Jay got his way

It sure looks like the top US central banker put his thumb on the scale to get a 50 basis point cut today.

To adapt the hackneyed expression, personnel is monetary policy.

That was on full display with today’s 50 basis point rate cut from the Fed in a decision that was hotly debated and not everyone in the room agreed with.

In some respects, this outcome really seems like Chair Jay Powell getting his way.

Some context clues:

For starters, speeches from two influential members of the Federal Reserve – the New York Fed’s John Williams and Fed Governor Chris Waller – that happened just before the central bank’s “blackout period” did not provide a strong signal that the September cut would be more than 25 basis points.

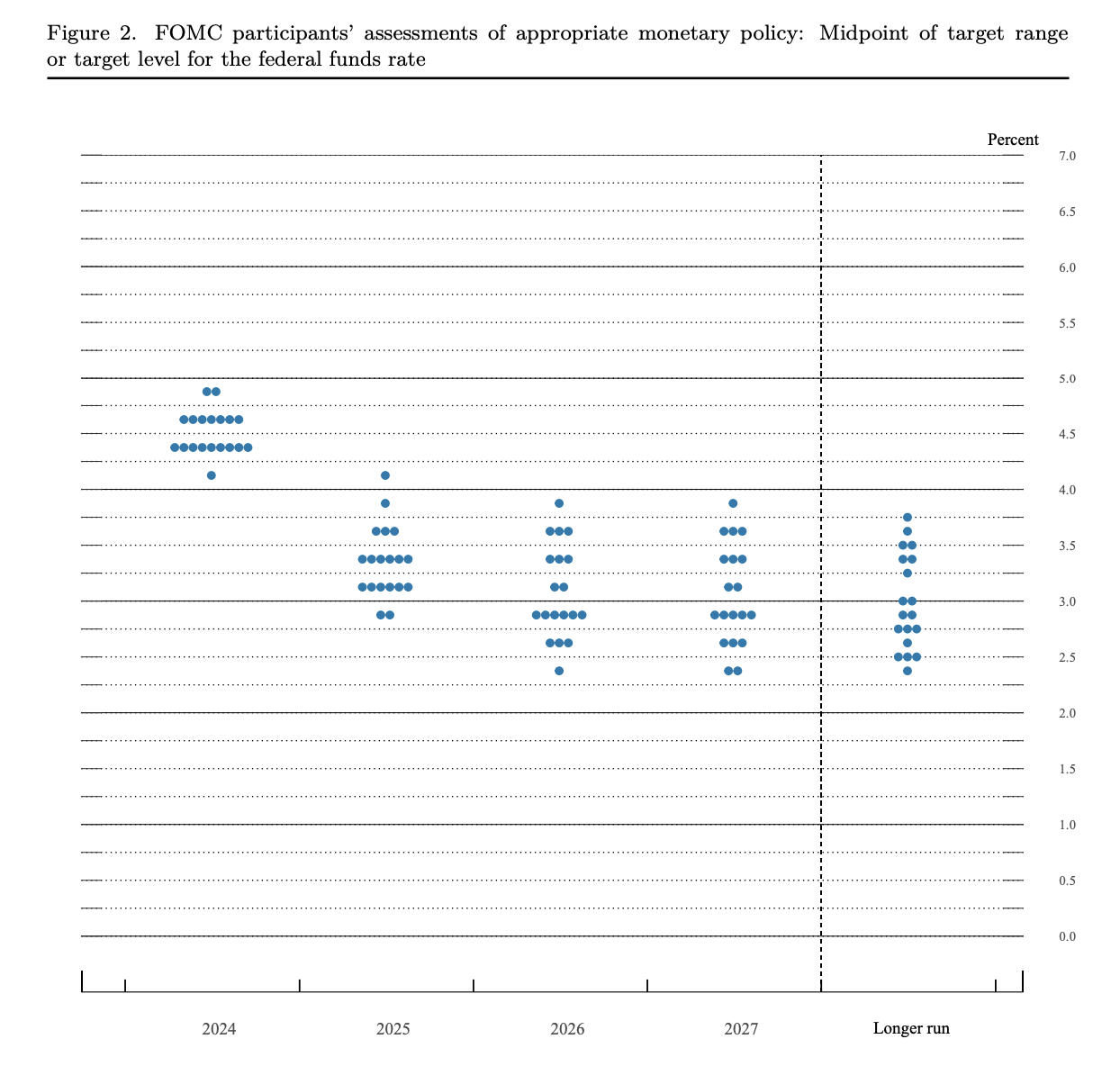

More importantly, the central bank’s so-called “dot plot” showed that 10 monetary policymakers think it will be appropriate to cut rates by at least 100 basis points or more if the economy unfolds like they expect it will. That would (likely) imply two 25 basis cuts at the two remaining meetings this year.

That still leaves a huge cohort (9 officials) who think rates should go down by 75 basis points or less this year.

And yet, somehow, only one monetary policymaker (Governor Michelle Bowman) dissented from this decision in favor of a smaller rate cut.

Since there are 12 voting members, there’s at least one person today who voted for a 50 basis point cut and doesn’t think it will be appropriate to cut rates at one of the two final meetings of 2024. And that same person also thinks rates should be lowered over the course of 2025. Riiiiiiiight. That makes no sense; it’s wildly incoherent, incongruent combination.

This, to me, is the kind of thing that can be best explained by someone in a position of authority putting their thumb on the scale. “You can have your opinion, but I must have my outcome” is the subtext running through today’s interest rate decision and summary of economic projections.

It’s the easiest way to reconcile everything that happened. I’m sure this wouldn’t be the first time in recorded human history that someone did something they didn’t want to do because their boss really wanted them to do it.

Former Fed Chair Alan Greenspan was famous for engineering his preferred result in a relatively heavy-handed manner; his successors have tended to be more consensus-oriented.

And at the risk of being an armchair psychologist, Powell seemed much more comfortable during this press conference than he was during his last one.

Back in July, he was trying to thread the needle of saying that it was good the labor market was losing momentum, but didn’t want it to lose any more momentum... and still wasn’t cutting rates.

It was a lot easier for him to rationalize the Fed’s decision this time around. In addition, he said the central bank “might well have” cut interest rates in July had it known how soft the job report (released two days later) was.

“The labor market is actually in a solid condition, and our intention with our policy move today is to keep it there,” Powell said. “You can say that about the whole economy, the US economy is in good shape, it’s growing at a solid pace, inflation is coming down, the labor market is in a strong place, we want to keep it there, that’s what we’re doing.”

The man is likely at his most comfortable when he’s getting his way and taking action to try to keep a good thing going. And honestly, aren’t most of us?