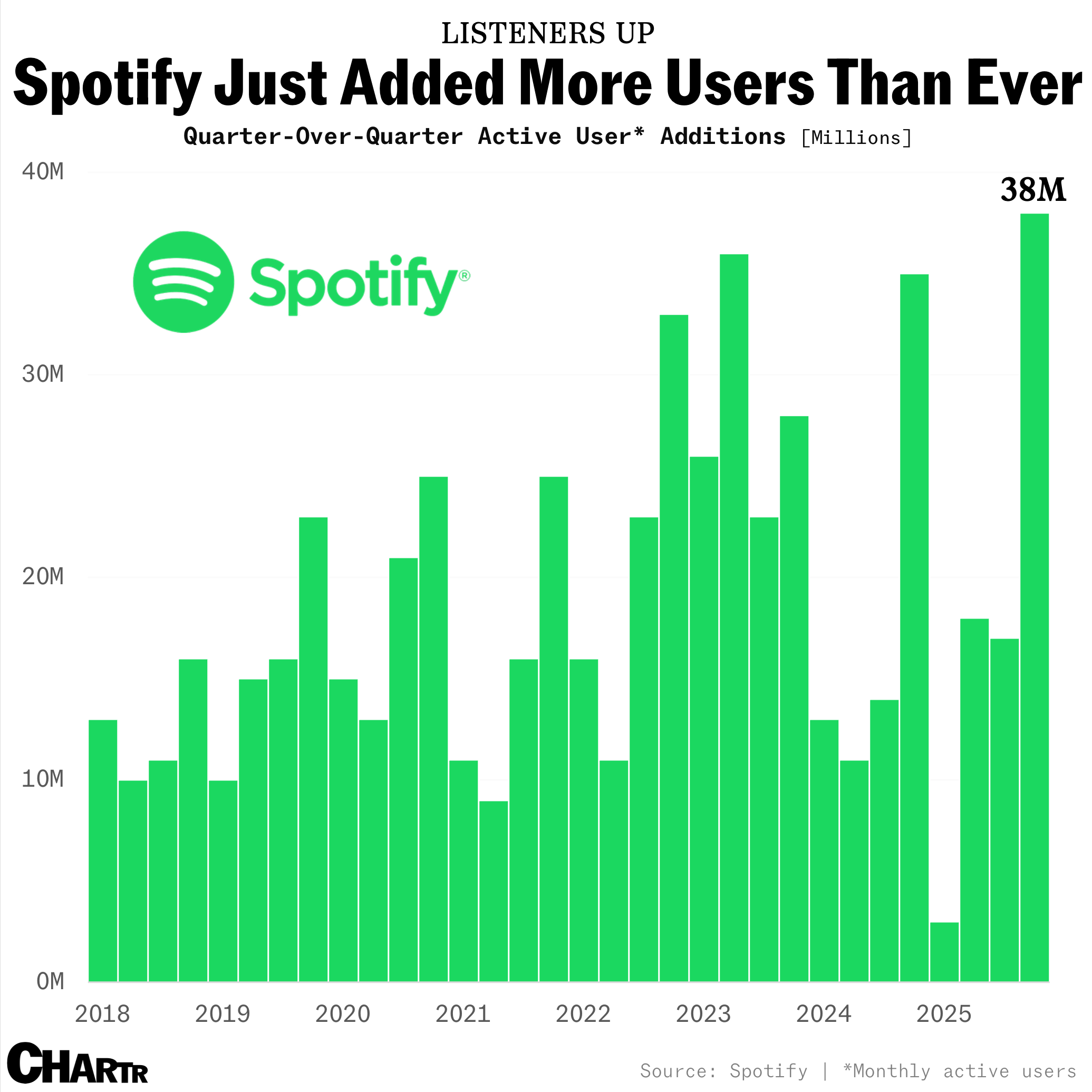

Spotify said it added more than 38 million monthly active users, a quarterly record that brought its total to 751 million. Wall Street analysts polled by FactSet expected 744.7 million. The number of premium, paying subscribers grew 10% to 290 million, slightly better than estimates of 289.4 million. Revenue for the quarter rose 7% to €4.53 billion (~$5.4 billion), which fell broadly in line with estimates, while its 33.1% gross margin figure was also a new company record.

Looking ahead to the current quarter, Spotify forecast an addition of 8 million net monthly active users for a 759 million total (vs. the 752.7 million expected). The streamer guided for 293 million premium subscribers in Q1, compared to the 293.5 million consensus estimate.

The company, which raised its US subscription prices this month, expects to book €4.5 billion, or $5.36 billion, in Q1 revenues. Wall Street expected €4.58 billion, or $5.41 billion.

With the global population sitting at just over 8 billion per the latest estimates, Spotify’s new figures imply that roughly 1 in 11 people now uses the streamer each month.