Keep an eye on the tumbling US dollar

The dollar has slumped against the yen, and is reaching a critical inflection point versus other major currencies as well.

The eagle’s wings have been clipped.

The US dollar is sinking like a stone, with the Bloomberg Dollar Spot Index down 1% over the past three sessions and more than 3% off its late June 2024 peak.

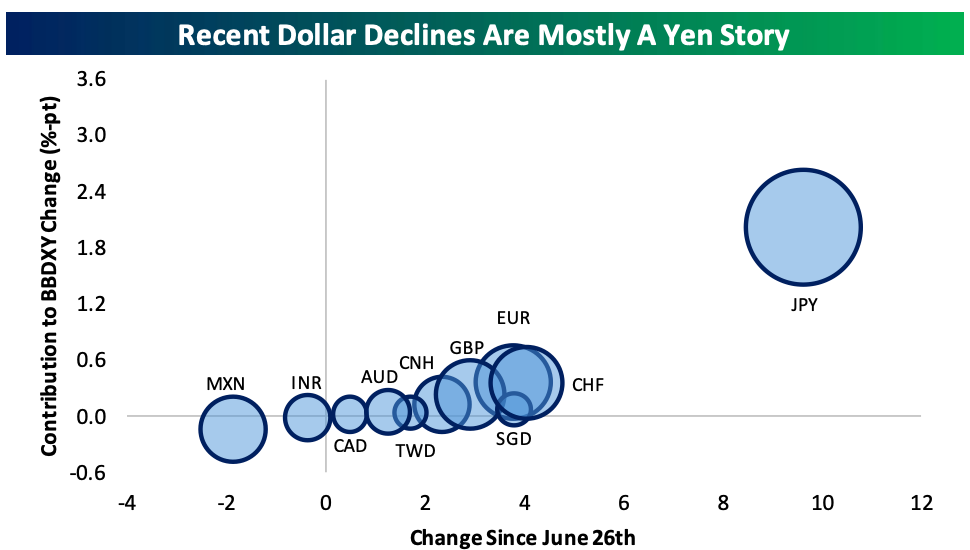

Of course, the biggest factor behind the ferocity of the USD decline in August was the unwind of the yen carry trade, which propelled the Japanese currency sharply higher.

Analysts at Bespoke Investment Group note that, through Monday, “2.0 percentage points of [the Bloomberg Spot Index’s] total drop has come from the yen, which has gained almost 10 percentage points against the dollar during its recent short squeeze.”

“All other currencies have accounted for only slightly more than 1% of the drop,” they add. “This USD decline is far less about broad dollar weakness than the yen story,”

But scan across the foreign exchange universe, and we’re reaching the point where this could transform from “yen strength” to “broad dollar weakness” – or this nascent trend could peter out.

A suite of central bank speeches at the Jackson Hole Economic Symposium this week – chiefly, Fed Chair Jerome Powell’s address on Friday, could be major currency catalysts.

An overarching reason for the greenback’s swoon has been a narrowing of interest rate differentials between the US and other major economies as expectations for Federal Reserve easing have ratcheted higher. This reduces the appeal of holding the US dollar because you’re getting less extra income from investing in short-term, safe US debt obligations compared to other nations.

Traders are currently pricing about 75% odds that the US central bank delivers a 25 basis point rate cut at its September meeting, and 25% odds of a 50 basis point reduction.

It’s highly unlikely that Powell telegraphs a big cut this week, with another round of jobs data as well as PCE and CPI inflation reports on tap before the next decision.

