Grayscale: Tariffs and inflation could be good for bitcoin

“Tariffs are a shock to equities, not bitcoin.”

Tariffs and inflation are not bad for everything, according to a Grayscale report that argues both can actually be beneficial for bitcoin. As the manager of one of the biggest bitcoin ETFs, Grayscale Bitcoin Trust ETF certainly has skin in the game, but the report found some interesting data points to support its thesis.

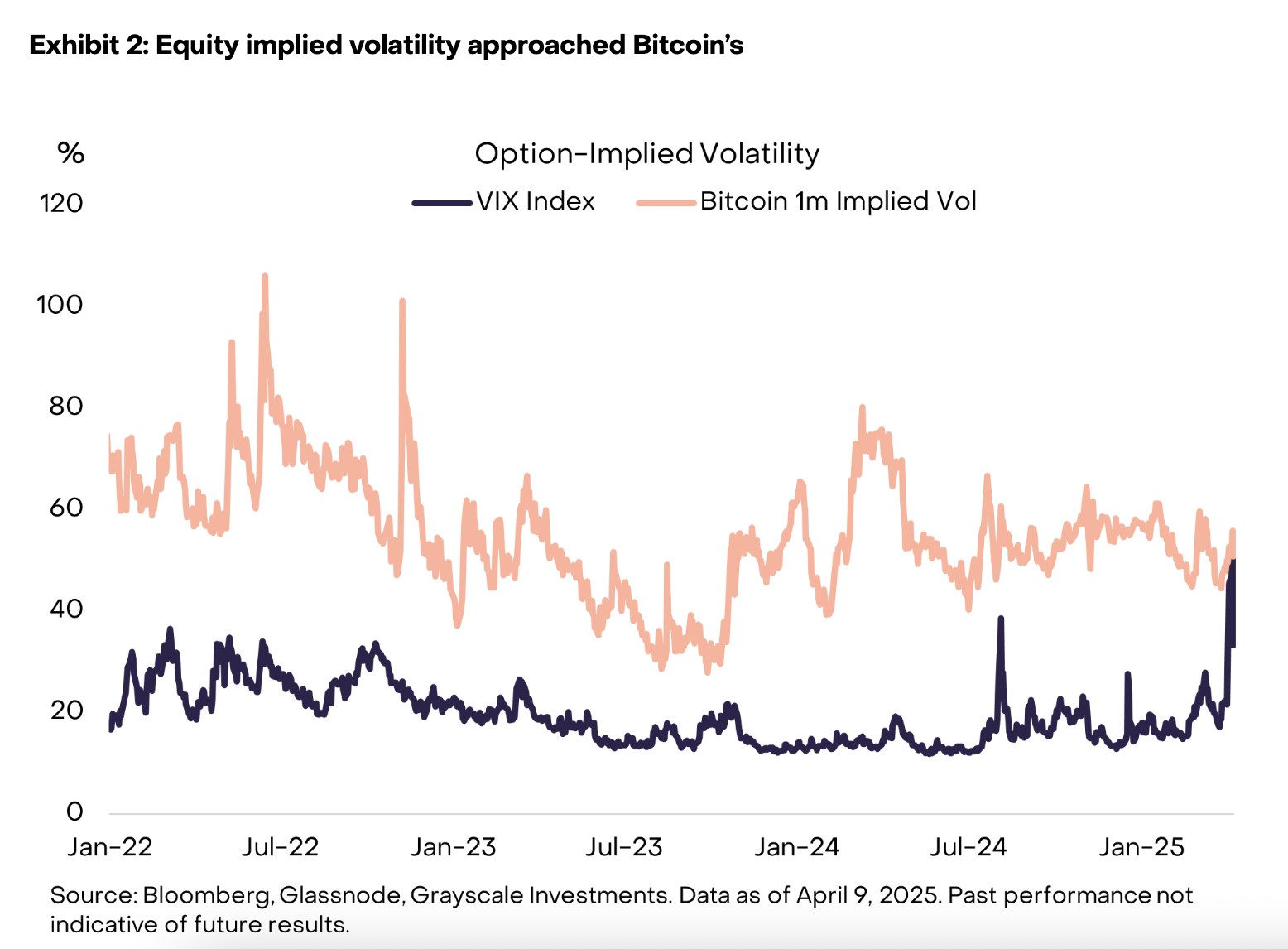

Grayscale head of research and the report’s principal author, Zach Pandl, wrote that bitcoin’s drawdown is less than one-third of what might be expected given the decline in equity markets and bitcoin’s typically higher volatility (though it has moved in step with equities this week).

Grayscale analysts argue that while the price dropped since the reciprocal tariffs announcement on April 2, “trade tensions will ultimately be positive for bitcoin adoption over the medium term.”

“Tariffs are a shock to equities, not bitcoin: the VIX is now at a level comparable to bitcoin option-implied volatility,” Pandl said. “In a nutshell, bitcoin’s price is down, but our conviction in its medium-term outlook has never been higher.”

