Even after the robust 1.3% gain to end the week, the US stock market is still largely a boulevard of broken charts.

If you’re looking for a segment of the market that has:

A price above its 21-day moving average (21 dma), and

A 21 dma > 50 dma > 200 dma that have all moved higher over the past month

There’s not much there.

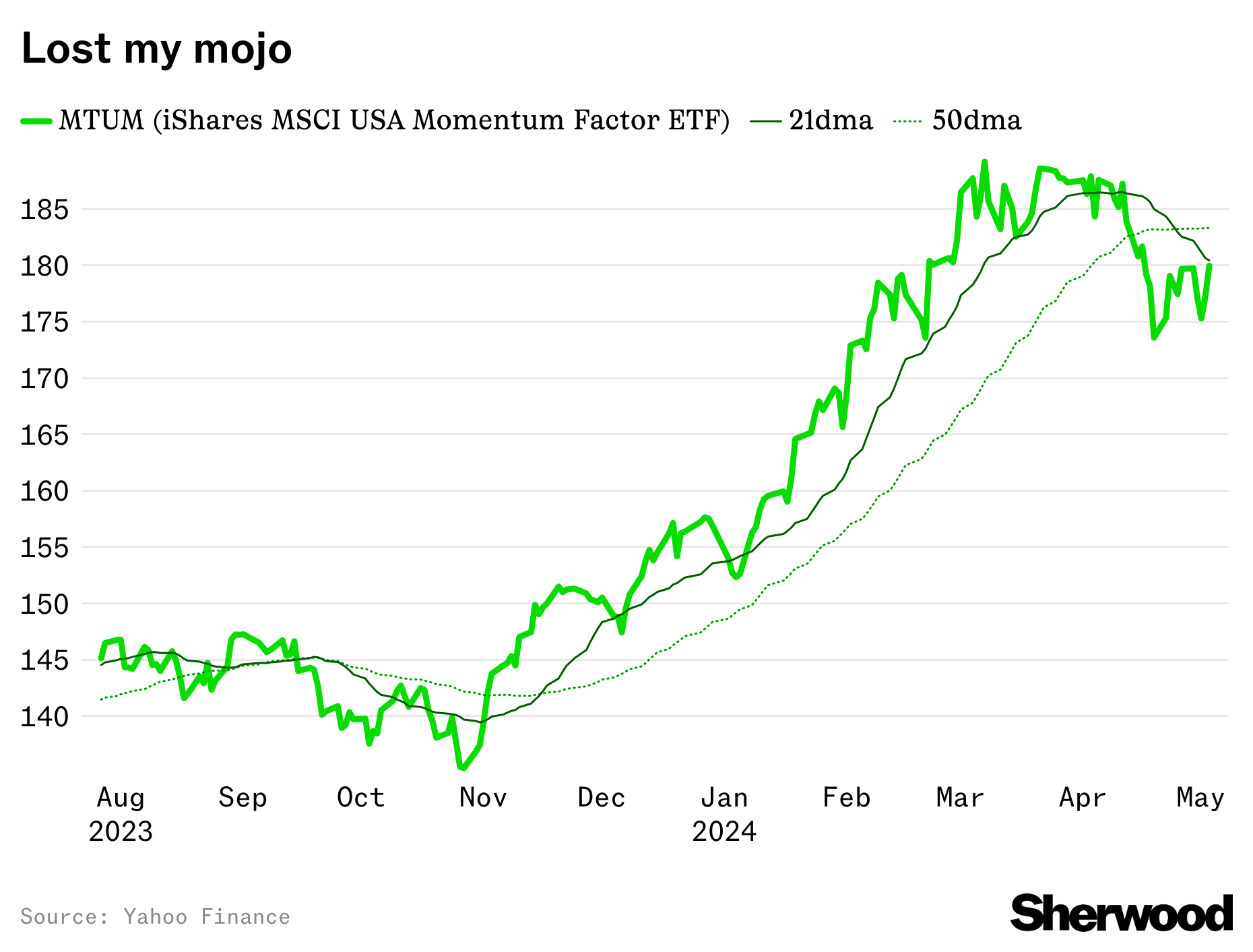

This holds for the US stock market as a whole…

That’s in stark contrast to where we stood a month ago, when the S&P 500 had closed at least 2% above its 50-day moving average for 96 consecutive sessions – the longest such stretch since 1971.

It’s a very clear and abrupt loss of momentum that’s been partially recovered, with US stocks sitting just 2.4% off record highs. The trends are far from your enemy right now, but they’re more of an acquaintance than a friend.

The good news? There’s not much evidence to suggest the pullback in US stocks had much to do with the economy or the outlook for corporate profits. So blame valuations. Or geopolitics. Or inflation. Or whatever excuse needed for profit-taking after such a historically strong run of form. (But you can’t blame the eclipse.)

Consider: Initial jobless claims remain near historic lows. Nearly 81% of people between the ages of 25 and 54 have a job as of April. There have only been 49 months (just over four years) in which a higher proportion of so-called “prime age” people were employed in US history, going back to the late 1940s.

The lion’s share of first-quarter earnings season is over, and the results have been stellar: companies are exceeding profit estimates by 8.6% so far, on average. If sustained, that would be the biggest upside surprise since Q3 2021. And 12-month forward earnings per share estimates continued to trend higher, even when the stock market wasn’t.

And there’s even one critical part of the stock market where trends stayed intact through the recent volatility: the banks.

It’s rare to have a 5% decline in US stocks where banks do better than the index at large. Over the past 10 years, banks have had a beta of about 1.25 to the S&P 500 Index (meaning their moves, in absolute terms, tend to be 25% larger than those of US stocks as a whole).

“While global economic performance was surprisingly desynchronized last year, the overall story has been consistent of late, one of economic resiliency supported by tight labor markets and the consumer,” said CEO Jane Fraser during Citi’s earnings call in April.

Simply: banks are a particularly cyclical part of the stock market, and if they’re holding up relatively well, it suggests there isn’t a host of consumer or business credit problems about to rear their heads.