The AI trade roars back after its worst week since April tariff announcements

The AI trade is roaring back after getting speed checked last week.

Baskets of US AI beneficiaries compiled by Morgan Stanley and Bank of America, which just suffered their worst week since the Rose Garden tariffs announcement, are up more than 3.5% in early trading to lead a broad-based market recovery amid optimism that the government shutdown will soon be over.

The likes of Palantir Technologies (which tumbled despite reporting strong results), Western Digital, and Seagate Technology Holdings are all up more than 4.5% as of 10:45 a.m. ET.

Semiconductor stocks are also rallying strongly after Nvidia CEO Jensen Huang asked his counterpart at TSMC to boost chip output.

“While the bears will continue to yell ‘AI Bubble’ from their hibernation caves we continue to point to this tech cap-ex supercycle that is driving this 4th Industrial Revolution into the next few years,” Wedbush Securities analyst Dan Ives wrote. “This is our focus and along with our AI use case work in the field is driving trillions of spending over the next few years and thus will keep this tech bull market alive for at least another 2 years in our view.”

Bank of America argues (convincingly) that last week’s retreat in the cohort had little to do with any industry-specific fundamental news.

“The pervasive skepticism re AI capex is understandable but likely a contrarian positive, helping minimize overcrowding,” Bank of America analyst Vivek Arya wrote in a note reaffirming his conviction on his preferred data center and semicap stocks. “Yes, large-cap AI semis have been volatile (down 7-8% on average last week) but we argue that was driven by (correctable) macro factors (US govt. shutdown, weak jobs data, tariff turmoil, misstated OpenAI comments) rather than any negative datapoint about the AI spending cycle.”

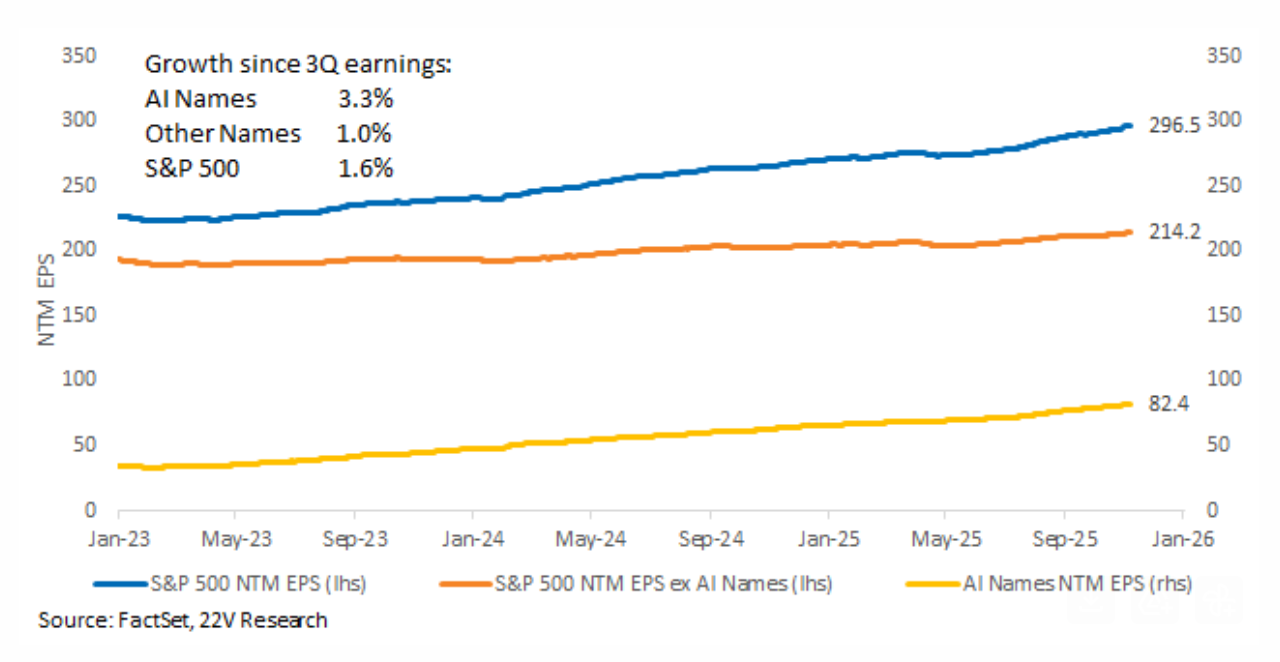

Further bolstering that argument, 22V Research flagged how earnings expectations are improving much more rapidly for AI-linked firms than the S&P 500 at large.

“AI usage and AI related fundamentals are unusually strong,” wrote Dennis DeBusschere, chief market strategist at 22V Research. “In 3Q, AI earnings growth rate has been ~3x that of other S&P names.”