Buffett’s Berkshire Hathaway has enough cash to theoretically buy every NFL team

The oracle of Omaha has been selling stocks over the summer, and the company’s coffers are fuller than ever.

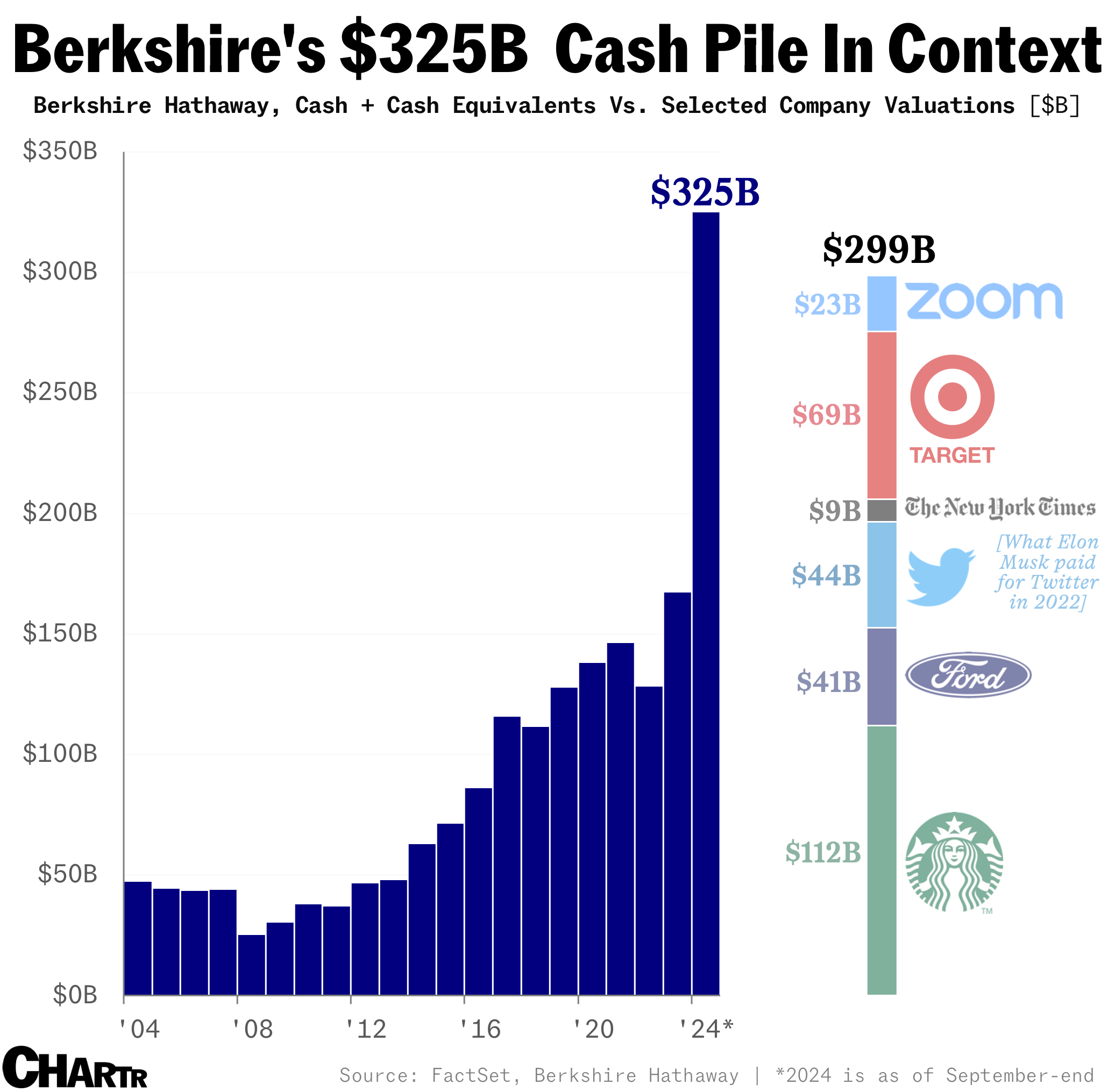

Iconic investor Warren Buffett and his loyal lieutenants have been busy over the warmer months, having sold $36 billion worth of stock holdings in Q3, taking the Omaha-based company’s cash pile north of $325 billion — its highest on record. The company’s stake in Apple was downsized significantly, with filings implying that Buffett and co. offloaded roughly one-quarter of the company’s stake in the iPhone maker, the fourth quarter in a row that Berkshire has trimmed its holdings in Apple.

Why is Berkshire selling so heavily? We wouldn’t presume to know exactly what the world’s preeminent investor is thinking, but there’s a saying: “Don’t listen to what people say; watch what they do.” In this case, by holding more than $325 billion in cash and cash equivalents, Buffett and co. are signaling something along the lines of: we don’t think there are a lot of compelling places to invest right now. And with that much money, not many opportunities are out of reach — there are only a few dozen companies in the US that the group couldn’t acquire outright.

For context on just how much cash it is, the world’s richest person spent “just” $44 billion acquiring Twitter in 2022, Starbucks’ market cap is about one-third of the cash pile, and buying America’s largest news organization wouldn’t take more than ~3% of the company’s hoard. It’s also enough to buy every single one of the 32 teams in the NFL at a 50% premium to their current valuation (which are collectively valued at ~$208 billion, per CNBC).

Is Berkshire Hathaway, like Goldman Sachs researchers, bearish on the future of stocks? Well, when choosing between owning shares in the world’s largest company and parking the cash in US treasuries, the world’s most famous investor is opting for the latter... for now.