Strategy’s STRC “at the center” of one of the “biggest bitcoin buying” months

STRC broke ATM records and saw record daily, weekly, and monthly trading volumes in the billions of dollars.

While some corners of the digital asset treasury (DAT) ecosystem are struggling, Strategy continues to thrive, largely thanks to its digital credit instruments. A new Bitcoin Treasuries report found that April was “one of the biggest Bitcoin buying months since mid-2025, largely driven by Strategy buying — and STRC is at the center of it.”

STRC is Strategy’s perpetual preferred equity instrument, launched in July 2025, with a notional value of $8.5 billion and which provides a 11.50% dividend. The company recently proposed paying dividends twice a month instead of monthly, as it says this “would lead to reduced reinvestment lag, enhanced liquidity, market efficiency, and increased price stability.”

Its proceeds have enabled the largest bitcoin holder to maintain its acquisition pace despite bitcoin’s first-quarter tumble. It now holds 818,334 bitcoin, overtaking BlackRock’s iShares Bitcoin Trust in holdings last month.

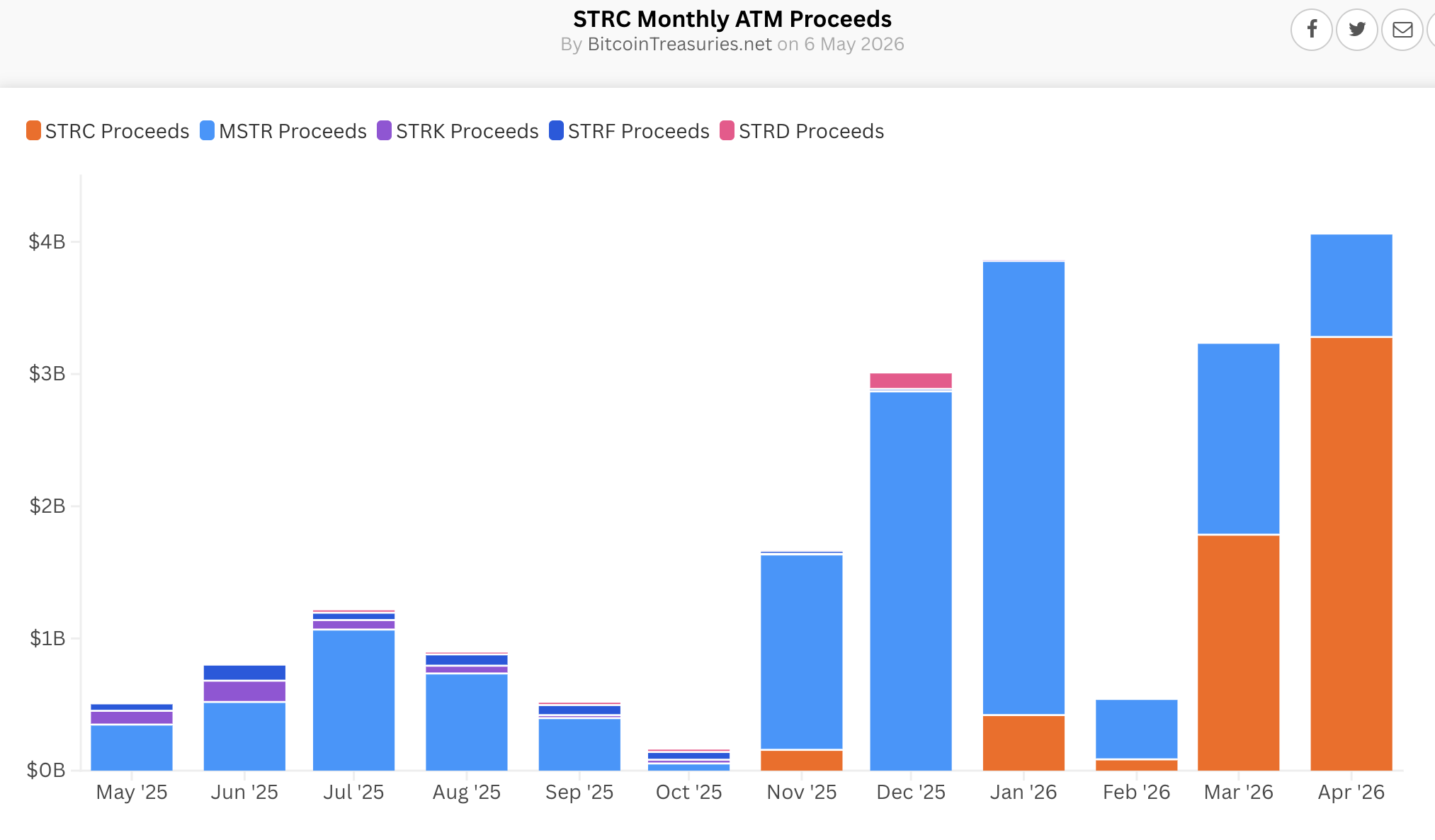

Bitcoin Treasuries analysts found that STRC broke at-the-market (ATM) records, as it made up “$3.3 billion of Strategy’s $4.1 billion in ATM proceeds from April 1 to May 3, and over $5 billion in ATM proceeds in March and April combined, also setting record daily, weekly, and monthly trading volumes in the billions of dollars.”

