The trade-down trade is a market theme worth watching

Annoyingly high costs of living are driving bargain hunting and big gains for discounters.

Earnings season came to its usual, consumer-oriented conclusion over the last couple weeks, with a flurry of quarterly reports from retailers peppering the tape.

The market was clearly taken aback by some superstrong numbers from a few unsexy off-price retailers. Kohl’s mooned 24% Wednesday after posting its numbers. Burlington Stores rose a more muted 5% Thursday for the same reason, as did Five Below, which gained about 4%. Others like Dollar General and TJX Maxx parent TJX Cos. also did much better than expected, even if the stock reaction wasn’t so dramatic.

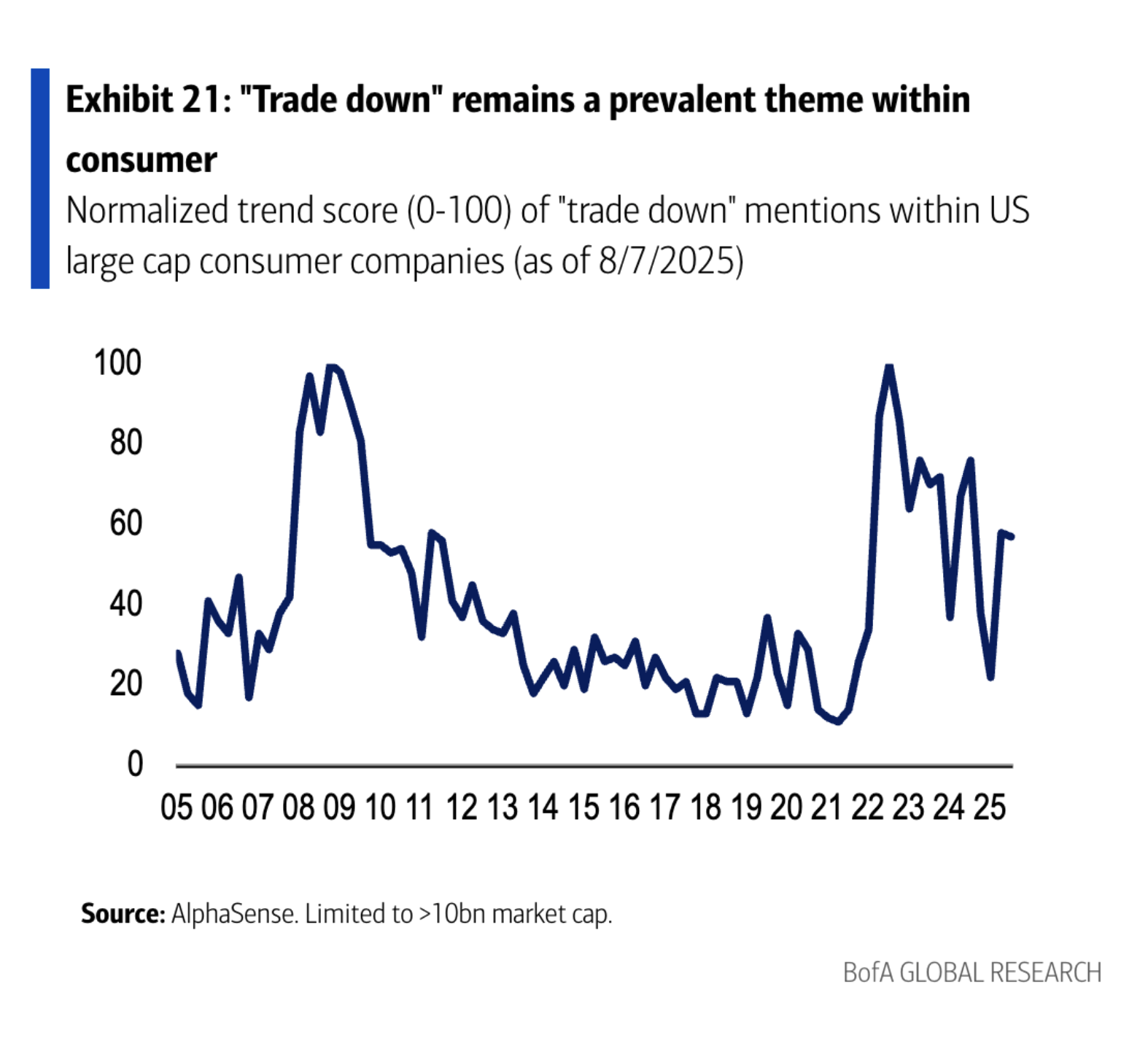

The upside wasn’t uniform — Ross Stores posted slightly disappointing sales last week, for instance — but in the aggregate, the news seemed to reinforce the message of an interesting chart published in a note by Bank of America analysts.

This trend line charts the change in mentions of “trading down” — that is, consumers shopping for lower-priced options rather than paying premium prices — on conference calls hosted by large US companies over the last 20 years.

Mentions of such behavior spiked during great financial crisis of 2008-09, and then again a decade or so later during the post-Covid inflation, as consumers saw their buying power weaken either because of job losses during the recession or because their pay didn’t keep up with price increases after the pandemic.

After a brief respite, this chart says (and the recent numbers from discounters confirm) that trading down is back.

This makes sense, as inflation remains stubbornly high. Actually it’s a bit worse than that, as inflation is actually accelerating.

The Fed’s preferred measure of underlying inflationary pressures, core PCE, hit an annual rate of nearly 3% last month, up from 2.6% back in April, according to data released Friday. It was the third straight monthly increase.

At the same time, the job market, while more or less stable, seems to be softening a bit on the margin, with the number of those receiving continued unemployment benefits rising and net employment growth decelerating, both of which make it harder to switch jobs or push for higher pay.

That might sound like an uncomfortable world for workers.

But it’s a solid backdrop for stocks of bargain retailers. Such stocks might be a decent place for risk-averse investors — if such a breed still exists — to hunt for relatively safe trades that could perform well in the high-inflation, soft-growth economy we might be looking at for a while.