Earnings season has been phenomenal, and it’s done nothing for the average stock

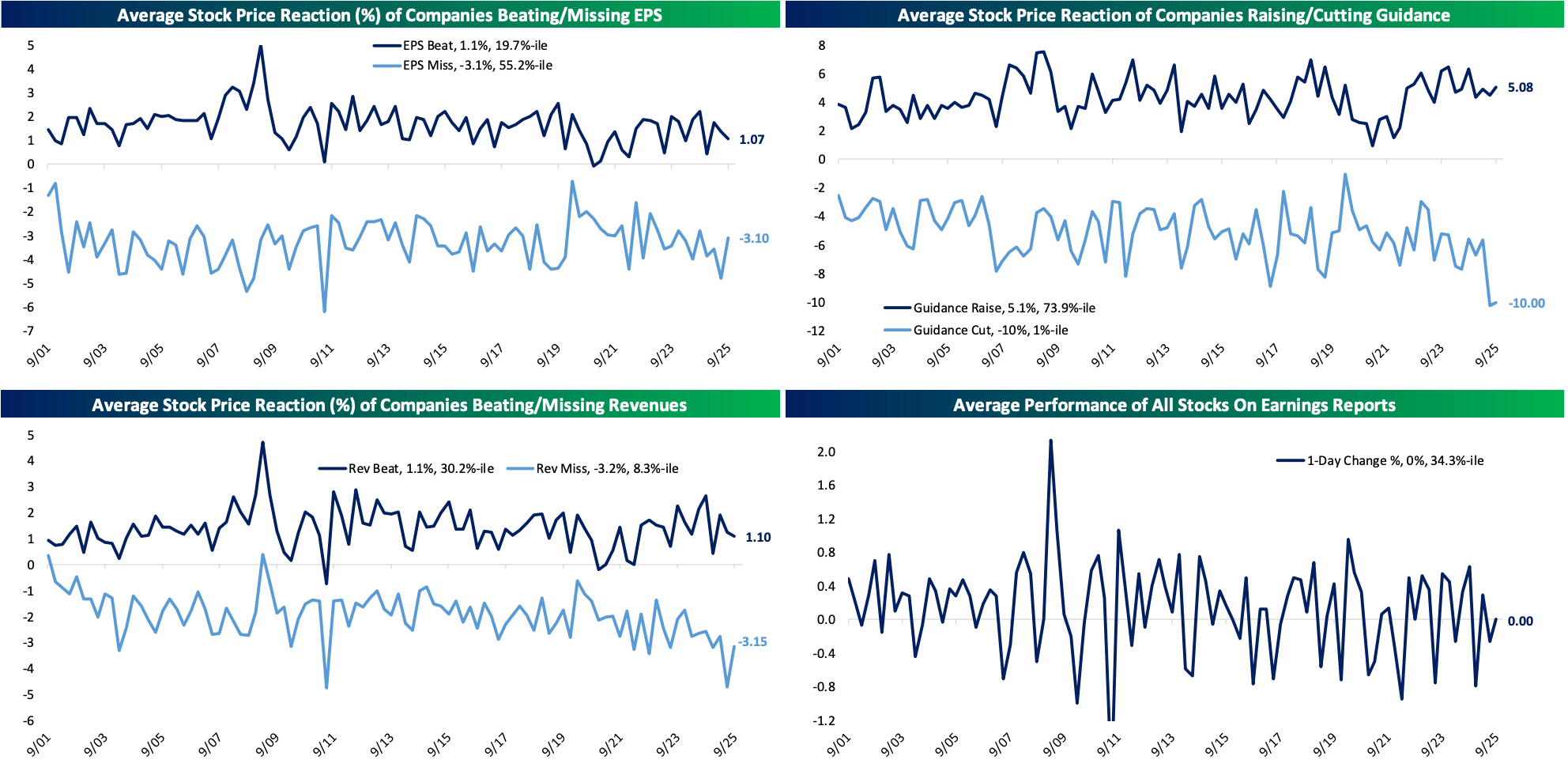

“The average stock has not moved on earnings this season, which is on the weaker side of the historical distribution,” writes Bespoke Investment Group.

Earnings season has been stellar. Traders’ reactions to earnings have been anything but.

