The three technical charts raising jitters over the AI trade

Semis head and shoulders, Nvidia below the 50-day average, and September seasonality.

A soft start to September after a poor end to August has left the most important part of the stock market — everything related to AI — in a shakier state.

A Morgan Stanley basket of AI tech beneficiaries fell 5.5% over the past two sessions, its worst two-day drubbing since the sessions immediately following “Liberation Day” on April 2, when the extent of President Donald Trump’s reciprocal tariff regime was unveiled.

With Google and Apple roaring on Wednesday, the picture is a little brighter for the AI trade. But in the background, there are still three technical spots of bother with the complex that’s been critical to the US stock market’s gains for the past two years and counting.

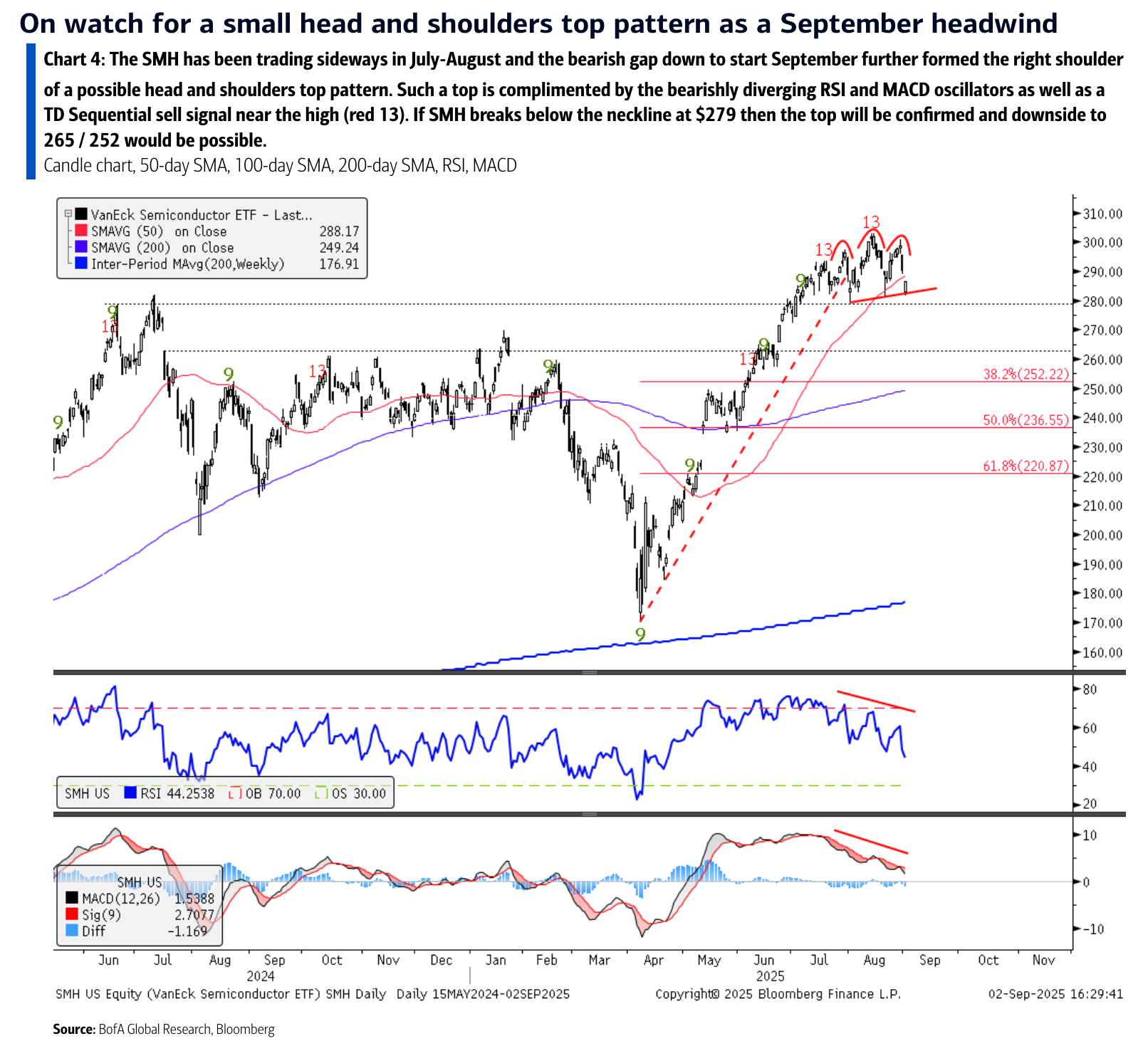

Semiconductors are in a precarious position, with the VanEck Semiconductor ETF not too far away from completing a bearish head-and-shoulders top pattern recently flagged by Bank of America head of technical research Paul Ciana.

Zooming in on the most important semiconductor stock: Nvidia, the heart, soul, and many other body parts of the AI trade, closed below its 50-day moving average on Tuesday for the first time since May, when it was repairing damage done in the wake of the momentum meltdown and tariff angst that roiled markets.

Since the AI boom unofficially kicked off in May 2023, there have been only four previous instances where Nvidia had a fresh break below its 50-day moving average (that is, closing below that level for the first time in at least 21 sessions):

August 9, 2023

April 19, 2024

July 24, 2024

December 10, 2024

And now, yesterday. The good news is that breaching that technical threshold hasn’t been a big deal for Nvidia. One-month forward returns from the above dates have been strongly positive (up at least 7%) on three of four occasions, and the one loss was less than 2%.

But oh yeah, it’s September, a seasonally bad time for the stock market. Returns have varied widely for the Nasdaq 100 over the past 20 years, from up as much as 13% to down nearly 15%, but on average it’s been the only month with negative returns for the tech-heavy gauge.

“One needs to be pragmatic while at these levels, namely because the tape is not only following the Fed Cut script closely of buying the rumor to then sell the news, but also because divergences in momentum and breadth as well elevated levels of complacency, all of which leaves the market open to a violent, yet buyable dip opportunity,” wrote John Kolovos, chief technical market strategist at Macro Risk Advisors.

That being said, he’s still constructive on the medium-term technical picture for stocks through year-end and early into 2026.