It’s hard to lose money selling a $200 a month subscription, but OpenAI is doing exactly that

OpenAI is currently losing money on its newest and most expensive subscription, ChatGPT Pro, because people are using it more than the company expected, Sam Altman said in a post on Sunday.

In a series of posts on X, Altman disclosed that he “personally chose the price” because he thought “we would make some money.” Released on December 5, ChatGPT Pro offers unlimited access to the company’s latest models, including a “full” version of the latest OpenAI o1 model that can be used to “think harder and provide even better answers to the hardest questions.”

Years ago, when asked how OpenAI would make money for its investors, Altman joked — or maybe not joked — that they would “build a generally intelligent system, that basically we will ask it to figure out a way to make an investment return for you.” Clearly, they haven’t got the answer yet.

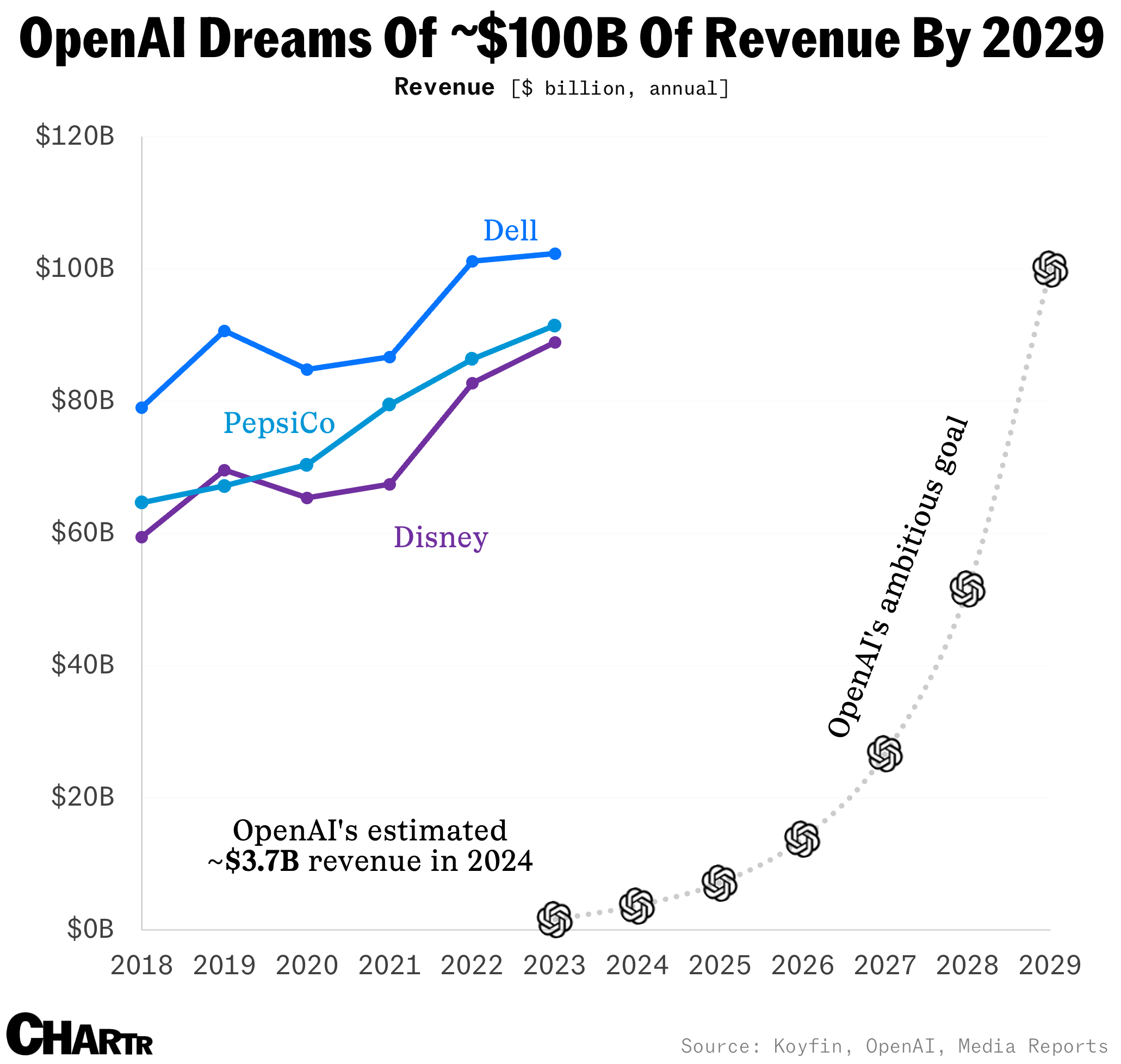

ChatGPT Pro being a money loser is the latest addition to OpenAI’s list of reasons to raise as much capital as possible. Despite being valued at a staggering $157 billion, the company is far from profitable: OpenAI reportedly expected $3.7 billion in revenue by the end of 2024, but also anticipated spending ~$8.7 billion to achieve that revenue, equating to a ~$5 billion loss.

Partly in an effort to attract investors, OpenAI has plans for a corporate restructuring and is said to be raising its subscription prices in the coming years. That would help the company achieve its lofty $100 billion revenue target by 2029, a mammoth sum which, purely in revenue terms, would be more than what Nvidia managed in its fiscal year 2024 and similar to corporate giants like Disney and PepsiCo.

Go Deeper: What company’s past reveals the future of OpenAI?

In a series of posts on X, Altman disclosed that he “personally chose the price” because he thought “we would make some money.” Released on December 5, ChatGPT Pro offers unlimited access to the company’s latest models, including a “full” version of the latest OpenAI o1 model that can be used to “think harder and provide even better answers to the hardest questions.”

Years ago, when asked how OpenAI would make money for its investors, Altman joked — or maybe not joked — that they would “build a generally intelligent system, that basically we will ask it to figure out a way to make an investment return for you.” Clearly, they haven’t got the answer yet.

ChatGPT Pro being a money loser is the latest addition to OpenAI’s list of reasons to raise as much capital as possible. Despite being valued at a staggering $157 billion, the company is far from profitable: OpenAI reportedly expected $3.7 billion in revenue by the end of 2024, but also anticipated spending ~$8.7 billion to achieve that revenue, equating to a ~$5 billion loss.

Partly in an effort to attract investors, OpenAI has plans for a corporate restructuring and is said to be raising its subscription prices in the coming years. That would help the company achieve its lofty $100 billion revenue target by 2029, a mammoth sum which, purely in revenue terms, would be more than what Nvidia managed in its fiscal year 2024 and similar to corporate giants like Disney and PepsiCo.

Go Deeper: What company’s past reveals the future of OpenAI?