Flows data from Monday’s quiet but strong session for US stocks suggests a nascent style shift may be at play, with investors selling tech stocks and buying small caps.

The iShares Russell 2000 exchange traded fund welcomed $623 million of inflows on Monday, topping the leaderboard among US-listed stock products. On the other end of the spectrum, the Invesco QQQ Trust (which tracks the tech-heavy Nasdaq 100 index) endured nearly $1.5 billion in outflows.

Monday’s flows are against the tide, both in terms of what investors have gravitated toward year-to-date and in performance terms. IWM is up just 1.9% year-to-date heading into Tuesday’s session, lagging the 7.5% gain delivered by QQQ. The small cap fund has seen $7.3 billion in cumulative outflows year-to-date versus $8.6 billion of inflows for the tech-dominated product. The acute breakdown in momentum that characterized April’s stock market drawdown may also portend a change in market leadership going forward.

One day of flows does not a trend make. But the last time we saw small caps take in over $500 million while the tech-heavy ETF suffered over $1 billion in outflows was mid-November of last year. IWM went on to rally 12.6% by year-end, outperforming QQQ’s 6.1% advance.

Back in November, investors were focused on how the sharp deceleration of inflation in concert with solid US growth had laid the foundation for the Federal Reserve to deliver imminent rate cuts to rejuvenate more cyclical pockets of the equity market.

Of course, those Fed cuts haven’t materialized yet, and most of the discussions around the Fed as of late have centered on the low likelihood of any additional hikes, with the timetable for delivering easing having been pushed back over the course of 2024.

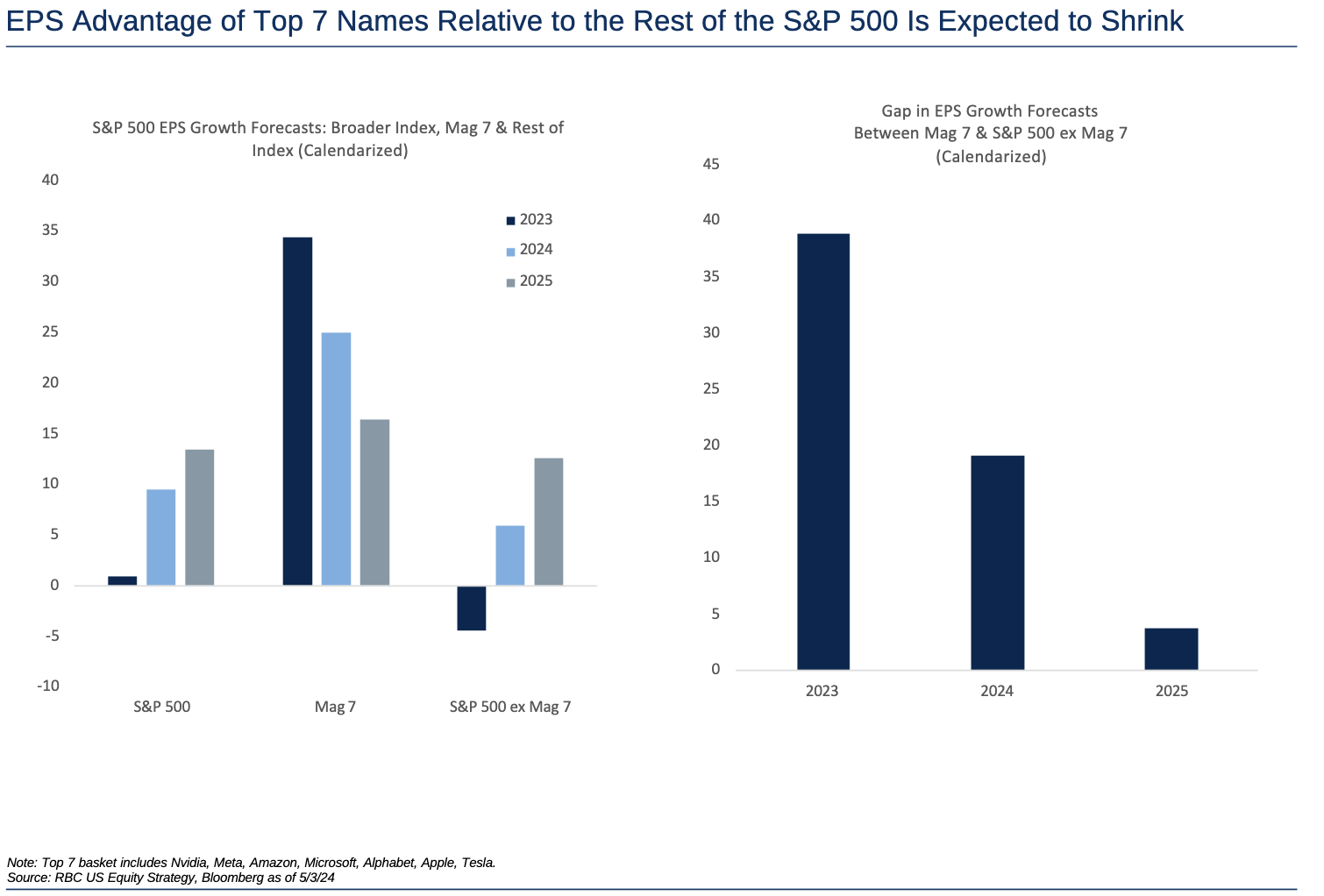

For over a year, the biggest positive catalyst for tech stocks (particularly the so-called “Magnificent Seven”) versus the rest of the market has been their outsized earnings growth, much of which is tied to the AI buildout and application theme. Lori Calvasina, head of US equity strategy at RBC Capital Markets, notes that this profit premium for these heavyweights is waning in 2024, and earnings revisions for the top ten firms in the S&P 500 have been slightly weaker as of late compared to the rest of the index as a whole.

RBC Capital Markets, for its part, is neutral on small cap US stocks. Calvasina observes many positive dynamics at play for this part of the market (it’s cheap, positioning is low, and economic expectations have picked up). However, these need to be balanced against the headwind coming from the lack of urgency for any Fed cuts, which have typically needed to be delivered for an extended period of small-cap outperformance, she concludes.