International investors want to own US assets — and have nothing to do with the US dollar

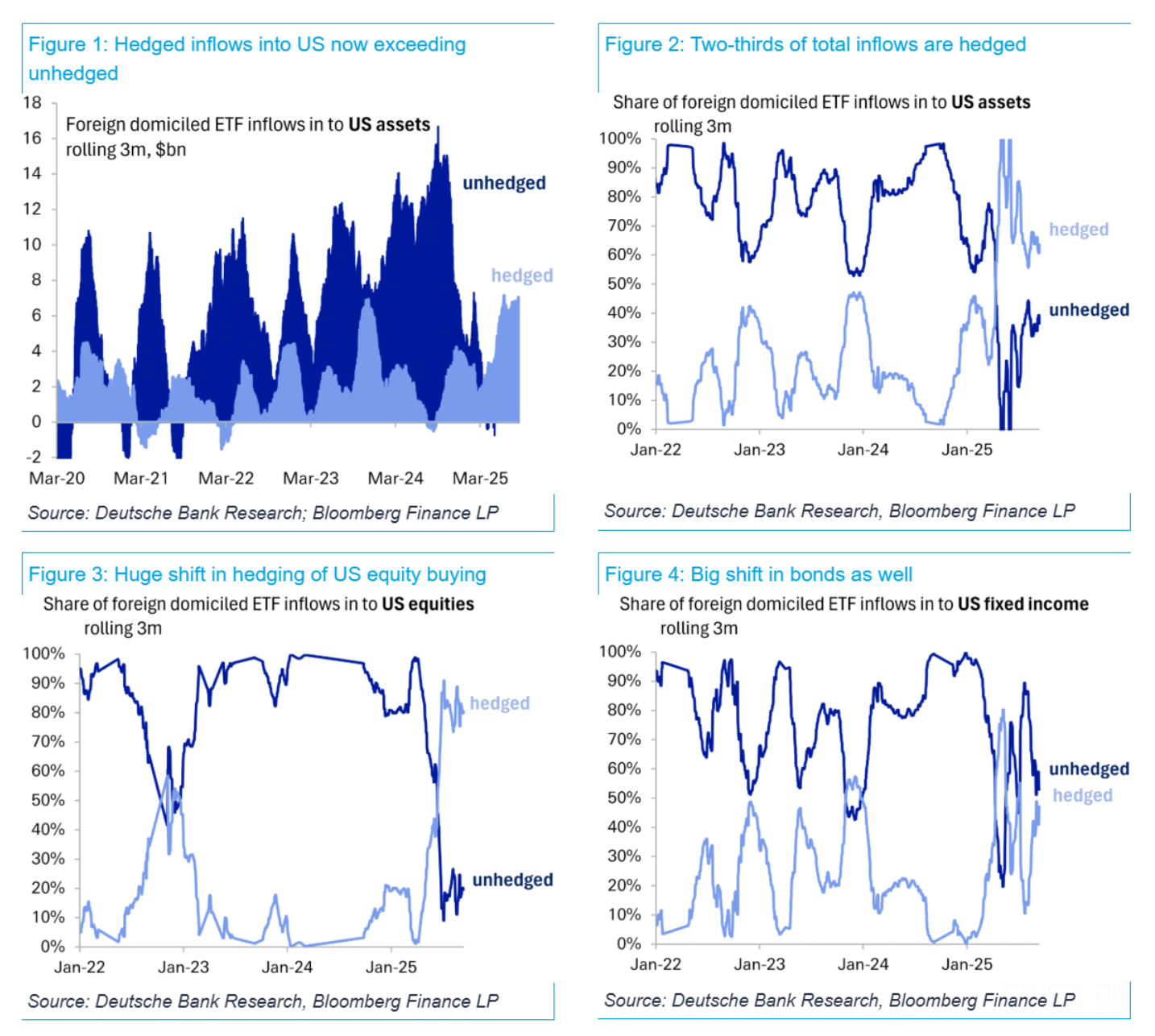

Looking at ETF flows, Deutsche Bank’s George Saravelos found that 80% of recent foreign inflows into US stocks and 50% of inflows into US bonds have been on a hedged basis.

“Sell America” — the global downgrade of US assets in the run-up to and immediate aftermath of the reciprocal tariffs announced on April 2 — was a very painful period for markets, but a very fun narrative to write about.

This narrative appears to have been brief, to the extent it existed at all, and could likely have been more appropriately characterized as “Right-Size Hedge Ratios on America.”

That is, traders want to hold lots US stocks and bonds, but don’t want exposure to the US dollar in the process.

And that story is still running strong, as Deutsche Bank’s global head of FX research, George Saravelos, shows.

“How can US stocks be making record highs while the weak dollar is at year lows? We wrote last week that there is nothing ‘exceptional’ about the US market because global equities are also rallying,” he wrote. “But there is also an important flow story: foreign investors are now removing dollar exposure at an unprecedented pace.”

Looking at ETF flows, Saravelos found that 80% of recent foreign inflows into US stocks and 50% of inflows into US bonds have been on a hedged basis.

There are two implications of this trend that immediately spring to mind.

Saravelos with the first:

“Yet it is only unhedged inflows that finance the US current account deficit and these are running 75% below the peak from last year,” he wrote. “The dollar is falling because the unhedged flow picture looks very weak. With the Fed about to start cutting rates while most other central banks are on hold, hedging dollar assets will only get cheaper.”

And I’ll offer up a second, inspired by Karthik Sankaran, senior research fellow at the Quincy Institute for Responsible Statecraft.

Typically, when conditions get very, very rough and there is visible credit market stress, the US dollar rallies because it’s the global funding currency of choice, and everyone scrambles to get their hands on more of it.

I don’t know when, but there will be a time when credit conditions tighten materially again. If, at that time, there is a scramble for US dollars, then the protection typically provided by the safer parts of investment portfolios will not be as strong of an offset as it traditionally has been.

Bonds might be rallying as part of a flight to safety, but the currency benefits portfolio managers have come to rely on would be AWOL.