Assets tied to the riskiest parts of the market and the economy are getting dumped in unison

If you’re looking for things to worry about, this combination of risk appetite souring on thematic, volatile stocks at the same time as companies that are in the business of giving money to less creditworthy companies should probably be near the top of the list.

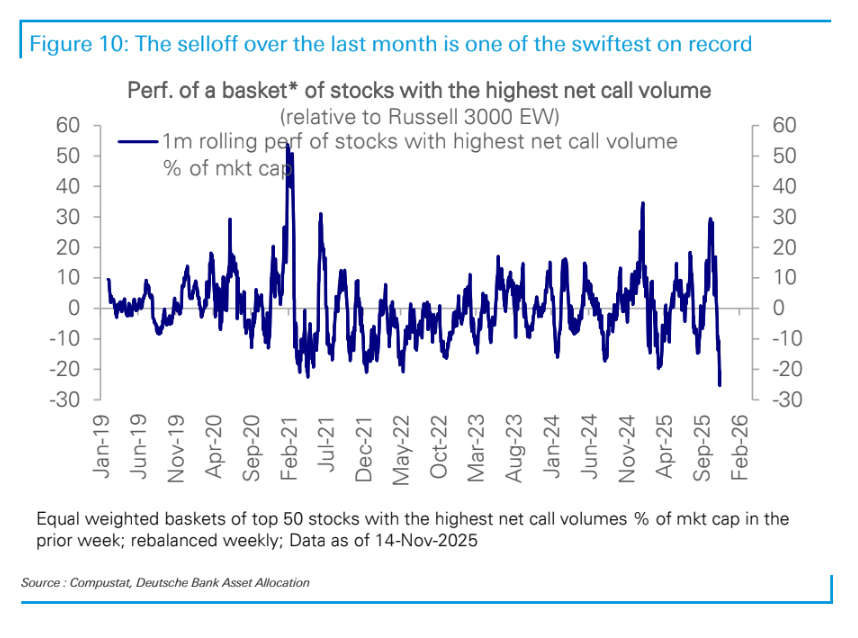

Speculative assets and parts of the stock market linked to riskier pockets of the economy are tumbling in unison.

In recent weeks, both the quantum computing space and smaller AI-linked companies have seen significant selling pressure, as has bitcoin. Given that crypto is a place with limited fundamentals to draw on, it’s a very good gauge of the ebbs and flows in risk appetite.

“The pockets of momentum chasing which had surged in September and early October, first stumbled on the US-China trade escalation, then continued bleeding and have now been completely unwound, with the selloff one of the swiftest on record,” Deutsche Bank strategist Parag Thatte wrote.

This sell-off is occurring in tandem with a slump in business development corporations (BDCs) — that is, firms in the private credit business that lend to small or midsize US companies. This space has been rocked by high-profile busts at Tricolor and First Brands, sending the VanEck BDC Income ETF sharply lower.

On Monday, Blue Owl, one of the biggest holdings of that ETF, is coming under acute pressure as the Financial Times reports that it has blocked redemptions in one of its earliest private credit funds as it prepares to merge with another of its vehicles, and investors could be facing losses of about 20%. In the stock market, traders of Blue Owl are hooting first and asking questions later, pushing shares down to a fresh 52-week low on Monday.

The 21-day correlation between the daily percent change in the iShares Bitcoin Trust and VanEck BDC Income ETF has exploded higher, reaching levels not seen since the nosedive and subsequent rebound as onerous tariffs were imposed and then watered down in the second quarter of 2025.

If you’re looking for things to worry about, this combination of risk appetite souring on thematic, volatile stocks as well as crypto at the same time as companies that are in the business of giving money to less creditworthy companies should probably be near the top of the list.

(Probably nothing a good Nvidia earnings report couldn’t get us to forget about, though.)