How do you want to pay?

It’s never been more confusing to pay for something

Cash is still king… except when it’s forbidden

Last month, Target announced it would stop accepting personal checks from shoppers. For industry observers, this development felt noteworthy because, well, where else do you most imagine being stuck behind someone writing a paper check in 2024 than at a Target? In explaining its decision, Target cited the most obvious rationale: the “extremely low volume” of checks used as a form of payment by customers.

While the movement away from checks has already happened in most other places, the US had long remained a holdout among its peer nations in phasing the payment method out. At long last, though, American consumers may have finally tired of trying to figure out how and where to write zero cents. A rigorous look at Federal Reserve data by Professor Jay Zagorsky earlier this year shows just how precipitous the decline in check-writing has been over the past few decades: “In 2000, the average American wrote roughly 60 checks cleared by the Fed each year, compared with about nine today.”

It’s hard not to love a story about the moment when a standard feature of consumer life truly becomes obsolete. Who doesn’t marvel at a fax machine or a phone book when they catch one in the wild? But even as the steady demise of paper checks leaves etiquette experts to debate whether it’s tacky for engaged couples to add their Venmo handles to their wedding websites, perhaps a better way to think about this story is less about the tangible virtues of checks and more about the fracturing of the payments ecosystem. To be an American consumer these days is to be split between priorities and preferences, benefits and penalties, when it comes to how you pay for everyday goods and services. It’s become an increasingly confusing world where a growing number of payment formats — be it cash, credit, prepaid cards, apps, and yes, even checks — have their specific place and time.

