How tech companies became the source – and death – of US stock market volatility

Tech stocks contain multitudes

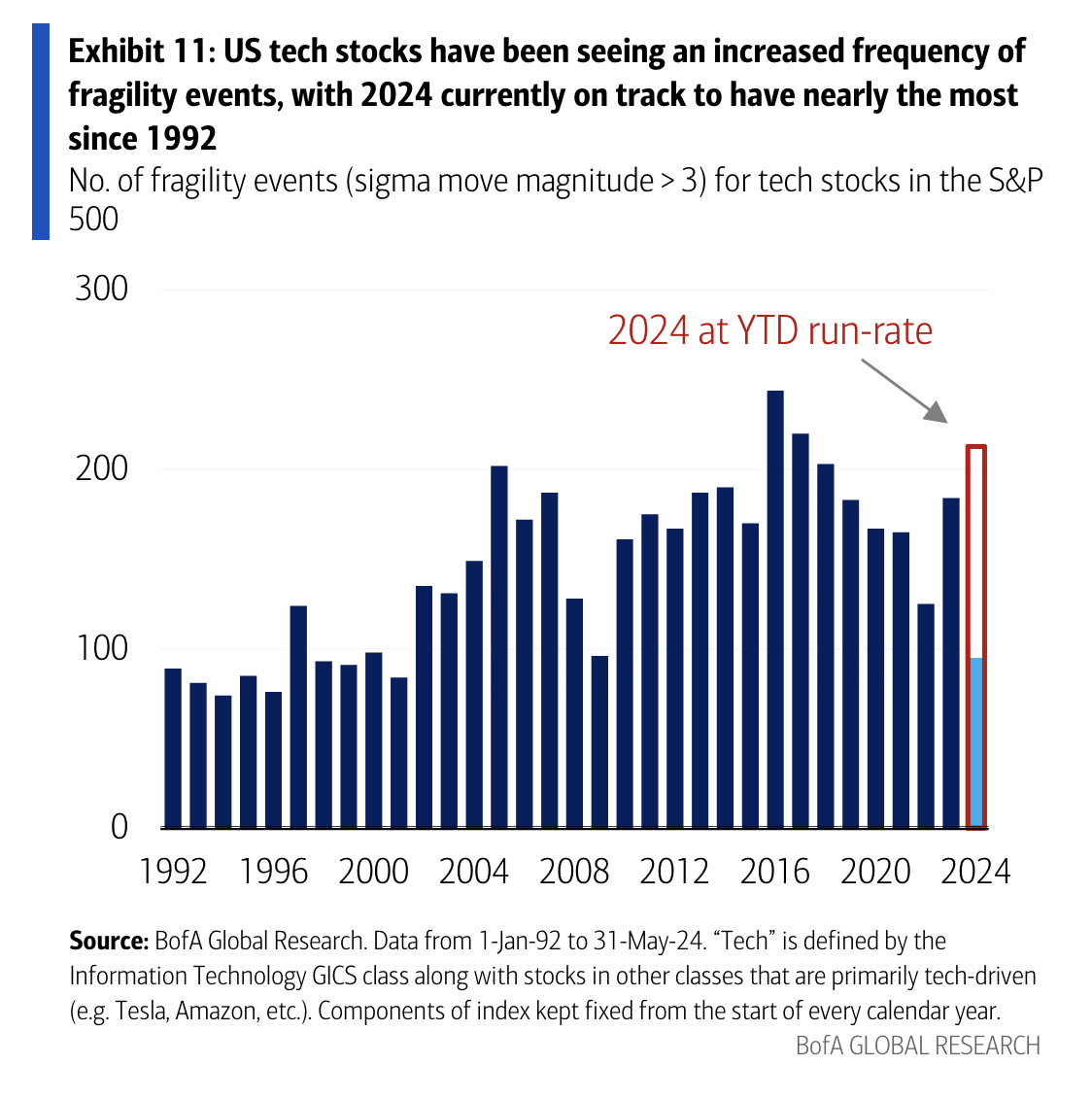

Wall Street: “2024 is on track to have one of the highest numbers of fragility events among US tech companies since 1992.”

Also Wall Street: The behavior of the five tech megacaps atop the S&P 500 has created a “motionlessness” stock market.

These two seemingly contradictory ideas can both be right!

Let’s tackle the first: it’s true that, on an individual level, certain tech stocks have had huge daily swings to the upside or downside.

“Salesforce and Dell experienced historic earnings-related moves last week, the latest examples of US Tech stocks exhibiting outsized jumps or price fragility,” write Bank of America analysts led by Benjamin Bowler. “In fact, such fragility shocks for Tech/US megacaps are near 30-year+ extremes today, both in terms of frequency and magnitude.”

BofA deems it a so-called fragility event if a stock’s daily move is three times larger than its 21-day trailing realized volatility. In my view, this is a rather expansive definition, and periods of low volatility punctuated by hiccups can create these fragility events. Under this metric, a bump on the plains can appear more momentous than another incline on a mountain.

The analysts note that the extreme price moves this year have even been witnessed among the megacaps like Nvidia, Alphabet, and Meta.

On the other hand, different major groups within the US stock market have been marching to the beat of their own drummers recently, and this dynamic has helped keep the stock market from lurching violently to the downside.

Dean Curnutt, CEO of Macro Risk Advisors, takes this one step further and flags that even within technology giants, the components aren’t moving in unison.

“Stocks are zigging and zagging in a way that is unique even adjusted for a bull market,” he said on the Alpha Exchange podcast.

This is true for the top five constituents: Microsoft, Apple, Nvidia, Alphabet, and Amazon. The average pairwise correlation between members of this group – loosely speaking, their tendency to move in the same direction — is just 43% over the past six months.

To be sure, it’s a little puzzling that correlations among these constituents are so low, given three of the five (Microsoft, Amazon, and Alphabet) are spending tens of billions on AI and another one of the five (Nvidia) is reaping the benefits of those outlays.

“Today’s paltry level of realized correlation among the supercaps comes at a time when the volatility of the stocks is also quite low,” Curnutt added. “The average of the six month realized volatility levels on these five corporate beasts is just 28%, again, one of the lowest readings over the last decade.”

So while BofA has been able to pick out some episodes where tech stocks — and even the heavyweights — are putting in eye-popping moves, by and large, the daily price action in these stocks has been rather mild versus history.

These low levels of realized correlation among major S&P 500 constituents are being extrapolated by market participants.

“In summary, option prices are really low because the motionlessness of indices like the S&P demands that be the case,” concludes Curnutt.

While BofA concedes that, to date, significant individual stock swings haven’t had major ramifications for the market as a whole, they think it’s just a matter of time until these massive moves in individual stocks happen in concert to the downside.

“So far, these fragility shocks have been idiosyncratic (occurring on different days), however, the risk is of a correlated shock among these companies that control so much of US as well as global equity indices,” they write. “Index vol continues to underprice this correlated shock risk, thus offering value as a fragility or broader market hedge.”