With New York’s acceptance law coming into effect, could cold hard cash stage a comeback?

Though digital payments are now the norm, most US adults remain opposed to the idea of a cashless society.

The familiar jangle of coins and pocket-padding of bank notes have become much rarer sensations for Americans today, as tapping and swiping have all but replaced the need for traditional wallets.

But while digital payments have become the go-to for the sake of convenience — even physical cards are now being overshadowed by the rapid rise of mobile payments, with two-thirds of Americans reporting using mobile wallets like Apple Pay in December — a large share of US adults still believe cash is king (or at least deserves a seat at the table).

Benja-maxxing

A survey conducted by the Siena Research Institute, published in January, found that 84% of Americans opposed moving to a cashless society.

That sentiment is echoed in a new statewide law that came into effect in New York on Saturday, requiring food stores and retail establishments to allow customers to pay in cash — mirroring the law that’s been in place in NYC since 2020. However, the rule doesn’t apply to bills in denominations above $20... which aligns with the Big Apple’s dollar-ish slice street food culture, but doesn’t speak to the wider currency landscape in the US.

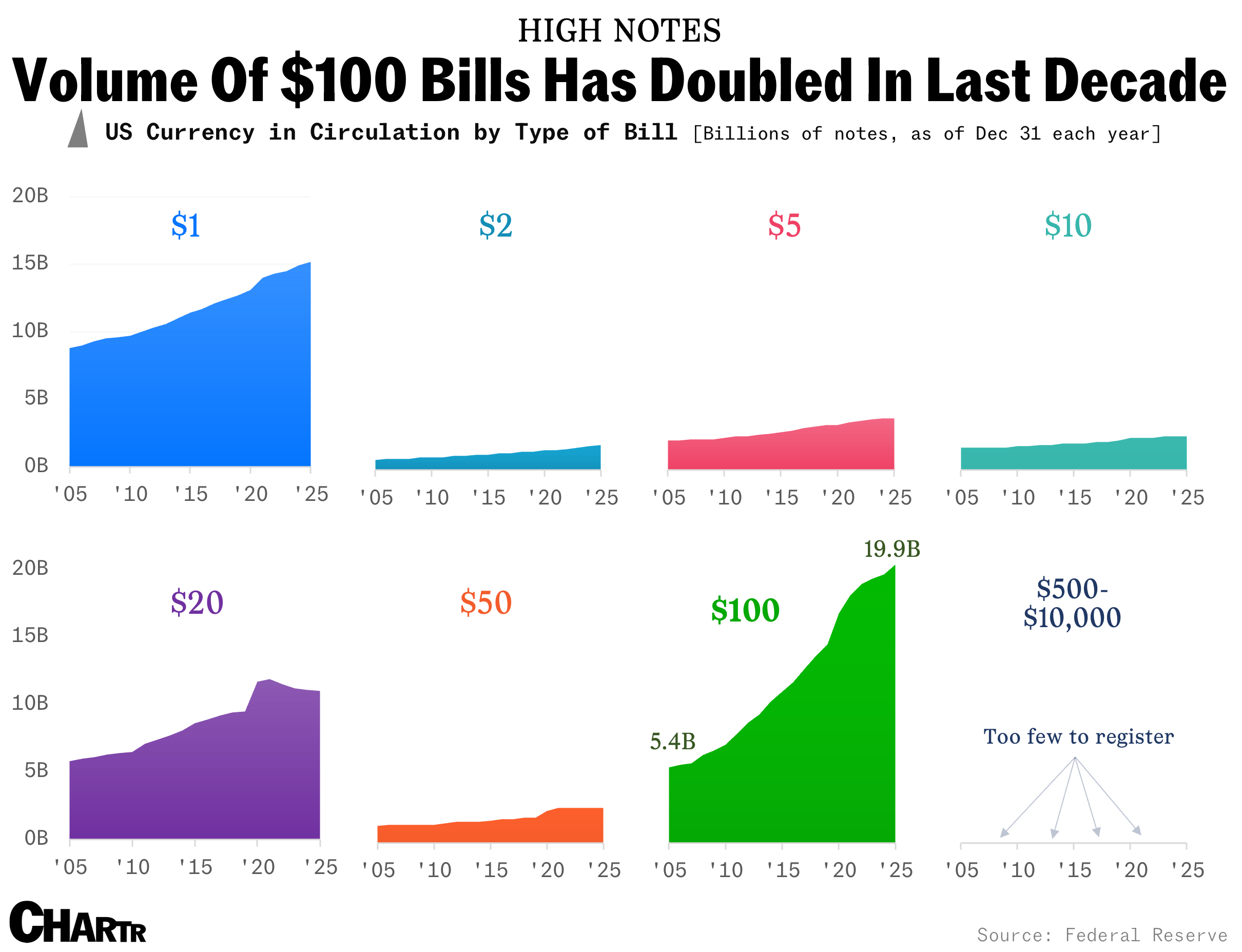

Data from the Federal Reserve on the volume of currencies in circulation shows that the national wallet is stuffed with $1 and $20 notes, with 15.2 billion and 11 billion in circulation, respectively, as of December 31, 2025. But it’s $100 bills that have really taken off, having surpassed the $1 bill by circulation volume back in 2017 and nearly doubling in volume from 2015 to 19.9 billion at the end of last year.

Bills, bills, bills

There are several reasons why the Fed keeps printing so many hundies: for one, $100 bills tend to be saved at a higher rate, owing to a phenomenon known as the denomination effect. International demand for US currency also sees over half of all $100 bills held abroad, which often surges during times of geopolitical instability.

While a shift toward digital payments is still being observed — the US government mandated that all federal disbursements would be made electronic last March, and San Francisco is currently looking to repeal a similar cash-accepting law to New York’s — cash remains relevant, accounting for 14% of all US consumer payments in 2024. Failing that, “cash stuffing” will always be valuable for, well, storing value.