Gold and silver are the new meme stocks

Momentum. Flows. Options activity. Intense retail enthusiasm. It’s all there.

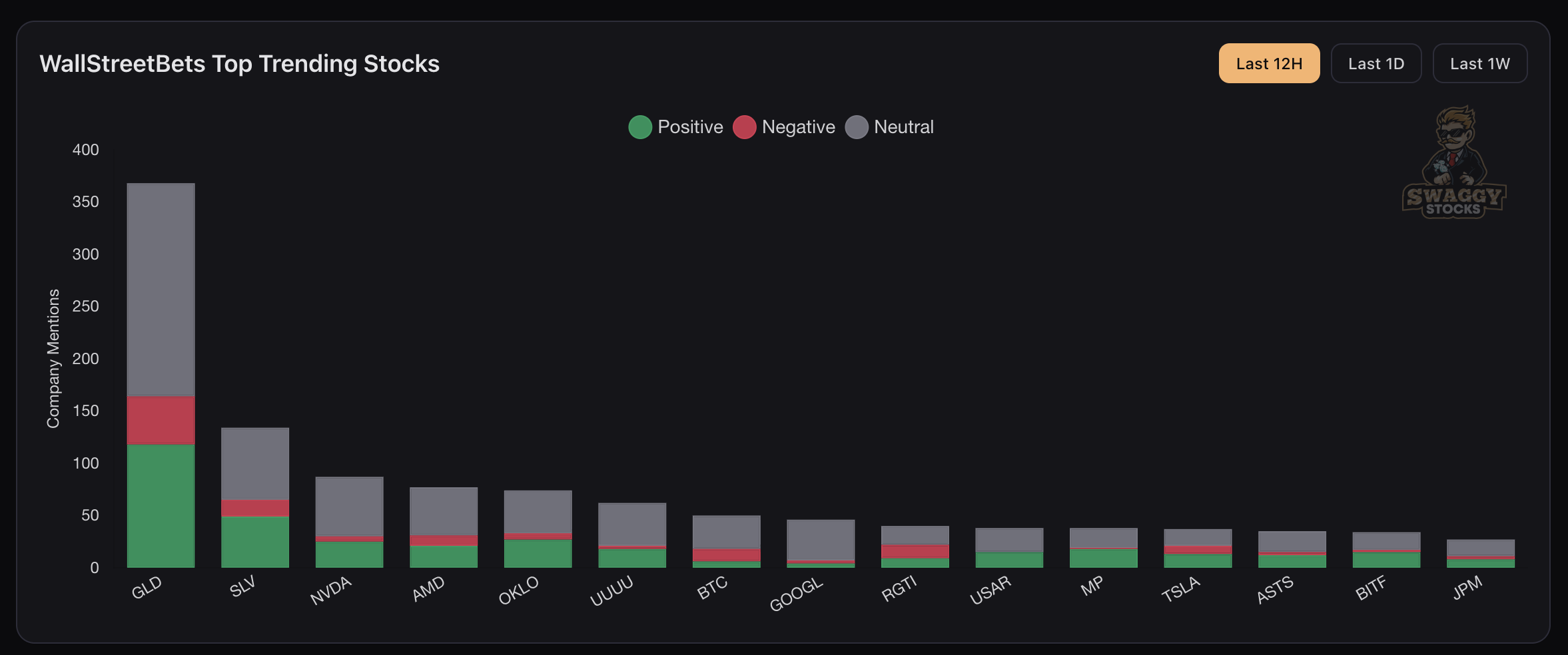

The r/WallStreetBets corner of Reddit is one of the places I go — and one of the sources that the Roundhill Meme Stock ETF draws upon — to get a handle on retail trader sentiment.

And right now, it’s showing quite starkly that gold and silver are the new meme stocks.

Momentum. Flows. Options activity. Intense retail enthusiasm. It’s all there. The new shiny toys for traders are the oldest, shiniest perceived stores of value.

Over the past 12 hours, the SPDR Gold Shares ETF and iShares Silver Trust are the two most mentioned and most positively mentioned tickers on the subreddit, per SwaggyStocks.

JPMorgan strategist Arun Jain, who tracks retail flows, showed that net buying of commodity ETFs from this cohort were $163.1 million as of 4 p.m. ET on Monday, or in the 98th percentile relative to their one-year history. On Friday, those flows were in the 90th percentile, and nearly in the 80th percentile on Thursday.

The five-day average for call volumes in GLD recently hit a record, while those for its silver peer are at their highest since 2021.

The 14-day relative strength index, a technical gauge of the magnitude and persistence of price movements, is at its highest level since 2020 for the silver ETF. The gold ETF, meanwhile, has seen its 14-day RSI close above 70 (which indicates it’s in “overbought” territory) in all but one of the 30 trading days since the end of August. That’s far and away the highest share of time it’s spent in “overbought” territory over any 30-session stretch since this product was introduced in 2004.

The very underfollowed @VKMacro argued on X that the price performance of gold is an example of flows driving very extreme performance:

Commods often go parabolic when investment flows become the largest driver of prices changes and this is an example pic.twitter.com/vd1Iz6Gbbz

— VKMacro (@VKMacro) October 14, 2025

Precious metals are normally what you turn to when the world is going to hell in a handbasket. And yet we’re seeing it bid up at the same time that the AI trade remains near all-time highs, zero-revenue nuclear energy company Oklo is ramping, and quantum computing stocks are also on fire.

Once again, the nature of the assets that are seemingly going parabolic suggests to me that we’re in an intense bull market in anti-humanity.