We're in a godawful vintage for venture funds

Data from Carta shows that venture funds launched in 2021 and 2022 are struggling.

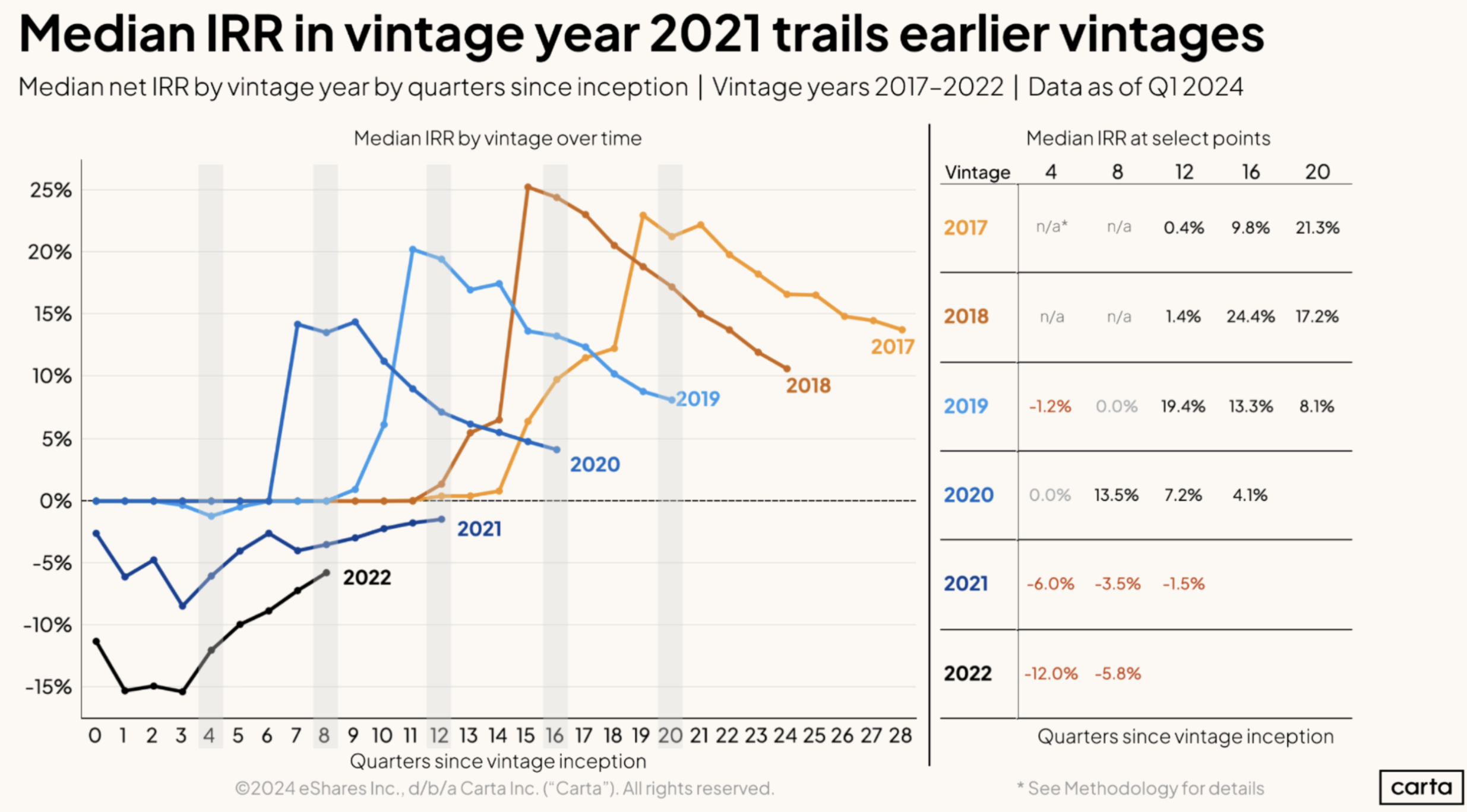

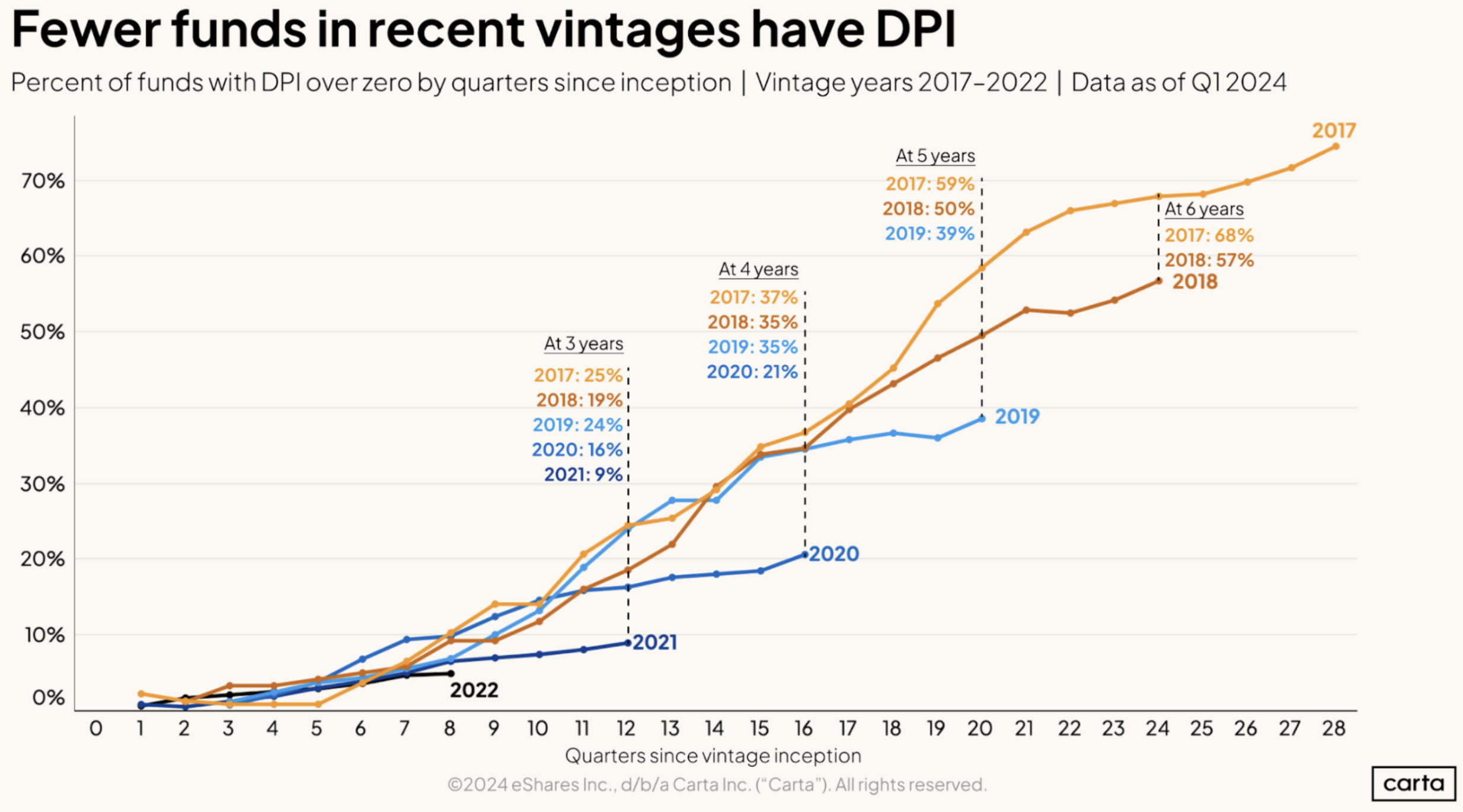

Equity management platform Carta published a detailed report on the state of venture capital through Q1 2024, and the results show that funds launched in 2021 and 2022 are not having a great time. Check these two slides from their report showing median internal rate of return (IRR) and distribution to paid-in capital (DPI) for different vintages over time:

IRR, which is one of the most commonly used performance metrics in venture, measures the returns of a fund while accounting for the time value of cash flows. Through 12 quarters, the median IRR of 2021 funds is negative, while the median IRR for the previous four vintages over the same time period was positive.

The median DPI for 2021 funds is even worse. DPI is the ratio of capital paid out to investors vs. what they invested, and through three years, 2021’s median DPI of 9% is less than half of the median DPI for 2017-2019 funds, and seven percentage points off from 2020.

The TL;DR is that younger funds are underperforming their predecessors by a wide margin.

Why the underperformance, and what does it all mean?

First, the 2021 market was hot, with the exit value in the US VC market hitting a record $797 billion. Thanks to a hot market, it was easier than ever to raise new VC funding, a record $128.3 billion in new venture funding was raised in the US, and 270 first-time funds were launched, the highest number in the last decade.

However, valuations and deal volume collapsed beginning in 2022 as the fed began raising interest rates, with exit value in the US venture market falling from its $797 billion peak in 2021 to just $61.5 billion in 2023. As valuations collapsed, many startups needing new funding were forced to raise down rounds, or funding rounds at lower valuations, and Carta noted that in Q1 2023, almost 20% of all venture investments were down rounds, vs. 5% of deals in 2022.

While funds raised prior to 2021 benefited from high-priced exits in a hot market, funds that launched in 2021 and 2022 have seen their returns struggle as they began deploying capital at market peaks. The biggest losers of this trend are the first-time funds who raised in 2021. While mature firms, who likely exited positions at the market high of 2021, can point to their multi-year track records when raising new funds, first-time venture funds are being judged on their current funds’ performances. Limited partners who invest in first-time venture funds want to see returns before committing to a new fund, and, unless returns improve for 2021 and 2022 funds, many of these first-time funds will struggle to raise new funding in the future.