Happy CEOs versus sad Average Joes

Americans are still fairly pessimistic on the economy. Business leaders are getting more confident.

In June 2022, Kyla Scanlon coined the term “vibecession” to describe the gap between the economy — which was (and still is!) in a solid position — compared to consumer and business sentiment, which was in the toilet. According to Paul Krugman, we’re still in that vibecession.

But while that may still be true for the American public, it’s no longer true of corporate America.

Call it the K-shaped vibecovery, or Happy CEOs versus sad Average Joes:

Americans have a fairly downbeat view on the economy, but corporate executives are getting bulled up.

Last week, purchasing managers’ indexes for the US economy — which ask business leaders if conditions are getting better or worse — hit the highest level since mid-2022, when confidence was collapsing as Scanlon’s “vibecession” thesis made its debut.

“If consumer sentiment continues to struggle, corporate sentiment is actually in pretty good shape, and perhaps accelerating,” wrote Michael Purves, CEO of Tallbacken Capital, in a note to clients. “Surveys from CEOs of both large and smaller companies are showing the C-Suite is embracing the economy.”

One simple way to demonstrate this divide:

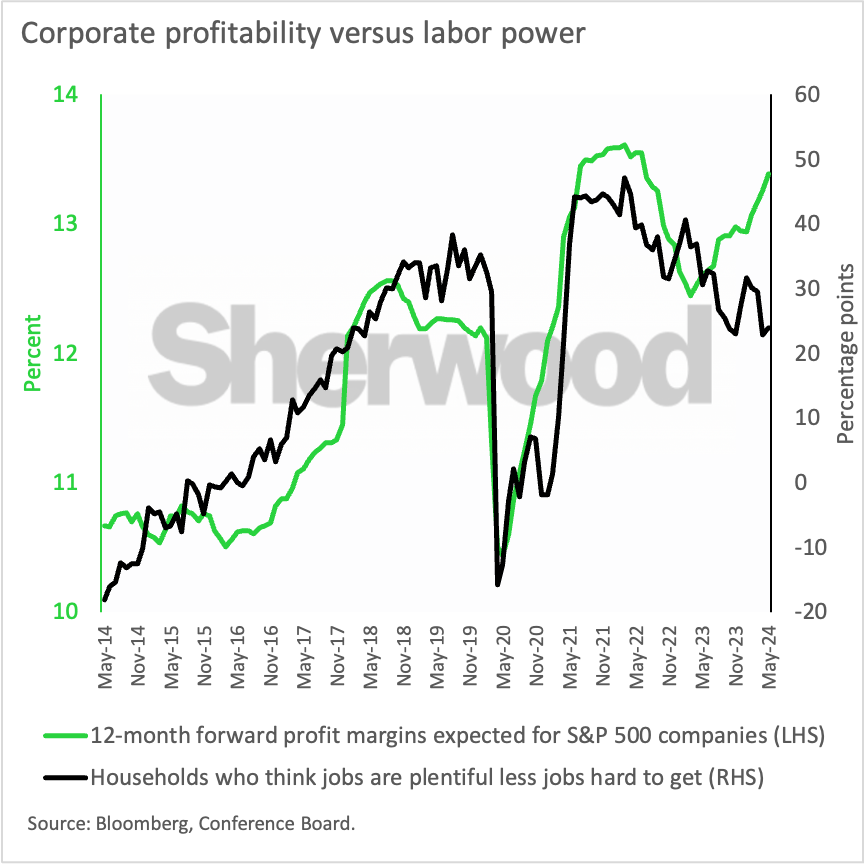

Since the middle of 2023, expectations for S&P 500 profit margins in the year ahead have been persistently revised to the upside. During that same period, the share of Americans who say jobs are “plentiful” less those who say jobs are “hard to get” has been shrinking.

Let’s set aside the question of whether it’s “right” for Americans to feel so gloomy and instead explore why businesses might be more optimistic than households.

Corporate America:

CFOs think recession risk is below average. Publicly traded companies are exceeding analysts’ earnings expectations by more than usual. Supply chains have largely un-snarled. Inventory-to-sales ratios have improved. And firms are getting rewarded for capital spending.

