Wall Street’s new strategy: Hope that these tariffs aren’t real

The scale of the trade barriers announced by President Donald Trump on Wednesday means that any bull calls you see out of Wall Street today will have one tenet at their core: take Trump’s reciprocal tariffs seriously, but not literally.

Here’s Wedbush tech analyst Dan Ives:

“Over the coming 24 hours the world will quickly realize these tariff rates will never stay as they are shown otherwise it would be a self-inflicted Economic Armageddon that Trump would send the US and world through over the coming year. We have to assume this is the start of a negotiation and these rates will not hold... stocks will sell-off massively but ultimately our view is these numbers would throw the US into a clear recession and cause stagflation almost immediately... IF they hold (and they will not for long, in our view).

For today with clients... we are taking the approach after speaking with business leaders/supply chain experts from around the world last night that these tariffs (and the fascinating calculations which need to be explained by someone from the White House today) are the start of negotiations with countries and even individual companies to even the playing field. If you start with that assumption then the massive sell-off today (and potentially over the coming days) is a major buying opportunity to own the best tech winners on sale for a policy that will be temporary and not permanent.”

Ives adds that “our focus to own this morning” is Wedbush’s tech winners basket, which includes Nvidia, Microsoft, Amazon, Apple, Tesla, Palantir, Alphabet, Palo Alto Networks, CyberArk, and Check Point Software.

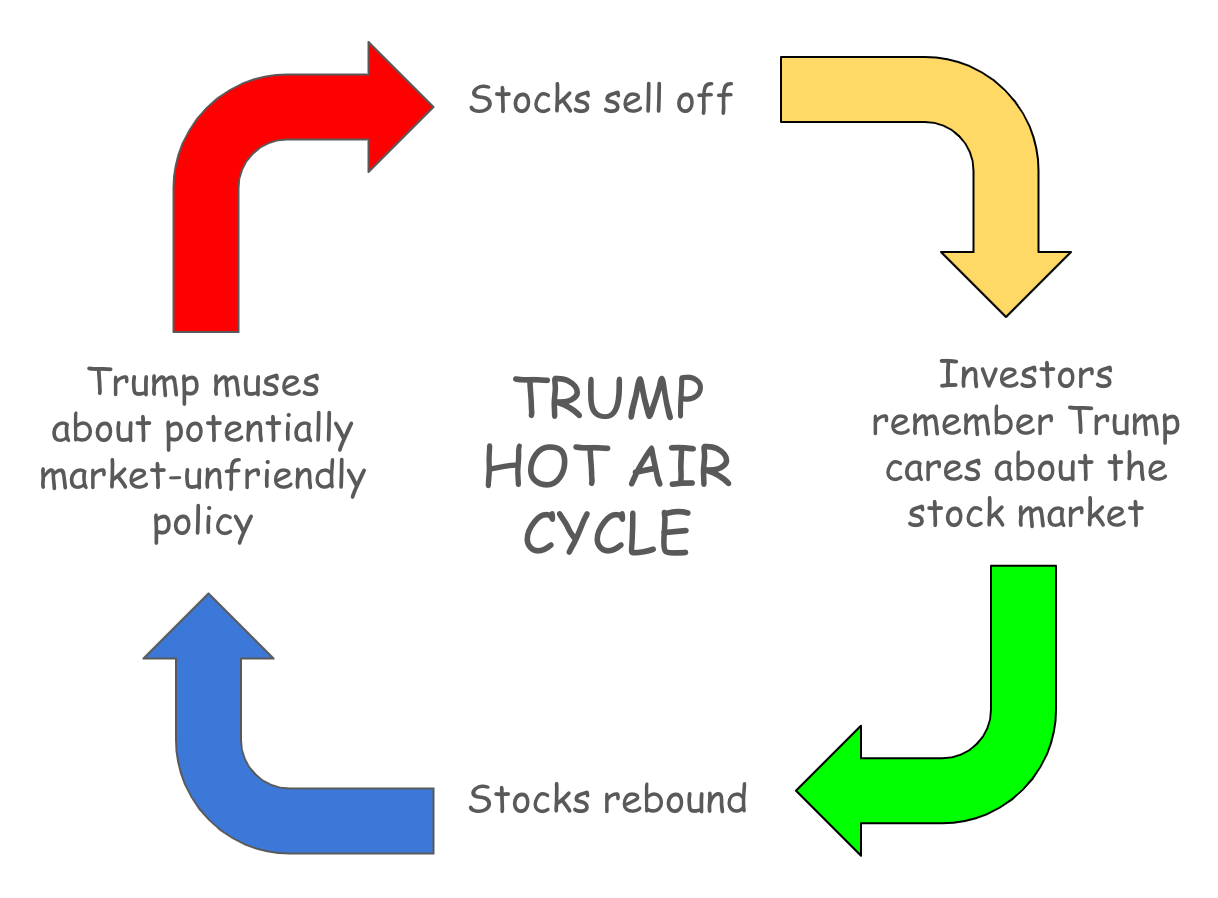

We’ve been pretty vocal about the idea that the proximate cause of the stock market’s retreat from all-time highs has been more a momentum unwind than a pricing in of the economic downside risks that loom following the imposition of tariffs. That’s in part because investors with some memory of Trump 1.0 policy sequencing, as well as the stock market serving as a “report card” for that administration, had cause to shrug off fiery trade rhetoric as cases of the president’s bark being worse than his bite.

When we first wrote about the “Trump Hot Air Cycle,” we noted that this method of thinking conditions investors to react late to negative catalysts — that this is a miniature version of Hyman Minsky’s “stability breeds instability” argument.

“What’s needed to break this cycle? Well, action that everyone was warned about but no one thought was coming, probably,” was the thought. Action that everybody was warned about but no one thought was coming sounds an awful lot like a scheduled “Liberation Day” Rose Garden address. And based on the reaction we’re seeing today in markets — which comes amid a continued reluctance to countenance the outcome of these measures as a new, enduring reality — yes, this has the potential to be a paradigm-shattering event.