Analyst: A lot more disclosure needed on these “circular” AI deals

The “circularity” issue keeps swirling.

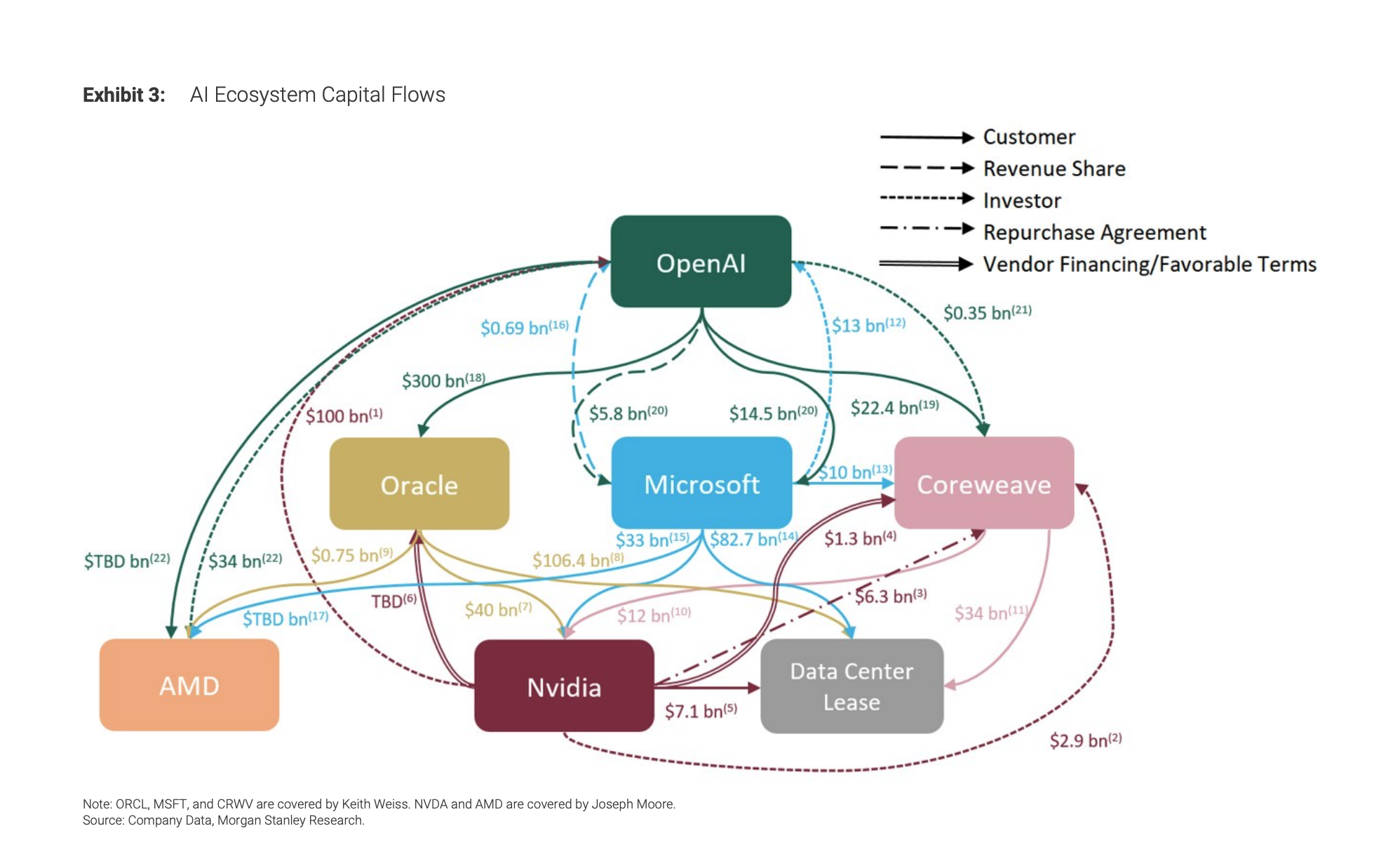

It’s rare that a note on accounting disclosures gets Wall Street’s attention, and even rarer still that a complex visual rendering of tentacle-like corporate linkages goes semi-viral. But a recent report, which included a chart detailing the web of relationships between major AI players, by a team of accounting analysts at Morgan Stanley seemed to achieve this feat.

Published last Wednesday, it focused on a growing concern for many in the markets: the hundreds of billions of dollars’ worth of AI-related deals swirling between Microsoft, Nvidia, Oracle, CoreWeave, and of course OpenAI, which seem to blur usually clear lines between customers, partners, and suppliers — lines that help investors distinguish between arm’s length transactions and overly cozy corporate back-scratching.

We spoke to Morgan Stanley’s Todd Castagno, who headed up the team that worked on the report, to ask him a few more questions on Tuesday afternoon.

The following Q&A has been edited for clarity and concision.

Matt Phillips, Sherwood News: Why are these kinds of circular relationships potentially a worry?

Todd Castagno, Morgan Stanley: I think the potential worry is that with some of these relationships, you have a contract and one of the players may not be able to deliver on that promise. That’s essentially the risk.

So, if one player perhaps cannot meet a commitment, that’s where the circularity, in my conversations with investors, has the potential for a domino effect. That’s the glass half empty view.

But let me go to the glass half full. And that’s that this kind of intertwining is not completely unfamiliar, to be honest.