“Earnings growth is a three-quarter leading indicator for capex spending, and the continued strength in earnings suggests that we will see a strong rebound in business fixed investment over the coming quarters” writes Torsten Slok, chief economist at Apollo Global Management, in a note to clients.

Non-corporate America aka Average Joes:

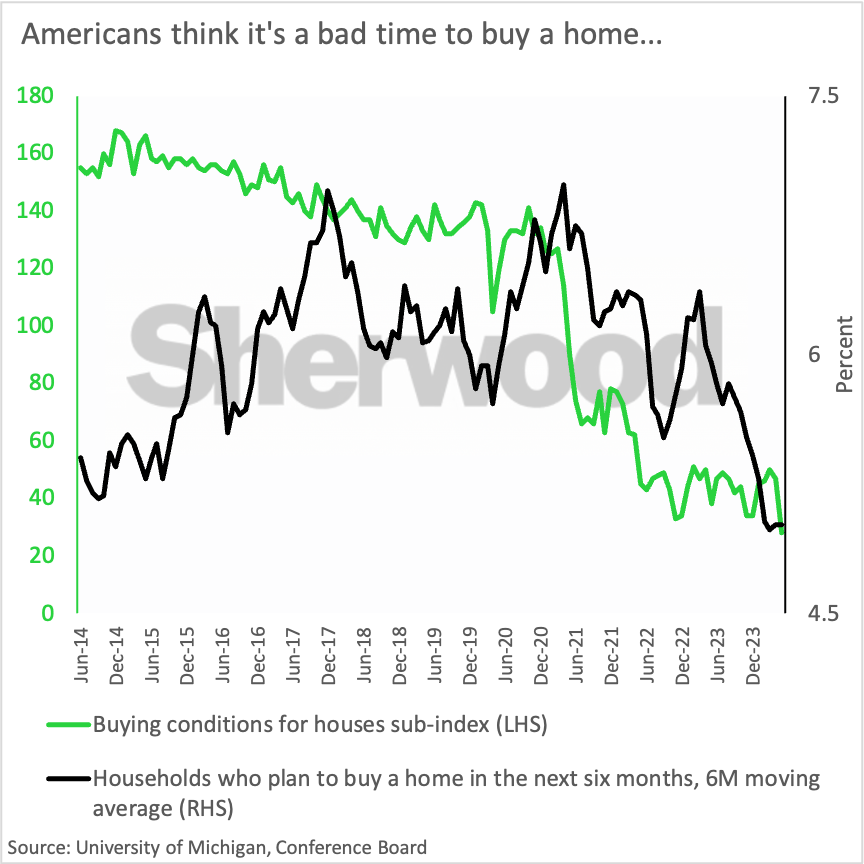

Wage growth is off the boil (in both nominal and inflation-adjusted terms). The private sector quits rate (a good leading indicator for wage growth, since a big reason to voluntarily leave your job is for higher pay) is now well below its pre-pandemic peak. Price levels throughout the economy are still high (even though inflation has decelerated meaningfully). Consumers think it’s a bad time to buy a house, and few plan to do so in the next six months.

In some respects, it seems zero sum: a couple of the reasons why consumers are a little sour are the same ones why businesses are happy. On a micro level, lower wage pressures help flatter profit margins. And a high price level — so long as it does not have an outsized negative impact on volumes sold — is also good for the bottom line.

The good news is that this better perception among businesses has the ability to improve households’ reality.

Changes in business spending are, empirically, much more volatile compared to household spending. Not to sound callous, but on a macroeconomic level, how people feel doesn’t matter — as long as it doesn’t impact their spending habits. Businesses are afforded a lot more discretion on how much they spend, what they spend on, and when to do so. So if this K-shaped vibecovery for corporate sentiment catalyzes capital spending, that typically leads to an increase in employment opportunities.

But for now, it’s no surprise that while consumers might not be too optimistic about their own income growth prospects, they are pretty confident that the stock market will keep going up!