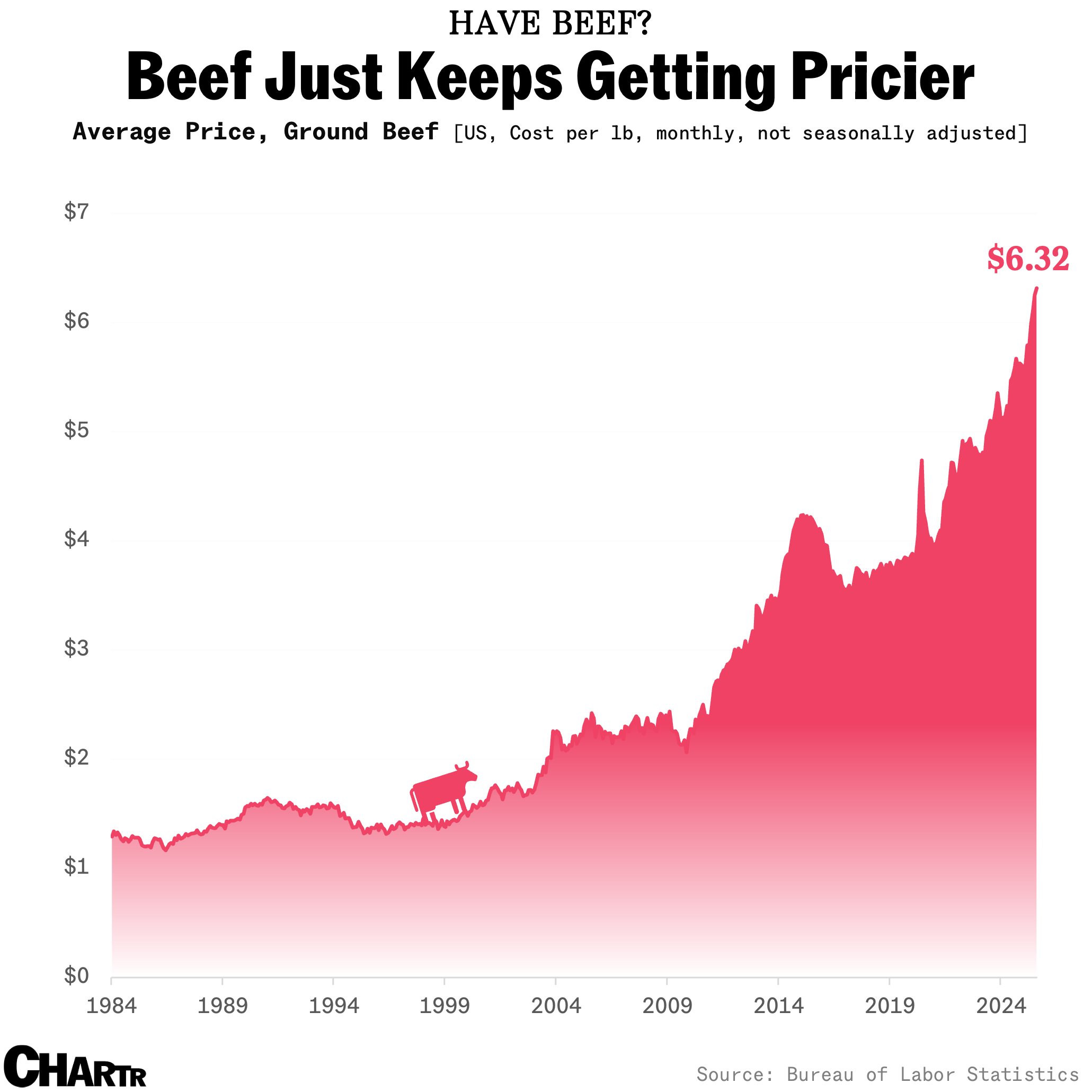

In bad news for protein-hungry Americans, beef is more expensive than ever

Meat-packing giants, meanwhile, are benefiting from beefier prices.

One of the billionaire owners of the world’s largest meat company thinks that the US isn’t producing enough beef to satisfy Americans’ increasingly protein-rich diets. He’s probably not wrong.

“The US is facing the highest beef price in history, and so the US needs to import more and more because production is not there to support the demand,” said Wesley Batista, one of the brothers behind Brazilian meat giant JBS.

While the US has long been a net exporter of beef, imports to the country are now reaching new heights as the nation tries to resolve its domestic beef supply issues, which largely stem from underinvestment in America’s cattle herd a decade ago. Even with President Donald Trump’s “Liberation Day” tariffs in place, the US was importing 30% more beef in the first half of the year than in 2024, as it looked to contain soaring beef prices.

The growing use of GLP-1 weight-loss drugs might also be driving US beef demand. “No one knows exactly what is the impact of these new drugs, Ozempic or Mounjaro... but something is happening because protein overall became [a trend],” Batista said last month.

A lot at steak

America’s beef landscape is dominated by four big companies, which produced 81% of the nation’s beef in 2021, per a USDA report last year. And with supply tight and demand growing, beef in the US keeps getting pricier — which is making meat-packers, not least JBS, fatter.

The São Paulo-based company made almost $2 billion in profit last year, bouncing back after a loss the year before, and has continued to see a 61% year-on-year uptick in net income in the latest quarter.

Now, JBS is looking to cement its status as the top beef producer in the US, where its wider meat and food business accounted for half its revenue in 2024. With prices increasing and the fact that the business produces most of the beef for its US market on American soil, that may very likely continue to tick up in quarters to come.

Related reading: The US beef industry looks a little unsteady — but Americans are still bullish on steak