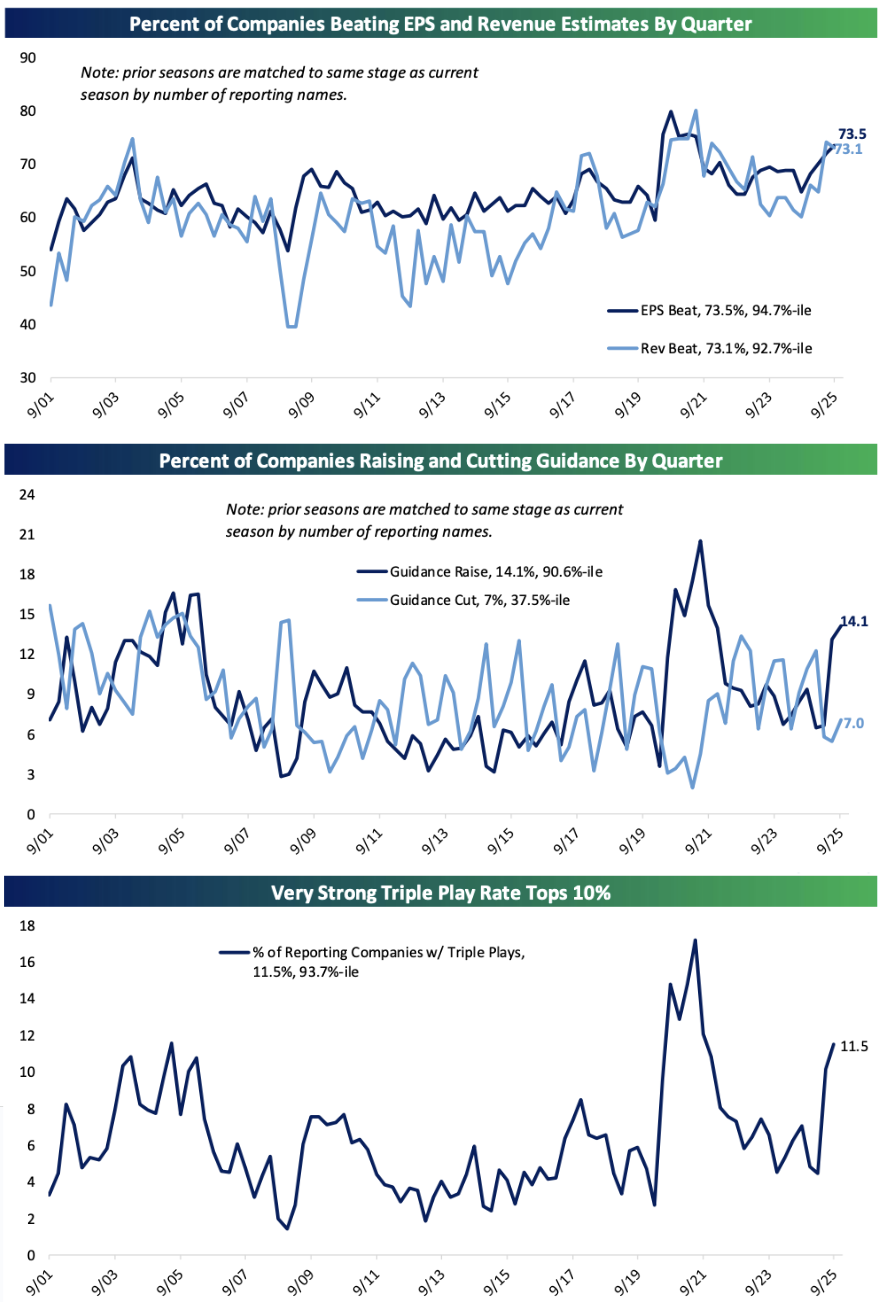

Bespoke Investment Group has an excellent series of charts spotlighting just how positive this third-quarter corporate reporting period has been, with exceptional beat rates and guidance hikes across US stocks:

However, despite 73.5% of companies tracked by Bespoke beating on earnings per share this quarter, the analysts noted that earnings reactions have “been a completely different story.”

In particular, earnings beats have been rewarded with tepid gains, and companies that lowered their outlook were severely punished for a second consecutive season.

“The average stock has not moved on earnings this season, which is on the weaker side of the historical distribution,” they added.

If I had to explain why stocks haven’t responded positively to robust results with guidance to match, I’d turn to the recent past.

Ahead of earnings season, September was the third-best month of 2025 for the SPDR S&P 500 Trust, trailing only the May and June recovery from the tariff-induced meltdown in markets and subsequent softening of trade tensions. The three-month growth in 12-month forward earnings per share ahead of earnings season (4.9%) was the strongest it’s been since 2021, when corporate profitability was getting a powerful boost as economic reopening was met by consumers flush with excess spending power.

While these are still more the exceptions than the rules, you can point to episodic examples of stocks that were on an absolute tear into Q3 earnings — Palantir and Micron come to mind — that posted beats and raised guidance only to drop in the wake of these results. The combination of how well stocks had done heading into this reporting period and how much forward expectations were getting revised higher provided a very difficult bar to clear, and made it much more punishing for those who came up short.

In other words, a strong Q3 earnings season... was priced in.