Musk thinks Tesla has some “rough quarters” ahead, as it waits (and waits) for autonomy

Tesla shares dropped about 5% in aftermarket trading as Musk pondered the company’s significant challenges on the Q2 earnings call.

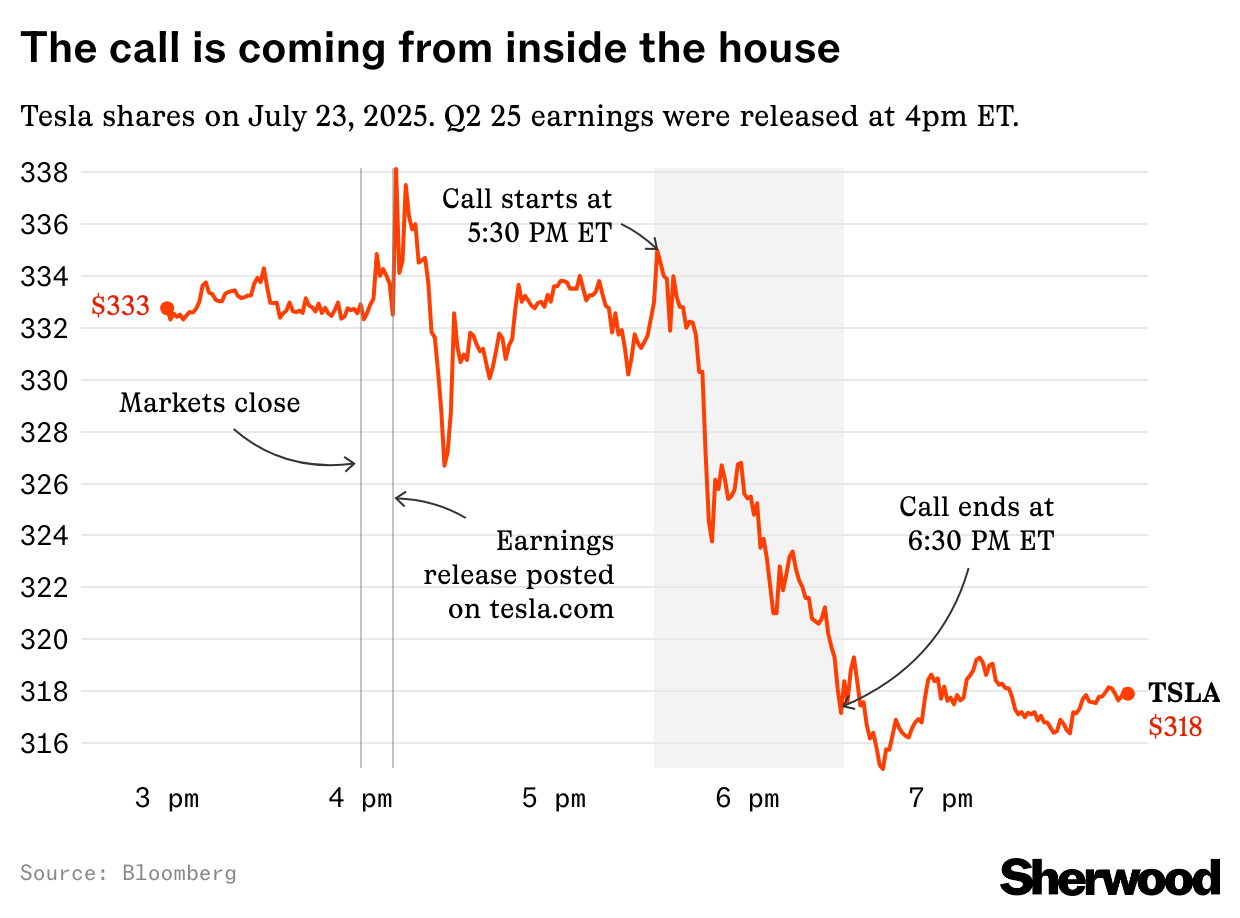

Maybe Elon Musk should say less sometimes.

The news wasn’t great. Despite a few bright notes from Tesla’s second quarter — a largely successful, limited robotaxi launch in Austin, Texas, and essentially meeting analyst earnings-per-share expectations — auto revenue was down 16% from the same period last year to $16.6 billion, making it two consecutive quarterly drops (year on year) for the electric automaker.