“We estimate STRC proceeds funded 45,000 BTC that Strategy bought in this period,” the analysts said.

Among STRC holders, institutional fund issuers take the lion’s share, with $450 million in STRC across multiple mutual funds and ETFs, they said.

Strategy’s balance sheet saw a $2.1 billion increase in the first quarter, driven by STRC issuance, and the instrument raised $5.58 billion, a 189% growth in 2026 year to date, Strategy’s May 5 earnings presentation showed.

It is also the “largest tradeable preferred in the world,” according to Strategy, with the second being Wells Fargo’s WFC/PL, at a $4.7 billion notional value.

Ishmael Asad, a Bitwise research analyst, told Sherwood News that STRC has undoubtedly become the favorite of both the market and the company itself. Still, the question that’s been on everyone’s mind is: where is the dividend coming from?

“Saylor finally answered that on their earnings call this week — they’re going to start selling some Bitcoin to pay the dividend,” he said, adding that while this shocked bitcoin traders at first, it’s the only logical answer.

Oliver Carding, head of marketing at Tesseract Group, told Sherwood that what changed on the earnings call was the framing around sustainability, as selling bitcoin to fund the company’s $1.5 billion annual dividend and interest obligations is now on the table.

“The issuance mechanic still works, but the assumption that 818K+ bitcoin sits permanently absorbed has weakened. The model needs three conditions holding simultaneously: STRC trading at or above par, bitcoin appreciating, and obligations not forcing sales. From our perspective, the probability of all three holding tightened materially this week,” Carding said.

Strategy’s issuance in January came from MSTR common shares (8%) and digital credit (12%), and by April it had shifted to 17% MSTR and 83% digital credit, per the earnings report, reflecting the company’s changing strategy.

The instrument has many fans, including Bitwise CIO Matt Hougan, who said that while bitcoin ETFs have played a part in supporting the bitcoin price, the rally from February lows was brought by STRC.

In a Thursday research note, TD Cowen analysts raised their price target on Strategy to $395, up from $385, on “higher expected BTC Yield and BTC $ Gain, reflecting a shift toward STRC-funded bitcoin acquisition that enhances capital efficiency without increasing reliance on common equity issuance.”

TD Cowen Managing Director Lance Vitanza wrote that increased STRC issuance and lower common equity issuance will be “driving meaningfully higher expected BTC accumulation in FY26 and beyond.”

Vitanza also addressed a key investor concern around STRC being a “perpetual dilution machine,” saying it was overstated.

Meanwhile, Benchmark Managing Director Mark Palmer said in a May 6 note that STRC evolved “from an experiment into a killer product” and has “done all of it during a bitcoin bear market.”

Benchmark reiterated its “buy” rating while reducing its price target to $570 from $705, “driven by a reduction in our bitcoin price assumption for YE26 from $225,000 to $125,000.”

Whether the model is sustainable hinges on two factors: STRC investor appetite and Strategy’s obligations-to-BTC ratio, Rajiv Sawhney, head of international portfolio management at Wave Digital Assets, told Sherwood.

Sawhney pointed to Hougan’s earlier framing that there was roughly $10 billion to $15 billion of headroom before that ratio approaches an uncomfortable level, and a meaningful chunk of that has now been absorbed over the past two months.

“So the question isn’t whether they can keep buying, rather it’s whether they can keep buying at April’s run rate. Probably not. A more reasonable expectation is a step-down to a slower, more sustainable cadence, but not zero,” Sawhney said.

As for risks, the main risk is reflexivity, he said, as STRC works because investors believe in both bitcoin’s trajectory and Strategy’s discipline, and both inputs have to keep cooperating.

“In a calm or rising tape, the flywheel does what it’s designed to do. In a sharp drawdown, demand for new STRC issuance dries up exactly when Strategy most needs it, and remember, the dividend obligations keep compounding regardless. It may not be a near-term concern at current prices, but it’s a risk nonetheless,” Sawhney said.

As for whether it can continue to support the bitcoin price, April demonstrated it can, as Strategy was the dominant marginal buyer, he said.

The harder question, he said, is whether it can keep doing the work alone if other demand sources soften.

“Strategy is just one balance sheet, whereas structural ETF demand reflects many institutional players with different investment scenarios. The healthiest setup for Bitcoin is when both are contributing, not when one, Strategy, is doing the heavy lifting,” Sawhney said.