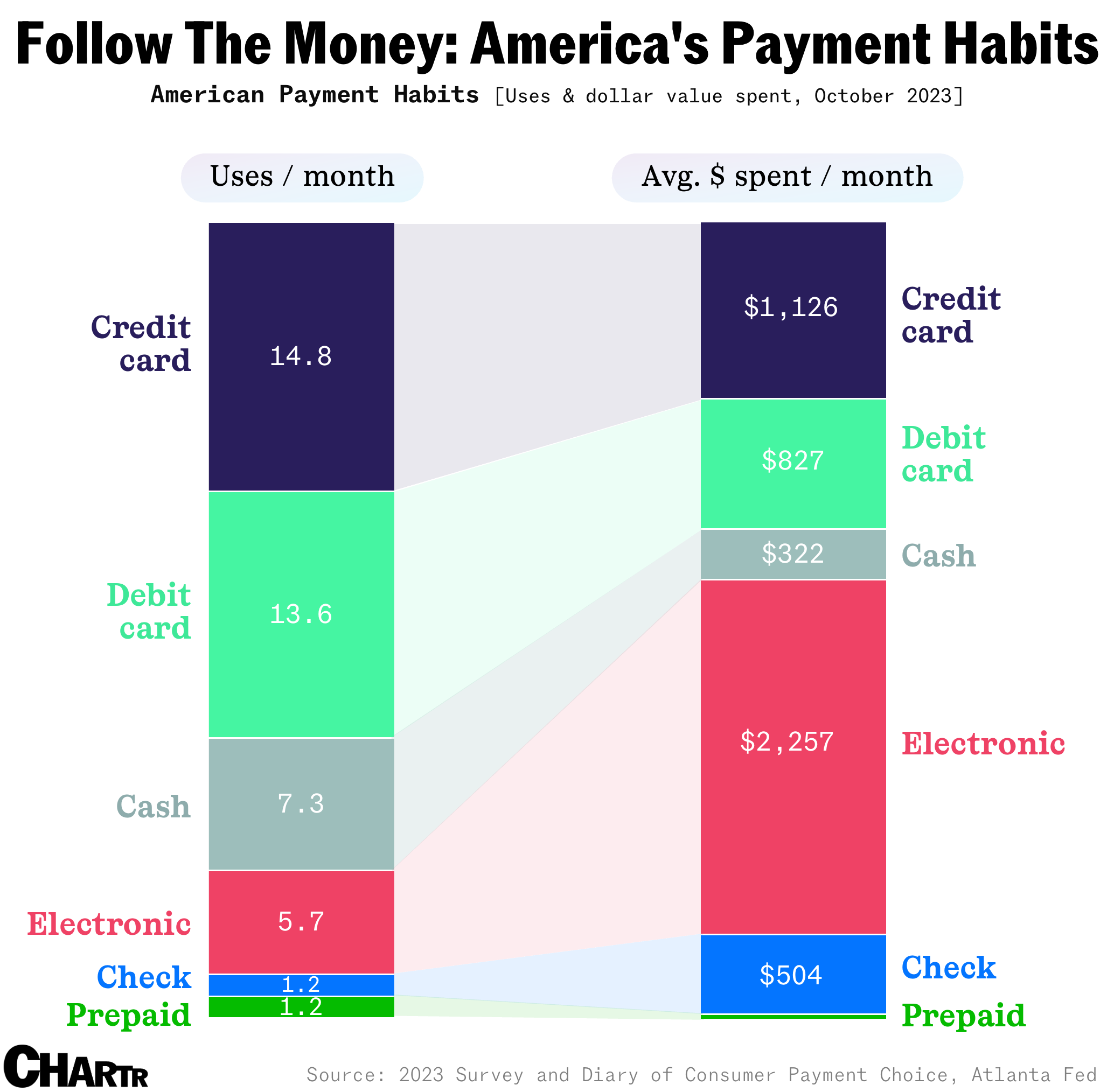

Just before the elegies for the paper check started pouring in last month, the Federal Reserve Bank of Atlanta released its latest round of consumer data, which shed some light on how American consumers make purchases in this variegated landscape. Among many surprising finds is the revelation that checks still aren’t totally dead. In October 2023, the average US consumer wrote 1.23 checks, reserving them mostly for bigger-ticket bills and items: the average amount spent by check that month was about $504 in total. Meanwhile, that same month, the average American used cash — another payment method on some death watch lists — in 7.3 transactions, at an average rate of $44.11 per transaction.

Another compelling discovery from the Federal Reserve had to do with prepaid cards, which are apparently most popular at the opposite ends of the income-level spectrum. In October 2023, only consumers with annual household incomes under $35,000 and over $125,000 appeared to use prepaid cards more often than the national average. For wealthier users, the appeal of a prepaid card can be seen in gifting, the ability to control spending, or the relative ease of reloading a card at various retail stores instead of a bank. For lower-income groups, on the other hand, a reliance on prepaid cards can often be a reality of being unbanked or underbanked, as well as the nature of payroll trends in low-wage industries.

Of course, many of our payment behaviors are ingrained. A 2023 survey by Pymnts found that 40% of US consumers still carry cash around, with older Americans predictably leading the way, though Gen Z, likely because they’re too young to have credit or debit cards, are nearly equally likely as boomers to have cash on hand. The biggest reasons given for the decision to carry cash were simple force of habit (20%) as well as the enduring preference to pay for smaller transactions with cash (19%).

Still, consumer tendencies aside, companies are asserting their own particular preferences in how we pay with a vigor that seems to be making a difference. While cash-only outfits once thrived, larger consumer-facing businesses have increasingly sought to rid cash from their systems. As PayPal argues (certainly with no ulterior motives in mind!), going cashless reduces theft and operational costs by relieving businesses of the “need to handle, count, or bank physical cash.” It also offers opportunities to better leverage customer data collected from digital purchases. And, of course, steering consumers away from cash is how PayPal and its ilk make their money.

But the reasons for the campaign against cash go deeper than that. In recent years, behavioral economists have repeatedly concluded that shoppers tend to spend more money when not using cash to make purchases. In fact, the neurological response to using a credit card has been compared with the effects of cocaine on a person’s dopaminergic reward center.

Shopping highs aside, some Americans haven’t taken the crusade against cash lying down. In 2019, the $15 salad purveyor Sweetgreen walked back its policy of not accepting cash in its stores following criticism from data-privacy hawks as well as advocates for the tens of millions of Americans who are unbanked or underbanked. Indeed, as more cashless businesses have opened and spread, they’ve often been shadowed by emerging laws in cities and states that require all businesses to accept cash. The pro-ATM lobbying group ATMIA notes that nine US states and four major cities have passed bans against cashless businesses, with similar legislation proposed in a handful of other places. (In a corresponding bummer, it’s never been more expensive to use an out-of-network ATM.)

Of course, industries that are desperate (and deep-pocketed) enough to move away from cash will always find the loophole. For example, despite NYC being one of the cities requiring businesses to accept cash, Yankee Stadium, like nearly all major sports stadiums, has forbidden cash transactions at its concession stands, leaving international tourists or old-school fans without a form of digital payment to use one of the stadium’s cash-to-card kiosks to turn their paper into a prepaid card. Having to mind and maintain these diminutively named “reverse ATMs” may seem like it would defeat the purpose of accepting just cash, but according to data from Visa, the effort to rid paper money from America’s pastime is worth the trouble: stadium-goers spend 25% more at venues where they’re steered away from using cash.

Ultimately, it would be simpler for everyone if payment trends all pointed in the same direction. Yet, as the goliaths continue to move away from cash, mom-and-pop stores around the country are embracing it anew. With merchant transaction fees on the rise — no doubt boosted by the credit-card-points industrial complex — more small businesses have started offering discounts for cash payments to lure thrifty consumers back into using paper money. The growing pay-with-cash movement goes way beyond the credit-card surcharges that drivers often see when standing at the gas pump. According to research by the Federal Reserve Bank of Atlanta, the share of all purchases that came with a discount for using cash climbed 66% between 2015 and 2022. In other cases, whether it’s a generations-old corner store or a new cannabis dispensary without access to traditional banking, many businesses are simply holding fast to the cash-only model.

In many ways, the great payments divergence is another symbol of an era where facets of consumer life, from information to entertainment, have gone from standardized and bundled to a decentralized mishmash. The result is a habitat where you can't always predict what's going to be the preferred way to pay when you stumble into someplace new. Personally, I’m banking on a big comeback for tulips.

Adam Chandler is a journalist based in New York and the author of Drive-Thru Dreams. His next book, 99% Perspiration, will be published in January 2025.