Earlier in the month, Tesla saw its biggest quarterly drop in deliveries ever, selling 60% fewer cars from the same period the year prior.

Initially, investors seemed to be absorbing the news of the less-than-stellar second-quarter earnings report, with shares wobbling a little, but not really reacting too much.

But then shortly after 5:30 p.m. ET, an hour and a half after the company released earnings, CEO Elon Musk started talking on the Tesla earnings call. After 19 minutes of rambling “opening remarks,” the stock had dropped 2%, and by the end of the call it had lost 5% of its value since the start of the call.

What did Musk say that investors didn’t like?

The call was pretty low energy, and Musk and other executives spent a lot of time talking about the many obstacles Tesla faces to achieve Musk’s futuristic vision of Tesla as the most valuable company in the world (worth $25 trillion), selling the most successful product in the history of the world (the Optimus humanoid robot) and people making money while their Teslas drive around as for-hire robotaxis (exactly zero people as of today).

Musk has been promising that a lot of these things are just around the corner for many years now, but the truth is that a Tesla dealership lot today doesn’t look a whole lot different than it did five years ago. And a lot of things have popped up that are having negative effects on Tesla that Musk did not foresee.

Caution and hard problems

Musk spent a lot of time talking about how difficult the things were that Tesla was trying to do.

Things that Musk said were tough:

🤖 Optimus robot engineering: “It’s a very hard problem to solve. You have to design every part of it, from physics’ first principle, principles. There’s nothing that’s off the shelf that actually works. So you’ve got to design every motor, gearbox, power electronics, control electronics, sensors, the mechanical elements.”

🚗 Full Self-Driving software: “This is actually a very tricky thing to do, because you, as you increase the parameter count, you get, you get choked onto memory bandwidth, but we currently think we can 10x the parameter count from what people are currently experiencing.”

🇪🇺 EU regulatory approvals: “I think we’re close to getting approval with the Netherlands; then it’s going to go to the EU. It’s quite Kafkaesque. In fact, Kafka had no idea that something like the EU could exist. Beyond comprehensible, the challenges with bureaucracy.”

🇨🇳 Regulatory challenges in China.

🚢 Headwinds from tariffs and supply chain challenges.

Musk emphasized that while he is extremely confident that Tesla will overcome significant technical challenges like Full Self-Driving, the company is being cautious:

“I think we’ll probably have autonomous ride-hailing in like, half the population of the US by the end of the year… But we are being very cautious.”

Goodbye $7,500 tax credit, hello vehicle shortages

Musk’s beef with President Trump got pretty ugly over the past few months, and one of the main reasons was Musk’s dislike of his “big, beautiful bill.” Musk hated it because it will likely hurt Tesla’s car business hard.

At the end of this quarter, the $7,500 EV tax credit from former President Biden’s Inflation Reduction Act expires, which effectively slaps a huge price increase on all of Tesla’s cars. Tesla is preparing for a burst of buyers seeking their last shot at the incentive, but it isn’t well prepared for the surge.

Tesla CFO Vaibhav Taneja said on the call:

“Given the abrupt change, we have limited supply of vehicles in the US this quarter, as we have already thin lead times to auto parts to build cars.”

Another painful side effect of Trump’s tax bill will be a steep reduction in sales of regulatory credits to other carmakers that aren’t selling enough EVs.

Even before the effects of the tax bill really hit, this easy money is drying up. Tesla saw regulatory credit sales of $439 million in Q2, less than half the $890 million the company made from the sales in the same period a year prior. The loss of the credit sales could imperil half of Tesla’s profits, according to JPMorgan.

“Rough quarters” ahead

While reflecting on the painful loss of regulatory incentives in the US and the lingering challenges of achieving “autonomy” for Tesla’s cars and robots, Musk declared that the company was in a “weird transition period.” You could almost feel the other executives in the room tense up as Musk expanded on this:

“Does that mean, like, we could have a few rough quarters? Yeah, we probably could have a few rough quarters. I’m not saying we will, but we could, you know, Q4, Q1, maybe Q2. But once you get to autonomy at scale in the second half of next year — certainly by the end of next year — I’d be surprised if Tesla economics are not very compelling.”

Despite all of Tesla’s obstacles, Musk’s optimism for the future Tesla he imagines is indefatigable. “I’d be surprised if at the end of five years, 60 months from now, if we are not roughly making 100,000 Optimus robots a month, I would be shocked.”