Stocks that have gone up keep going up, as momentum rolls higher and value stocks get crushed

What goes up, must go... up? Go-go stocks are having a September to remember — but momentum reversals can be sharp and sudden.

Of all the potential reasons to form an investment idea, none is simpler than the core tenet behind momentum: stocks that have gone up tend to keep going up.

It is, perhaps, the most beautiful of all investing strategies. Beloved by everyday retail traders and some of the most complicated quantitative investing firms on the planet — the type that only employ physics Ph.D.s — momentum was an intuitive idea that became a statistical curiosity when the phenomenon was first posited in academic literature in the 1990s, and it’s been blowing up portfolios, and making others rich, ever since.

And it is having an incredible year so far.

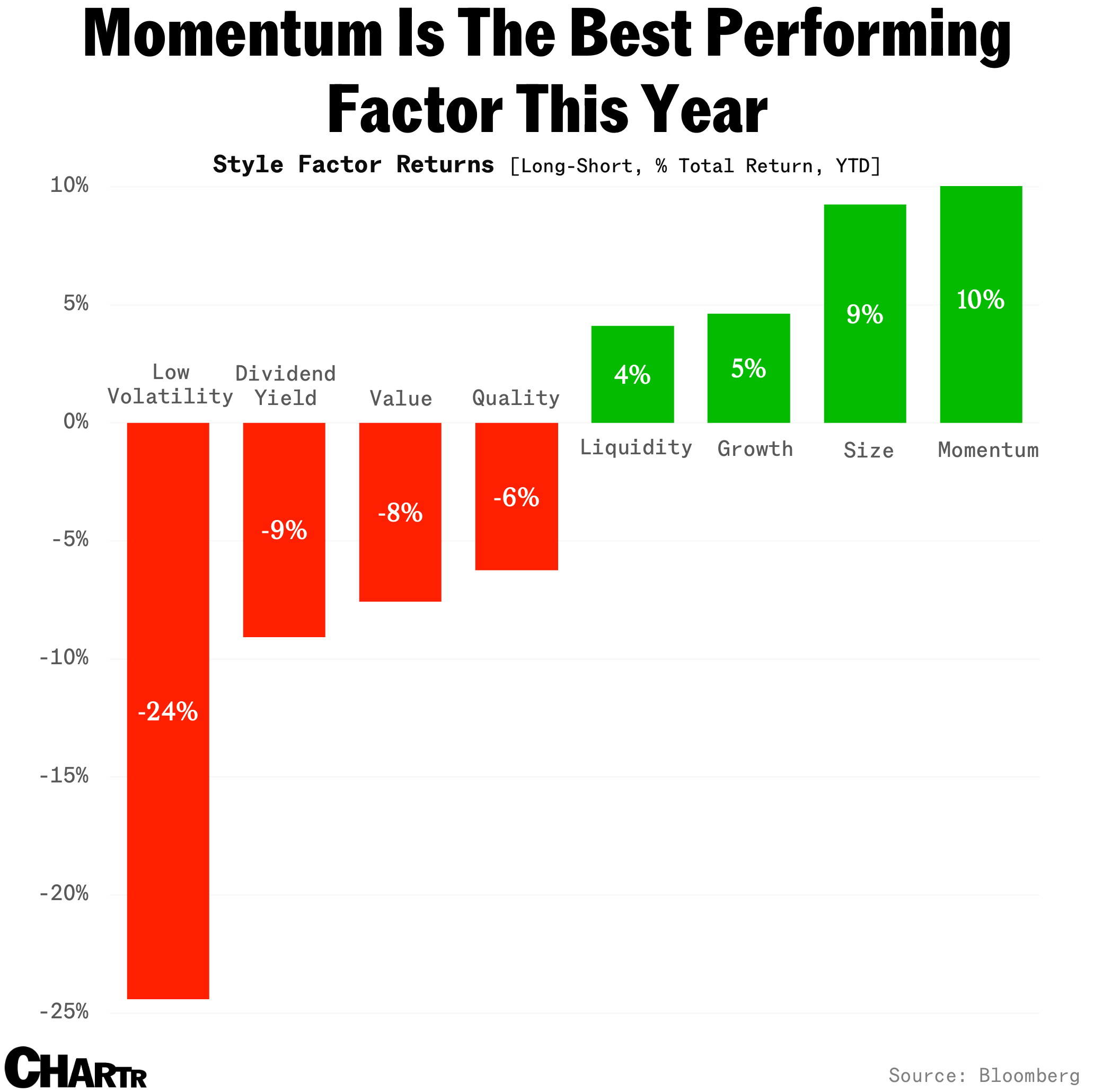

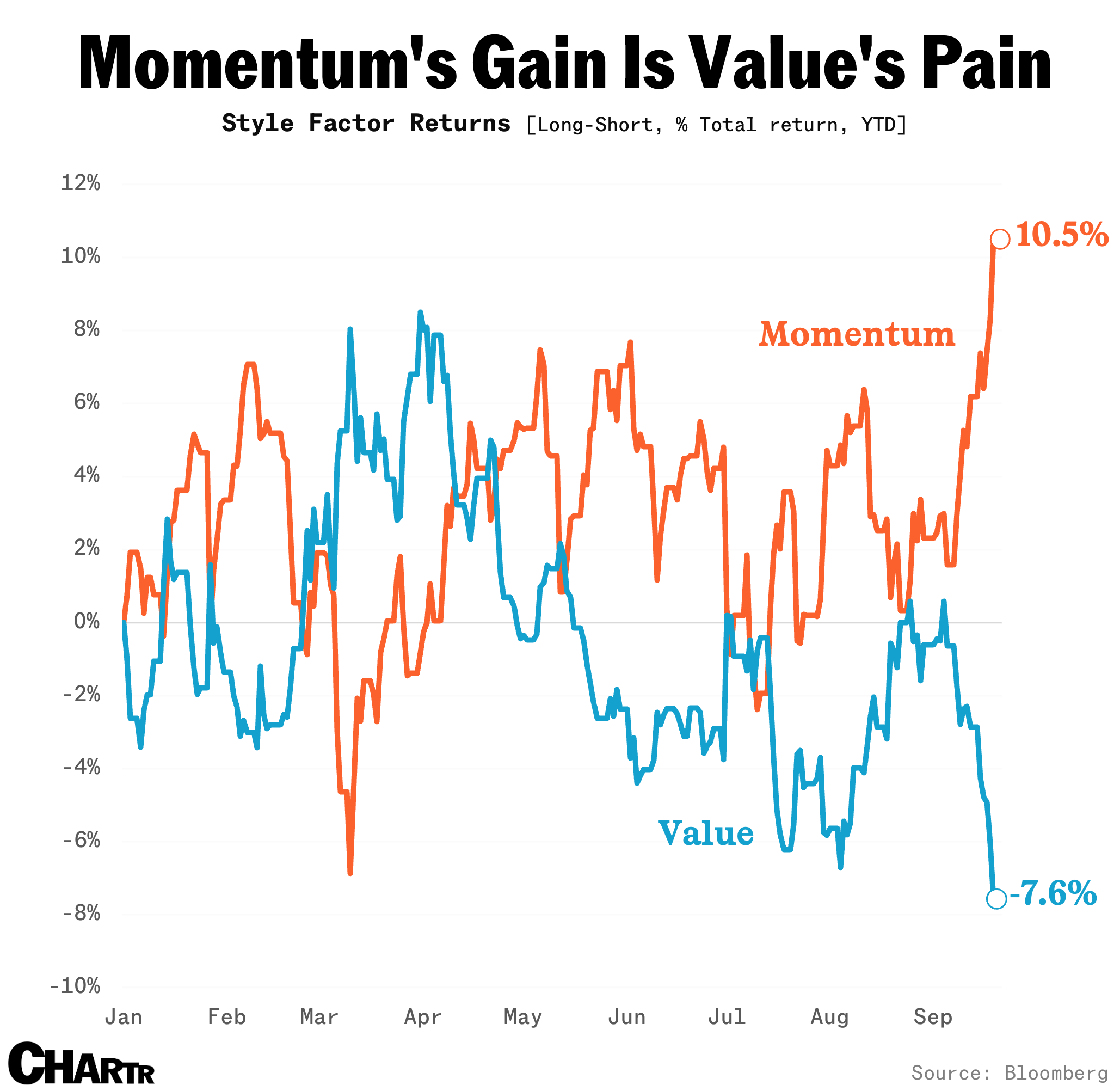

Per data from Bloomberg’s PORT MAC3 model, which tracks a swath of factors and risk premia, a long-short portfolio of US high-momentum stocks — effectively “buying” the stocks that have already gone up a lot*, while simultaneously betting against the ones that have been weaker — has gained 10.5% this year. That’s the most of any of the traditional style factors.

Though epitomized by highfliers like Palantir and Robinhood Markets, this isn’t a trend being driven by just a few stocks; the portfolio has over 300 names in the long leg and 300 names in the short leg.

(Robinhood Markets Inc. is the parent company of Sherwood Media, an independently operated media company.)

And many of those stocks have had an incredible few weeks — much to the delight of retail traders, with Sherwood News’ Luke Kawa noting on Friday that their favorite stocks are on a record 10-day winning streak.

In fact, having gained 8% in September so far, momentum is on track for its best month of gains since March 2020.

But if speculative stocks are in, it’s no surprise that boring, stable stocks are out. Indeed, “low volatility” names have been hammered this year. Even the long-favored investing style of icons like Warren Buffett and Benjamin Graham has been under pressure recently, as beaten-down, cheaper stocks have lagged sharply in September as value and momentum remain sharply negatively correlated.

At some point, those stocks will get too cheap to ignore, but right now, they’re gathering dust while the momentum carousel continues.

*The momentum definition being used here is 12-month minus one-month returns.