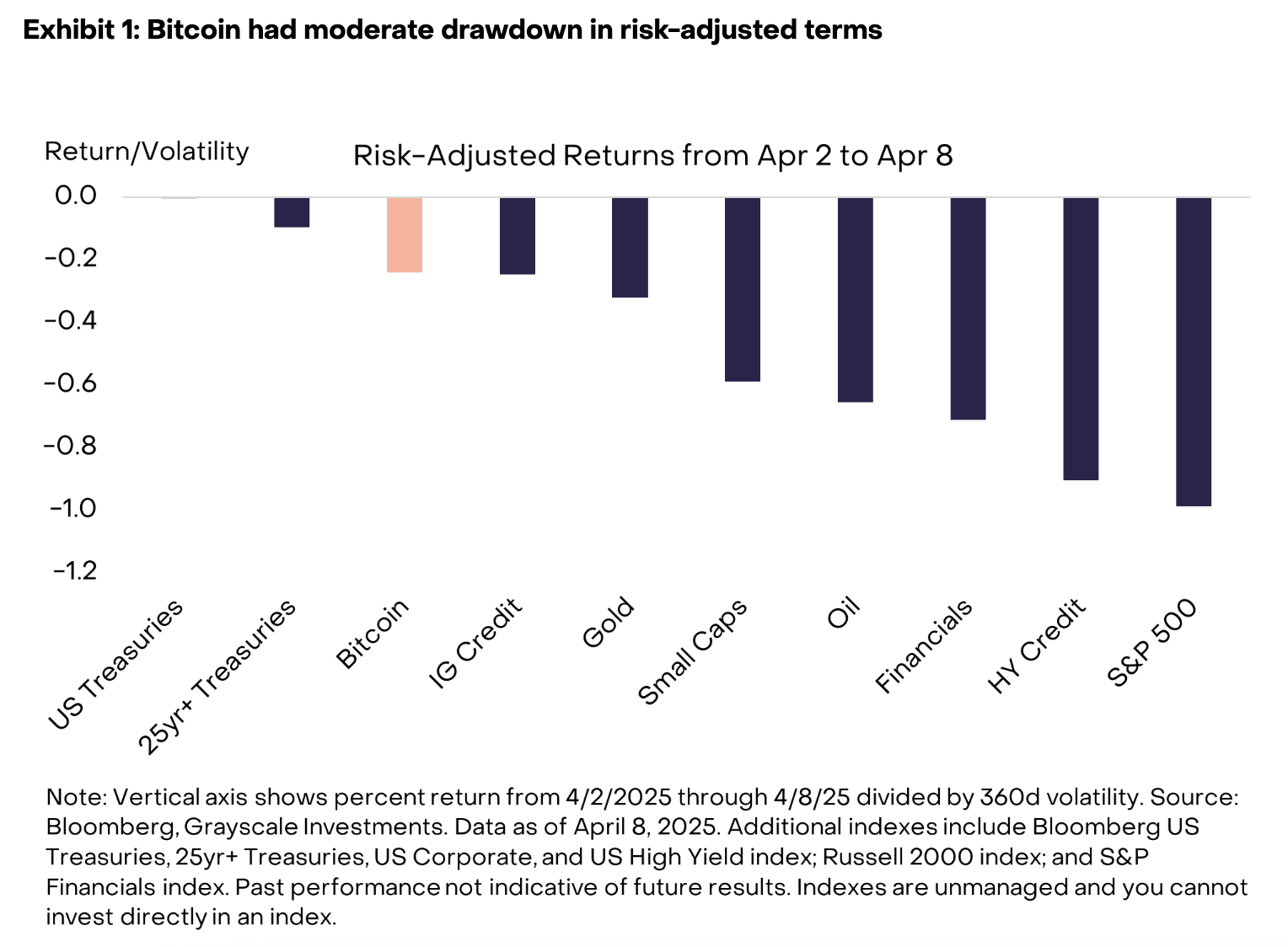

According to the report, from April 2 to April 8 (pre-90-day pause announcement), the S&P 500 declined 12%.

“Bitcoin’s price volatility is typically around three times higher than the S&P 500. Therefore, if Bitcoin had a 1:1 correlation with equity returns, the decline in the S&P 500 would have implied a 36% drop in the price of Bitcoin,” the report reads.

Following President Donald Trump’s announcement of a 90-day tariff pause on most countries yesterday, bitcoin, which started the day at about $76,000, jumped to over $82,000. (It’s still down 26% from its all-time high of $109,114 on Inauguration Day.)

Tariffs may also further weaken the US dollar, the report adds, boosting bitcoin’s appeal as a store of value.

Opinions vary regarding how the economic uncertainty and the dizzying pace of the administration’s tariff announcements (and enactments) could affect the crypto market and bitcoin’s trajectory.

Today’s CPI figures, which came softer than anticipated, didn’t budge bitcoin’s price. Nic Puckrin, founder of Coin Bureau, said that this suggests investors may be too shell-shocked after yesterday’s tariff announcement.

Puckrin added that bitcoin holding steady above the $81,000 resistance line after yesterday’s rebound is a positive sign.

“However, the jubilance needed to push it into a more sustained rally past $88,000 and then $93,000 just isn’t there,” Puckrin said. “The 90-day tariff reprieve doesn’t spell the end of the trade war — it’s simply kicking the can down the road.”

And any setback would send markets hurtling back into correction territory, he added.

“It’s not unusual to see such huge moves during the last stages of a bull run,” he said, “but it makes any short-term trading decision more akin to gambling at this stage.”