Thousands of bank branches have closed across America

America has lost thousands of bank branches. The latest closure? JPMorgan’s iconic 45 Wall St. address.

Last week, JPMorgan closed its historic branch at 45 Wall St., ending its 150-year stint on the iconic street where John Pierpont Morgan and his ilk created the building blocks for what would become America’s largest bank.

The departure not only exemplifies the gradual exodus of banks from Wall Street itself — once a necessary outpost for any global financial institution worth its salt — but also the wider trend of bank branch closures in cities that once thrived on footfall.

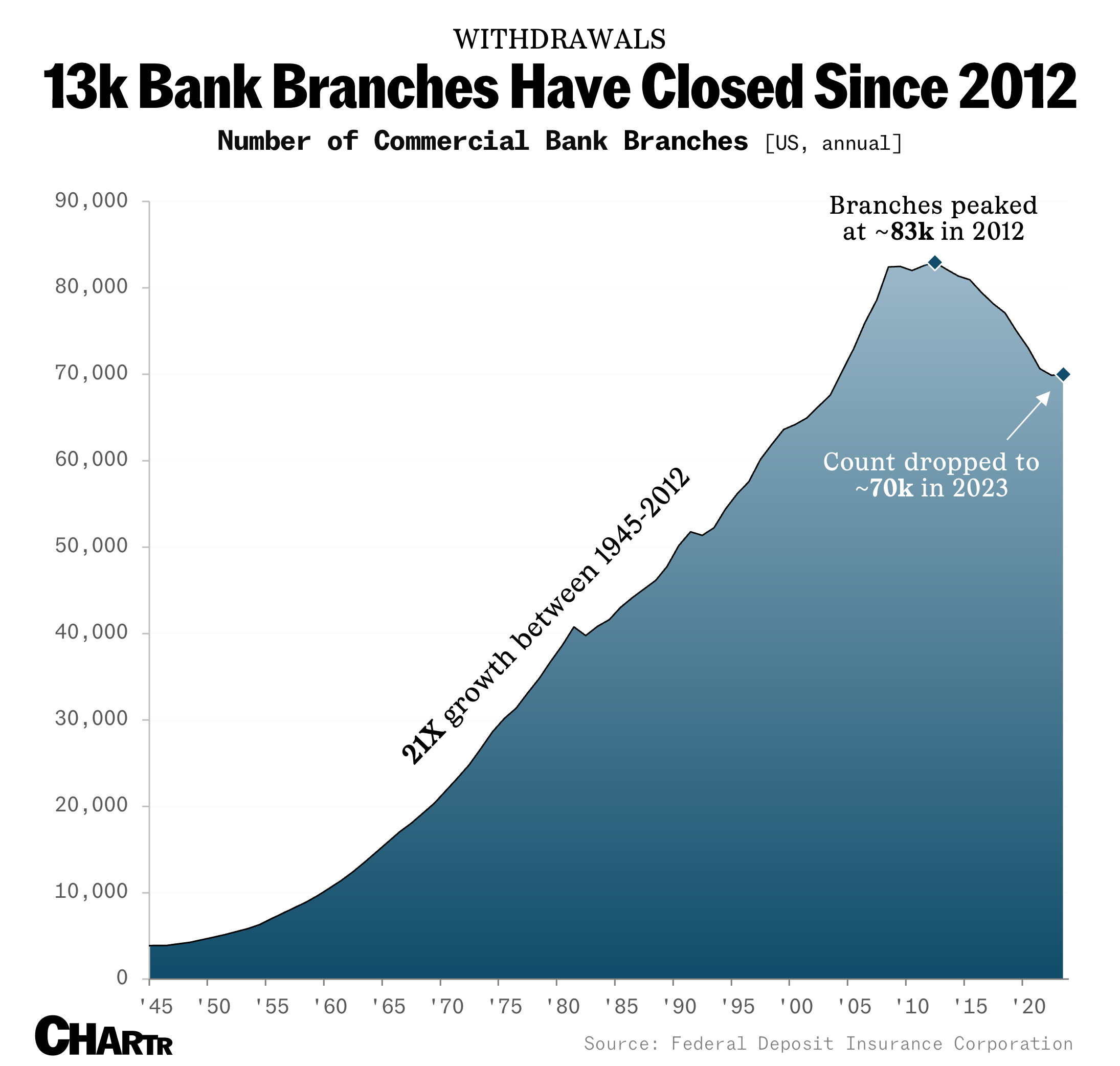

After decades of near-constant expansion throughout the 20th century, America has been shutting commercial bank branches during the last ~10 years, losing some 13,000 since 2012, per data from the Federal Deposit Insurance Corporation (FDIC).

It’s not hard to guess why banks are shutting branches: most of our everyday banking needs are simply met online, with even the most cautious consumers now sending money using computers or phones. Interestingly, however, there are some signs that the decline in branch numbers may be steadying. Data from S&P Global showed that bank branch closures had slowed in 2023, while the FDIC, which tracks the institutions that it insures, also saw that number stay roughly flat (+0.1%).

Clearly, as anyone who has spent time with a banking chatbot can attest, some human interaction is still highly valued. Indeed, despite leaving Wall Street, JPMorgan is far from retreating from physical banking entirely: last year, JPM was a “net opener” of banks, and the company recently announced plans to open 500 new branches by 2027.