United Airlines’ dual forecasts have a deeper, ugly message about the outlook for US stocks

The bull case for the US, omnipresent for over a decade, is much more elusive these days.

There’s a hidden message in United Airlines’ dual forecast that’s being celebrated by Wall Street. In this case, what’s not being said is speaking volumes.

The management team at the airline provided two sets of guidance for this year: one for a “things stay the same, as we expected” outcome, and one in the event of a US recession.

It leaves one wondering, if that’s the status quo and the bear case, what’s the bull case?

Now, this may be an attempt to keep investor expectations in check, setting up a low bar to step over later. These kind of tactics from management teams are why Societe Generale strategist Andrew Lapthorne once slammed earnings season as “cheating season.” But if anything, United’s forecasts on what would happen to the company’s finances in a recession are a significant improvement versus what’s happened in either of the past two.

But in discussing the outlook for the US dollar, Jon Turek, founder of JST Advisors, posed this question: “What is the right tail?”

Left-tail outcomes are ones where the economy goes pear-shaped. Right tails are positive surprises — best-case outcomes.

That’s a pretty profound question that applies not just to the US dollar, but also the domestic economy and stocks. It gets straight to the heart of how deeply the US outlook has changed since November, when optimism about how bright America’s future would be ran rampant, thanks in part to presumed pro-business policies that would be pursued by the incoming Trump administration.

For years, the US has had a much more visible bull case than other global markets, thanks to outsized profit growth (primarily through megacap tech firms) and relatively more supportive (or less destructive) fiscal policy decisions compared to the rest of the world.

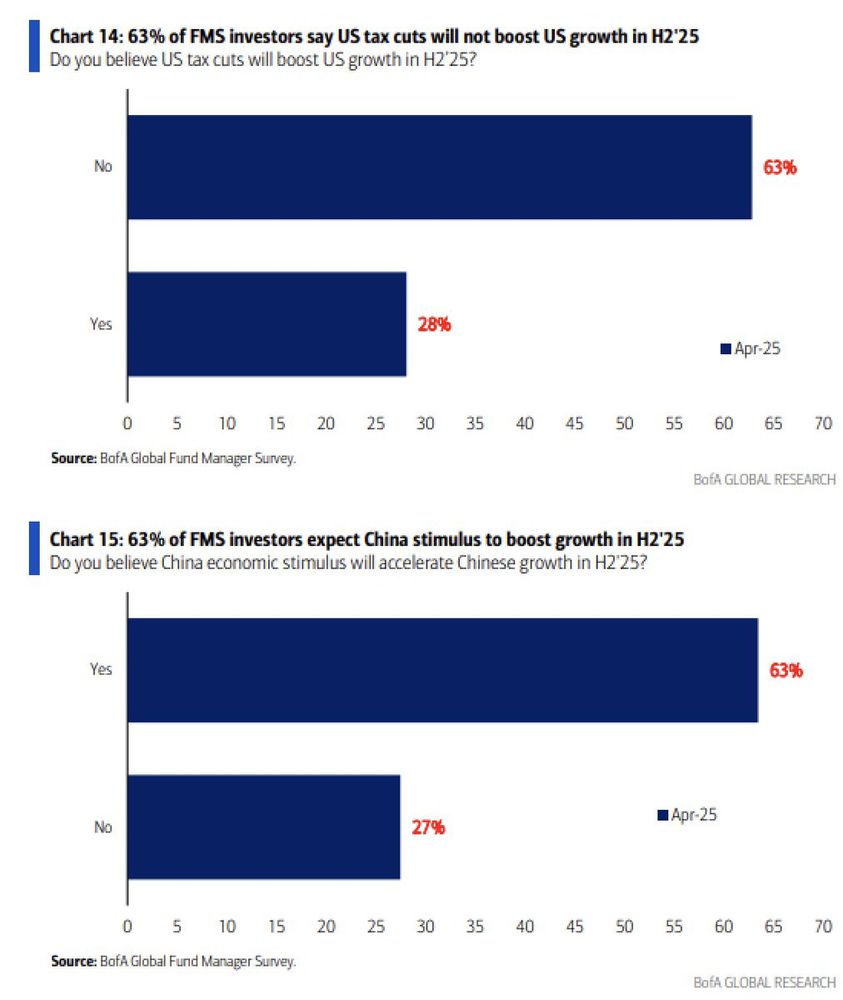

Now, per Bank of America’s April global fund manager survey, investors are much more confident that Chinese policymakers will deliver fiscal stimulus that boosts growth in the second half of this year than they are in US activity getting any kind of a lift from tax cuts.

Deutsche Bank strategists Michael Puempel and George Saravelos observed that foreign ownership of US stocks has increased sixfold since 2010, with most of that increase coming thanks to valuation increases rather than new money piling in, and that position is at risk of reversing to the detriment of US assets.

They wrote:

“The increased weight towards US equities during the bull market years is what stands out the most from our analysis. This has likely lowered the bar for repatriation flows driven by negative asset price moves, thus increasing the sensitivity of the USD to equity valuations. If US-centric trade actions are determined by market participants to represent a structural shift in policy over the next several years, eroding the US equity exceptionalism narrative, it is likely that investors will begin to increase allocations to non-US markets, presenting a headwind to the USD over the near to medium-term.”

The world’s massive overweight position in US equities is something that fund managers are unwinding at a record pace with no end in sight, per Bank of America.

Maybe the AI boom really heats up again (or never really slowed down as much as feared). Maybe there’s enough resilience in US households and corporate balance sheets to weather the hit to growth coming from tariffs, and we’re facing more of a prolonged slowdown in growth rather than a recession.

But “we think our old winners still have more legs and maybe we won’t have a recession” is not the kind of bull thesis you’d put on a bumper sticker.