The war is a mega rotation trade

Coming into this week, there had been some very well-defined and well-subscribed trades:

Memory stocks > everything, especially software.

Rest of the world’s stocks > US stocks.

Within the US market, the many > the few (as in, S&P 500 equal weight over S&P 500).

War is far from kind. In fact, for markets, it is seemingly a catalyst for mean reversion: all of these aforementioned trades are reversing this week.

There’s some fundamental backing, or at least an excuse, behind all of these unwinding:

Europe, for instance, is much more adversely impacted by oil price shocks than the US;

That’s also true for South Korea (whose market is dominated by a pair of memory chip stocks);

Oil price spikes are generally negative for economic activity; tech companies (particularly the heavyweights) have tended to enjoy acyclical growth.

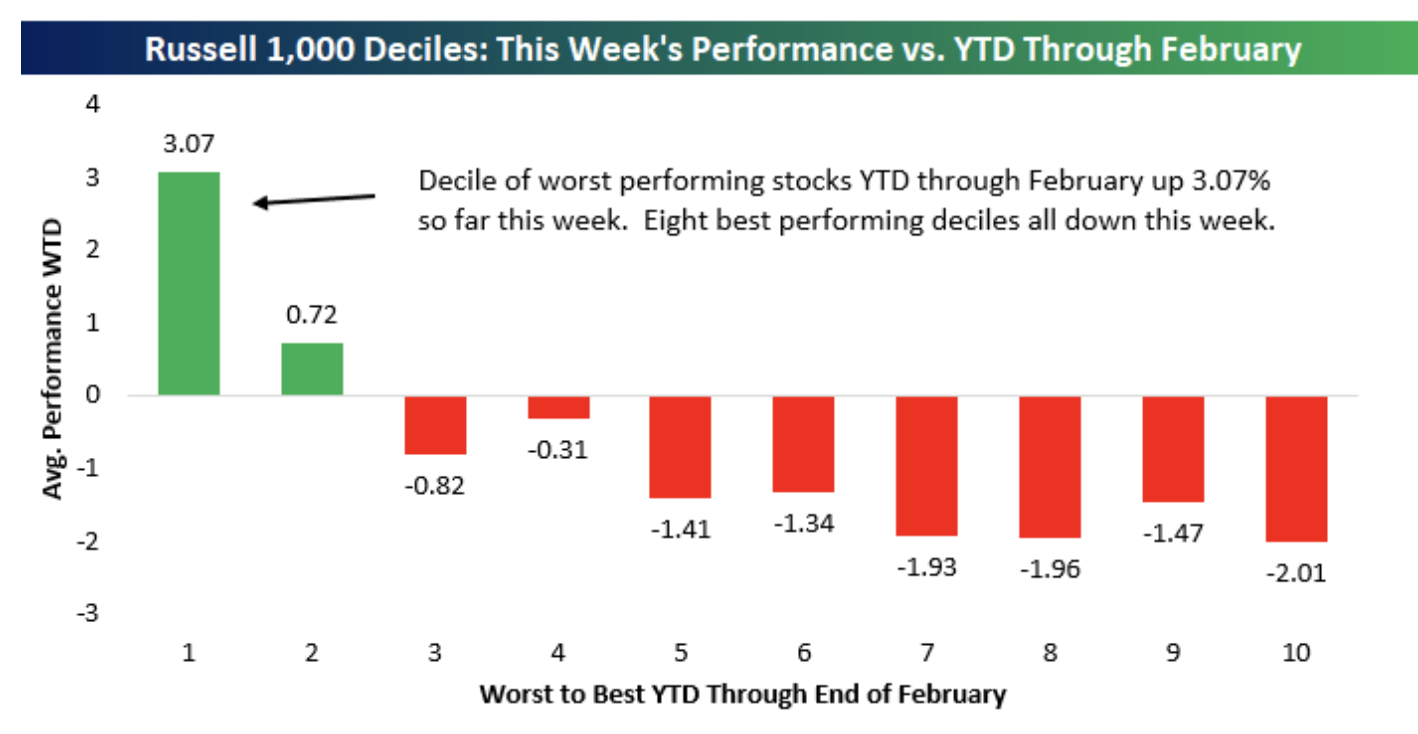

“Who knew that a war against Iran would cause a mean reversion trade here in the US?” wrote analysts at Bespoke Investment Group on Wednesday. “So far this week, the best-performing stocks have been ones hit hardest this year through February, and vice versa.”

For markets, the risk was that war would drive a pickup in correlations within US stocks and between different asset classes. On Tuesday, the price action was validating and accentuating these concerns. Since then, broadly speaking, it hasn’t.