Three reasons why investors are brushing off Trump’s tariff threats

If the president-elect really cares about the stock market, investors wager the pro-growth policies will come before trade tensions escalate.

The big stock-market news of the day is what’s not happening.

After President-elect Donald Trump posted messages on Truth Social warning Canada, Mexico, and China that they’d face across-the-board tariffs if their politicians didn’t stop the flow of people and drugs into the US, the stock market is… up.

Levies of 25% on Canadian and Mexican imports and 10% on China would be a more impactful trade policy than anything Trump pursued during his first term in office.

So why are stock-market investors seemingly shrugging this off? I can think of three potential reasons.

Investors either:

Are unwilling to price in Trump policies that are negative for the stock market, given his focus on that as a yardstick;

Think any “sticks” in the policy agenda won’t be on the horizon until after the “carrots”;

Or remember that the 2018 trade war was not really the proximate cause of the weakness in stocks that year.

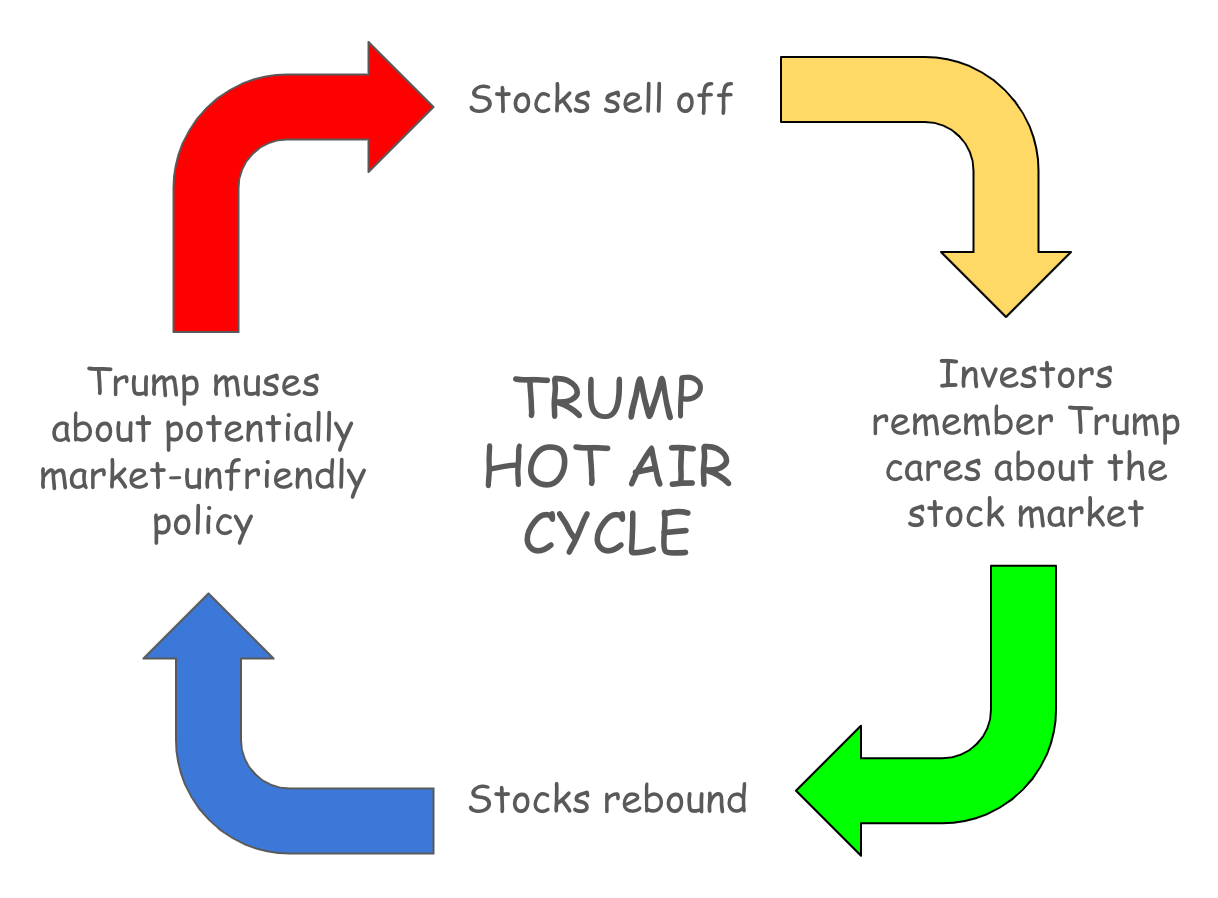

Hot-air cycle

Market participants don’t just think of Trump as the incoming POTUS. He’s also the SOTSAP: Steward of the S&P 500.

