Why investors will always be buying US bonds even as debt swells

Income, portfolio protection, and a pat on the back from regulators.

“Who will buy all the bonds?”

You’ve probably heard this recently, usually around a government-deficit projection or debt-auction announcement.

The (rhetorical) question is grounded in three related concerns. One is the size of US government deficits and debt. Another is that deficits will push inflation above the coupon income earned from bonds. The third is that a government in cahoots with the Federal Reserve will hold rates down, risking (or welcoming) inflation in order to ease its debt burden. The jargon calls this last fiscal dominance, a practice that subjects unwitting holders of government debt to bondage.

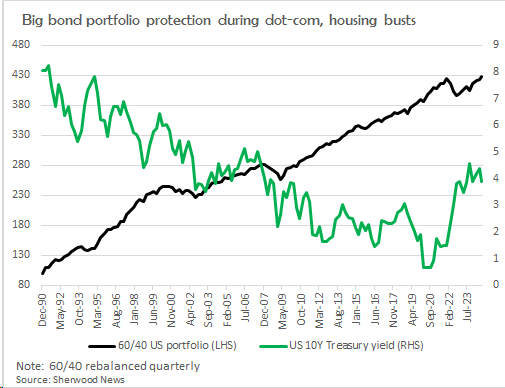

And yet, the 10-year yield fell from 4.7% on April 25 to a closing low of about 3.8% on August 5. Much has happened since April, but this was mostly caused by rising anxiety about a precipitous slowdown that came to a head after weak July jobs data. This is interesting because one can expect two things in an economy with less activity: tax collections will fall, and expenditures (on unemployment benefits and such) will rise.

In other words, a weakening economy would result in rising debt-to-GDP ratios and the specter of insolvency that terrifies “whowillbuyers.” And when fears of a slowdown increase dramatically, yields on high-yield debt typically go higher. Junk gets junkier. By simultaneously raising the interest rate for refinancing debt and lowering revenue, a slowdown brings default closer. As that specter nears, any new buyer for debt must be compensated with higher yields — which only exacerbates solvency issues. But that did not happen to Treasuries.

Instead of fleeing from bonds, people fled into them. Ironically, one reason lies in what whowillbuyers complain about. The US government has a buyer in the Fed who could “print the money” the Treasury owes. Obviously this can go horribly wrong, as those invoking Weimar and Zimbabwe keep reminding us. But this also means the US government is not subject to a solvency constraint driven by vicious interactions between interest rates and growth, making it unlike any other debtor in the economy. This also applies to governments of other countries indebted in their own currencies and with a credible central bank. (For trick questions about Italy or Spain, see me after class.) For a US investor, this makes bonds a pretty safe place to be in most recessions most the time. And that’s exactly how they reacted.

There are other reasons to hold bonds. You get back at maturity all the money that you put in. Admittedly, it may buy you fewer things than when you bought the bonds, because of inflation, but even that varies. You would get less house than you did 10 years ago, but a lot more pixels and screen acreage.

You would also likely have earned some income while you held it. Earning an income and receiving the par value of your principal might not seem like a big deal, but it helps. Ask a man who succumbed not once but twice in three decades to the siren call of fuel cells.

Incentives for institutional investors are even stronger. Bonds are the most liquid securities in the world, making them preferred collateral. They are assigned a “zero-risk” weighting by regulators — i.e., banks don’t have to assign loss-absorbing capital to hold them. And, during the banking troubles last spring, the Fed created a program to lend money against bonds that valued them at face value rather than market price.

So a bond pays you a predictable amount annually to hold it with a pretty cast-iron assurance that your principal will be returned (and comes without a deposit-insurance ceiling). You know that regulators dress it up with other enhancements for institutional buyers, and in many (but not all) instances of a slowing economy, its value will likely rise, acting as a dampener of portfolio volatility. What’s not to like?

Here comes the fine print, but in regular size. The ability of a bond to offset other losses in a portfolio depends on two things. The first is its coupon (that is, the interest paid to investors), and the second is its maturity. The lower the coupon and the longer until the government returns your principal, the faster a bond’s value will plummet in the face of inflation. This makes sense — every year, you’re losing purchasing power. So that 0.85% coupon, 100-year Austrian bond issued in 2020? Yikes. But they’re not all like that.

There’s also a global consideration here. If inflation depends on the balance between supply and demand, then it matters what form economic shocks take. The 1970s saw OPEC oil shocks set off inflation in developed economies. Covid and Russia’s invasion of Ukraine were marked by a whiplash — a demand implosion that led to plummeting bond yields was followed by fiscal stimulus and serial supply shocks that pushed inflation higher, fast. One result: rising inflation and sluggish growth made low-coupon bonds drag down rather than buffer a “balanced” portfolio combining stocks and bonds. But if we return to something like the first two decades of the 2000s, where shocks were primarily to demand, bonds could perform that balancing function better.

I owe you some sense of what the term “high-coupon” might mean. My rule of thumb is that if you trust the Fed to do what’s necessary to hit 2.0% inflation over the longer term, and the US economy grows at just under 2.0% real, a 4% coupon on a 10-year bond affords both income and a portfolio buffer against periodic cyclical hits to growth. Even if you don’t agree with the numbers, this exposition might help frame things.

Perhaps then your answer to whowillbuyers will be: um, maybe me?

Karthik Sankaran is a macro strategist/portfolio manager with 16 years’ experience on the buy side and sell side in emerging markets, foreign exchange, and interactions of national geopolitics with asset markets.