An explosion of speculative call option buying signals the return of retail traders’ favorite weapon

We’re seeing activity that looks an awful lot like gamma squeezes in some of the most speculative stocks.

A funny thing happened after the S&P 500 set an all-time high in late June, officially shaking off the tariff-induced tumble.

The benchmark US stock index became pretty boring while an explosion of risk appetite happened below the surface, propelling nonprofitable tech companies, former SPACs fallen from grace, crypto-linked stocks, heavily shorted companies, and other retail favorites sharply higher.

Most of these indexes have reached multiyear, if not record, highs in the process:

Some companies within these baskets have seen their stock prices surge thanks to a clear catalyst, whether that’s Nvidia starting to do business with them or a pivot to holding crypto treasury assets. Some booms, like Opendoor Technologies, have come out of nearly thin air. But what many of them have in common is an underlying market dynamic that’s reinforcing their gains: the gamma squeeze is back.

The sequence goes a little something like this: traders buy a ton of call options, and they have to buy them from someone (market makers and/or dealers). These players don’t want to make money by taking the other side of this bet, though. They want to make money through extracting value from every little bit of buying and selling activity that occurs. So when a market maker sells a call — which would leave them exposed to losses if shares of the underlying company rally a ton — they will simultaneously offset that risk by buying a given amount of shares of that company.

When lots of traders are buying options, they are effectively forcing a lot of buying of the underlying stock at the same time! This buying can put upward pressure on the share price, which forces even more buying from these entities that have no view whatsoever on the stock, but are merely trying to cover their butts.

Let’s tie in the Greeks: delta is a term that describes how an option’s price is expected to change based on a $1 shift in the price of the underlying asset. Delta will tend to go up as the stock price goes up. When market makers are buying stock after they’ve sold a call (and buying more if the stock rises after that!), they’re delta-hedging. Gamma is the second derivative of delta; it describes how much the delta is poised to change based on a $1 change in the price action. Gamma is at its highest at the point when the option is at the money. This makes some intuitive sense: whether an option is in the money or out of the money will, at expiration, loosely determine whether or not it has any value.

To sum/to some: the natural response of market makers in an environment where increasing out-of-the-money call option buying propels a stock price higher, pushing that strike in the money and pushing the stock even closer to a higher strike price where another formerly out-of-the-money call option threatens to be money-good, and so on and so forth. It starts to look an awful lot like a perpetual motion money-making machine.

A “gamma squeeze” is the technical explanation for how and why these parabolic moves occur. Market makers are rapidly picking up more deltas, which they need to hedge their exposure because gamma keeps accelerating at different, higher points in the options chain. It’s much easier to see this dynamic play a starring role in smaller stocks and/or ones with constrained float.

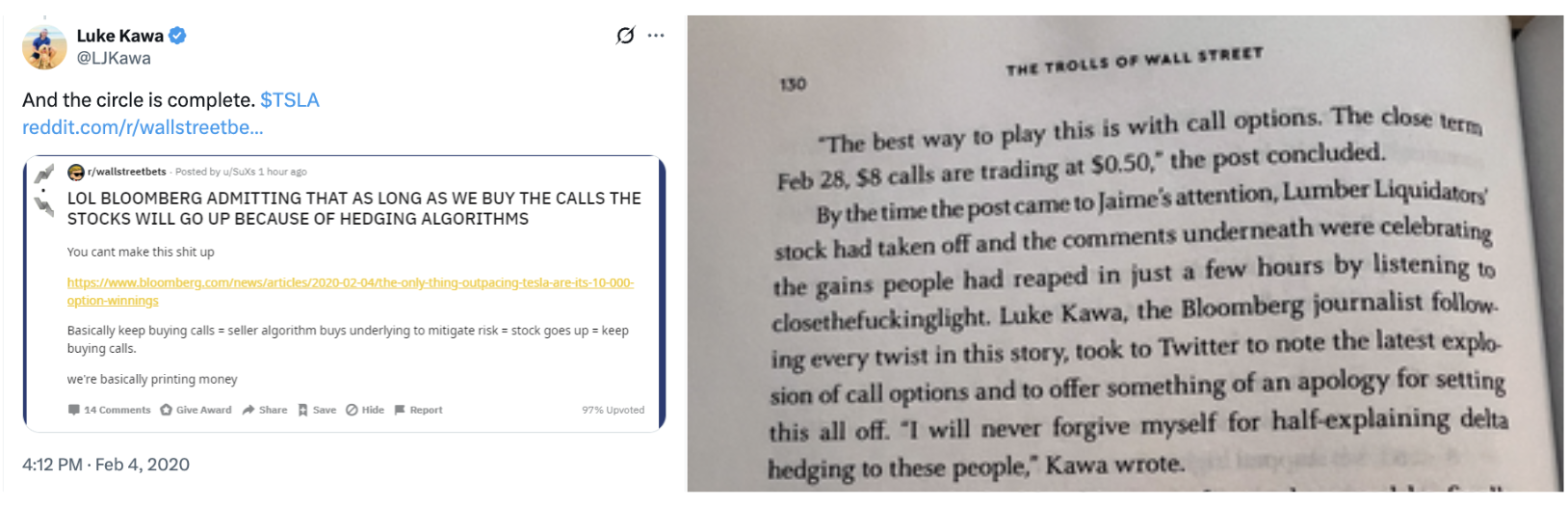

This is something that, while very well known by professional options traders, was “discovered” and popularized in the r/WallStreetBets community in early 2020 thanks to… me (whoops). Similar market dynamics played a significant role in the next year’s mania that took shares of GameStop to record highs.

Benjamin Graham, the famous value investor who trained the likes of Warren Buffett, famously quipped, “In the short run, the market is a voting machine but in the long run it is a weighing machine.”

Well, the gamma squeezes we’re seeing are the market equivalent of stuffing the ballot box in third-world countries.