Over at Bloomberg, Joe Weisenthal has discussed the idea of “stock market vigilantes.” To summarize, politicians have their policy options constrained by Americans who are either indirectly or directly equity owners and need those asset values to rise to feel comfortable about their current and future financial situations.

Right now, investors are left in a bit of an information vacuum. Reasonable and intelligent people can (and do) disagree on whether this is merely a negotiating ploy, something that has a high likelihood of being carried out on January 20, and what, if any, remedies might be needed to avoid it. The stock market’s initial verdict seems to hinge on the memory of a low follow-through rate on policy announcements made through social media during Trump’s first term.

“We (continue to) believe that Trump will not implement these tariffs on day 1, as the pain to the US economy would be too great (as Trump himself recognized during his first term, in walking back his then similar threat),” Andrew Bishop, global head of policy research at Signum Global Advisors, said in a note.

“Trump linking tariffs to drugs and immigration, rather than trade policy/FX/economics signaled to investors that this announcement is a negotiating tactic,” 22V Research chief market strategist Dennis Debusschere said. “Not a policy tool.”

But if you subscribe to the “stock market vigilante” thesis — and add on to that the memory of the Trump administration looking at the stock market as a real-time report card — that leaves you in a bit of a tricky position. The rational move is to buy any dip from a policy announcement that might be bad for the markets out of a strong belief that the administration won't follow through with it simply because of the negative market consequences. Effectively, it’s conditioning investors to react late to negative catalysts.

This is a miniature version of Hyman Minsky’s “stability breeds instability” argument, and the ensuing “Trump Hot-Air Cycle” looks a little something like this:

What’s needed to break this cycle? Well, action that everyone was warned about but no one thought was coming, probably.

Opening sequence

What this may be for investors is a bit of a shot across the bow, a wake-up call when it comes to policy sequencing. There is an embedded presumption, based on Trump’s first term, that he will pursue market-friendly and pro-growth policies to “prime the pump,” so to speak, ahead of more disruptive measures on trade.

The landmark policy achievement in 2017 was the Tax Cuts and Jobs Act, which caused earnings estimates and major stock indexes to explode higher at the beginning of 2018. Afterward, tariffs moved to the front of the agenda. With that framing in mind, it’s not overly surprising that the market reaction to the election has largely been “price in good things — M&A! Deregulation! Maybe even more tax cuts! — first, and don’t worry about potential bad things until the good things have happened.”

Well, Monday’s truth bomb suggests that policy priorities may be different this time around.

“Our overall read is that tariffs are clearly at the top of the Trump agenda,” wrote George Saravelos, global head of FX research at Deutsche Bank. “We see an implicit signal that they are likely to be used as a broad-based economic and geopolitical tool in this Administration.”

Relitigating 2018

Here are the facts: US stocks went down in 2018. They went down by less than global stocks. And more domestically oriented US companies performed better than those without lots of international exposure. Unsurprisingly, US stocks with a high share of sales to China did the worst.

It’s possible to look at this picture, say “trade war!” and be done with it. But you can also explain much of this price action through macroeconomic trends that are largely independent of trade policy.

To oversimplify, stocks fell in 2018 as the profit outlook dimmed. The trade war was negative for the stock market through the announcement effects (simply, bad news = sell stocks) and because it was a contributor to the rise in the US dollar, which hurts multinationals’ earnings power.

However, the greenback’s rally was more complicated than that: policy-rate differentials between the US and other countries were growing because the Federal Reserve was hiking rates amid stronger domestic growth and inflation outcomes.

That’s the positive US dollar story reinforced by a negative story for the rest of the world: a lackluster environment for global growth due to a lack of fiscal policy support in Europe and especially China. That Chinese economic slowdown in 2018 was much more a function of internal choices — dialing back on its credit-supported growth model — than external forces.