The best example is the leap into the avionics and aerospace industry in the 1920s through 1950s. Boeing funded its customers. It funded its suppliers. It owned its suppliers. Douglas, which then became McDonnell Douglas, did the same thing. Lockheed. Raytheon.

They were the most creditworthy companies. And in order to scale the aerospace and defense industry, they had to help fund their customers, their suppliers, and sometimes their competitors.

We’re now just seeing that on a massive scale. That’s the nature of it. It’s an ecosystem that probably does need to self-fund, to be honest, in order to scale and compete.

Sherwood: And that’s just because of the sheer amount of money they need, in order to build out these data centers.

Castagno: Correct.

Sherwood: You wrote “increasingly complex transactions make it challenging to evaluate how demand for AI is developing.” Could you explain why these transactions make it challenging to evaluate demand?

Castagno: I think the opacity. We have published work from some of my colleagues that suggests a lot of the numbers from a certain player are maybe somewhat aspirational. We just don’t see that clarity, which is kind of the reason why we wrote this note. And the commitments seem somewhat binding. So some of OpenAI’s commitments with other providers, chip makers, etc., they appear to be somewhat binding. But we don’t see their financial statements.

Sherwood: This is a point you made in the note. For instance, for Oracle to include its deal with OpenAI in its massive RPO number in its recent quarter — which sent its stock up a lot and created a lot of market value — accounting rules require that be a real, noncancelable contract. So the fact that it ended up in Oracle’s RPO number suggests that’s sort of a real contract.

Castagno: That’s the spirit of the accounting rules. The way the accounting works — which is my lane — is at a point in time, you look at this contract and say, “This is a real contract and this is binding.” But in the real world, the economics can change.

Sherwood: Companies can run into trouble, and they might not be able to pay their obligations.

Castagno: A good example of this is lease debt. During Covid, you had a whole bunch of retailers that had contracted to pay their leases over a certain term. But we had Covid and they couldn’t pay. All of the retailers didn’t declare bankruptcy and go out of business; they worked through it by changing the terms of their lease.

In our note, we highlight the potential impact of AI leases as well. And that could be the same thing. They enter into this data center lease for X years for X pricing. What happens if we have another DeepSeek moment and we realized we don’t need half the data centers we think we do? So what is “contracted” is may be a looser concept than it might seem.

Sherwood: What are you hearing from investors and clients on this topic?

Castagno: That’s kind of the whole reason for this note. The reason we wrote it is that the disclosures are not as sufficient as some would expect. Now, I don’t think any of these companies are skirting accounting rules. But I think there could be more transparency, particularly with related party disclosures.

Another thing we highlight is that some of these companies, like Microsoft, are so large, and we’re in such early innings with AI, it gets to the existential SEC issue, which is materiality.

Sherwood: Just to make sure I understand correctly, you’re saying that some of these hyperscalers are so big that from a dollar perspective, these AI deals might not be “material” and therefore might not technically require going the extra mile on disclosures, according to accounting rules.

Castagno: Yeah, that’s why the disclosures will lag. What you’re going to start to see, though, is when these RPO numbers and these contractual obligations start to be executed, then you’re going to start to see the materiality. So I just think we’re in early innings. I think you’re going to start to see Q3, Q4, definitely Q1 next year, you’re going to see some of the things that we’re asking for in terms of more disclosures.

Sherwood: One issue that was fascinating in your note was about joint ventures. Tell me if I get this wrong, but under Generally Accepted Accounting Principles, if there’s a joint venture, say between Microsoft and OpenAI, there’s a world where they may both be able to record the revenue of the joint venture as their own revenue, when really it’s being shared between them both. Did I understand that right?

Castagno: I think that’s a possible outcome. Correct.

Sherwood: So that would clearly be an area that could obscure the true nature of the demand, right? If you’re essentially double-counting the aggregate revenues, that would make demand for AI look a lot stronger than it actually is.

Castagno: We just don’t know, to be honest. I think the challenging nature of these relationships is, “I’m funding you. I own you. I’m buying from you. You’re also buying from me.” So you could get to an accurate accounting outcome, where you do have a sense of double-counting.

Sherwood: But you’re not saying that’s happening.

Castagno: I’m saying we don’t know. And I’m also saying with the way the accounting rules are written, we’ve never seen anything like this with modern accounting rules.

Sherwood: In the note, you spotlight the fact that in its most recent earnings report, Oracle didn’t disclose that “the vast majority of its $318bn RPO growth in the quarter came from a $300bn contract with OpenAI.” You point out that “this concentration creates significant business risk.” From a naive perspective, having great big customer sounds like good business. Tell me a little more why that can be a risk.

Castagno: The risk is the customer trips, and the ecosystem is so concentrated, and you have a cancellation or a contract being changed that can have the opposite effect on the stock price than what we saw. That’s where I get a little bit concerned: if all of a sudden there’s a link in the chain that breaks, is counterparty X going to be able to pay counterparty Y?

Sherwood: Right. Does that then create that waterfall effect of people not being able to pay the next person in line?

Castagno: But cushioning that, as we talked about before, is that these contracts are changeable.

I think, you know, honestly I have to monitor the risks, but you also have to step back. This is real technology. I think a lot of the articles are very negative, suggesting AI is “a house of cards.” The more positive view is that this is constructive to society and productivity.

Sherwood: All right, maybe we should leave it there. This has been super helpful, Todd. Thanks for your note, and I’m glad you’re out there reading all the footnotes to earnings statements so we don’t have to.

Castagno: Well, AI makes it easier. [Laughing]

Sherwood: Don’t tell the bosses!