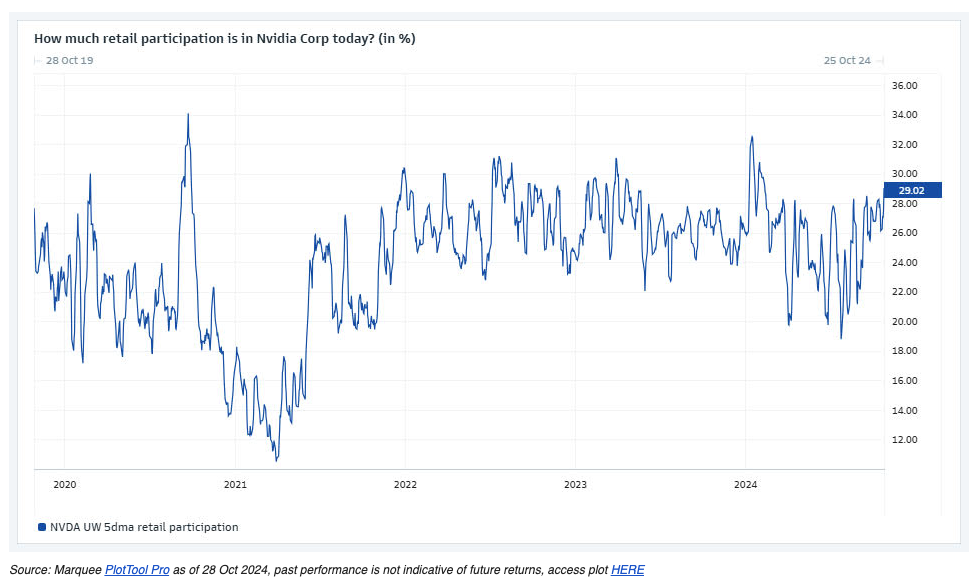

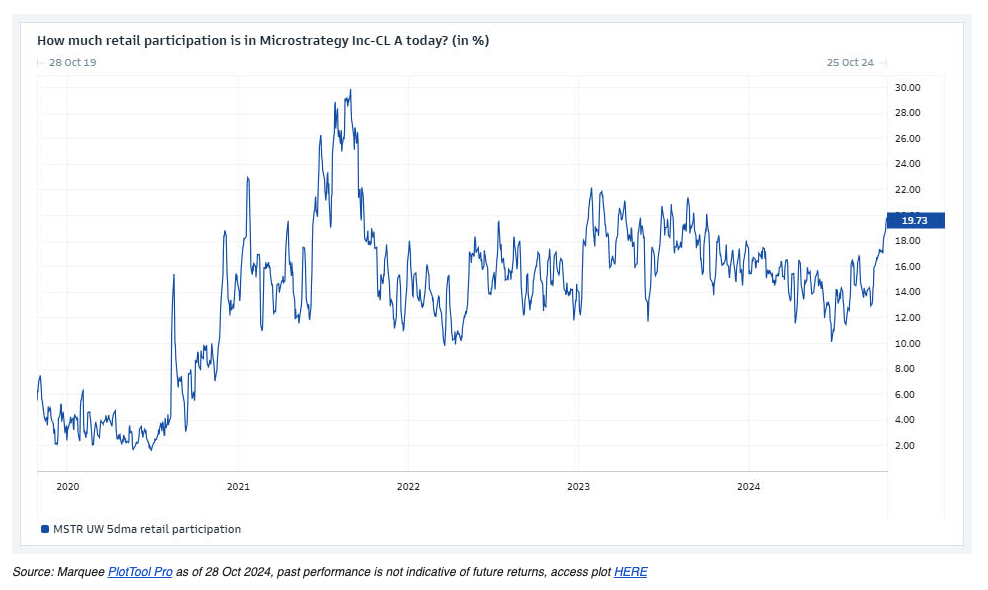

Retail traders are getting bulled up on Nvidia and Microstrategy

One potential reason for Nvidia’s massive outperformance of its peers and Magnificent 7 stocks.

In Scott Rubner’s recent note, the Goldman Sachs managing director laid out the case for stocks to ramp up into year-end, highlighting the immense support coming from corporate share repurchases. But he also flagged another class of buyer that’s been flexing its muscles lately.

“I am noticing that retail activity on the message boards has started to increase again,” he writes. “Keep an eye on this cohort via options and ETFs.”

According to data from Goldman’s Marquee platform, retail participation in Nvidia is at its highest since the start of the year and at the hottest level of 2024 for bitcoin proxy Microstrategy.

We recently flagged that Nvidia has been massively outperforming its peers (and the rest of the Magnificent 7, at least before Tesla’s blowout earnings) as of late — usually the kind of thing that happens when it’s about to deliver a huge quarterly report (or just did). Rubner’s observation on the return of enthusiastic retail buyers offers one good explanation for why the price action has played out this way.