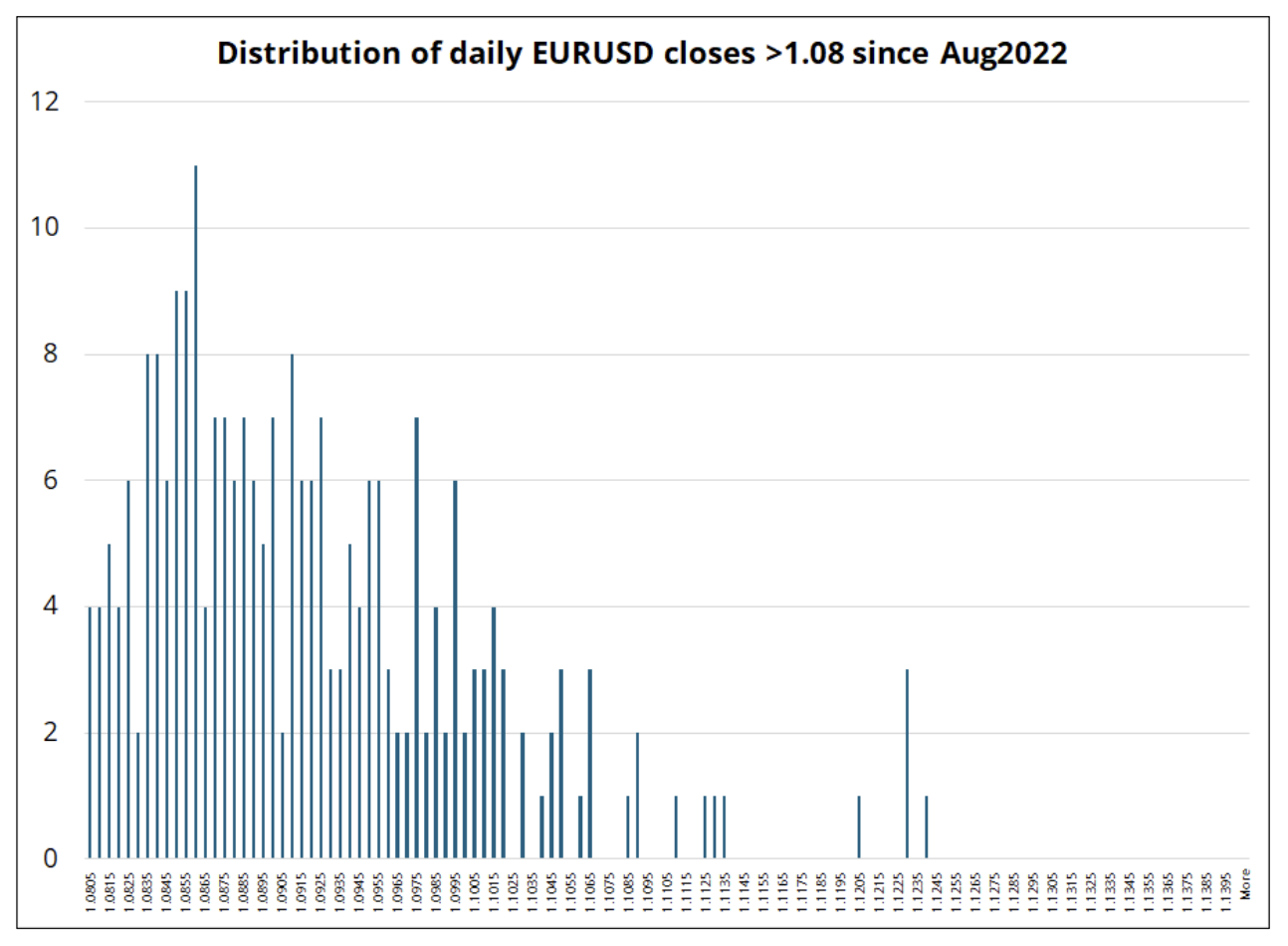

Other crosses have also moved quite a bit since the US dollar’s 2024 peak; the Swiss franc, South Korean won, and euro are all up more than 4% versus the greenback. The euro is far and away the biggest component of the Bloomberg Dollar Spot Index.

“The euro is right at a huge level as we have closed above 1.1100 just nine times in the past two years,” writes Brent Donnelly, president of Spectra Markets. “We have only closed above 1.1130 five times in the last two years. We are in rarified air.”

Not only the euro, but the currency of America’s neighbor to the north is also at an inflection point. USDCAD is closing in on 1.36, a key level where previous rallies in the Canadian dollar have fizzled out so far this year.

Donnelly flagged two made-in-Canada challenges for the currency in the near term. First, Alimentation Couche-Tard (translation: Late Night Snack) – the biggest retailer in Canada – made a bid to acquire Japanese company Seven & I Holdings (which operates 7-Eleven). Moving forward with that transaction could involve selling a lot of Canadian dollars to buy Japanese yen. Secondly, the looming rail strike in Canada would be a negative for the domestic economy in addition to disrupting North American trade.

For these reasons, he says “I would definitely not be long CAD right now (against anything)” over the next few weeks with these idiosyncratic negatives percolating in the background.