A definitely real company with zero footprint made a jaw-dropping $43 billion offer to buy Paramount

Then the press release disappeared.

On July 7th, after six months of back and forth negotiations that, as recently as June, looked poised to collapse, David Ellison’s Skydance Media and Paramount Global signed a definitive agreement for Skydance to acquire the media company.

The deal was complicated. Paramount has two classes of shares: Class A voting shares and Class B common shares, and Shari Redstone’s National Amusements (NAI) owned 77.4% of the voting class shares.

Ultimately, Skydance and investing group RedBird Capital Partners agreed to invest $2.4 billion to acquire NAI for $2.4 billion, $4.5 billion (in cash and stock) to acquire other Class A and Class B shares, and add $1.5 billion in additional capital to Paramount’s balance sheet.

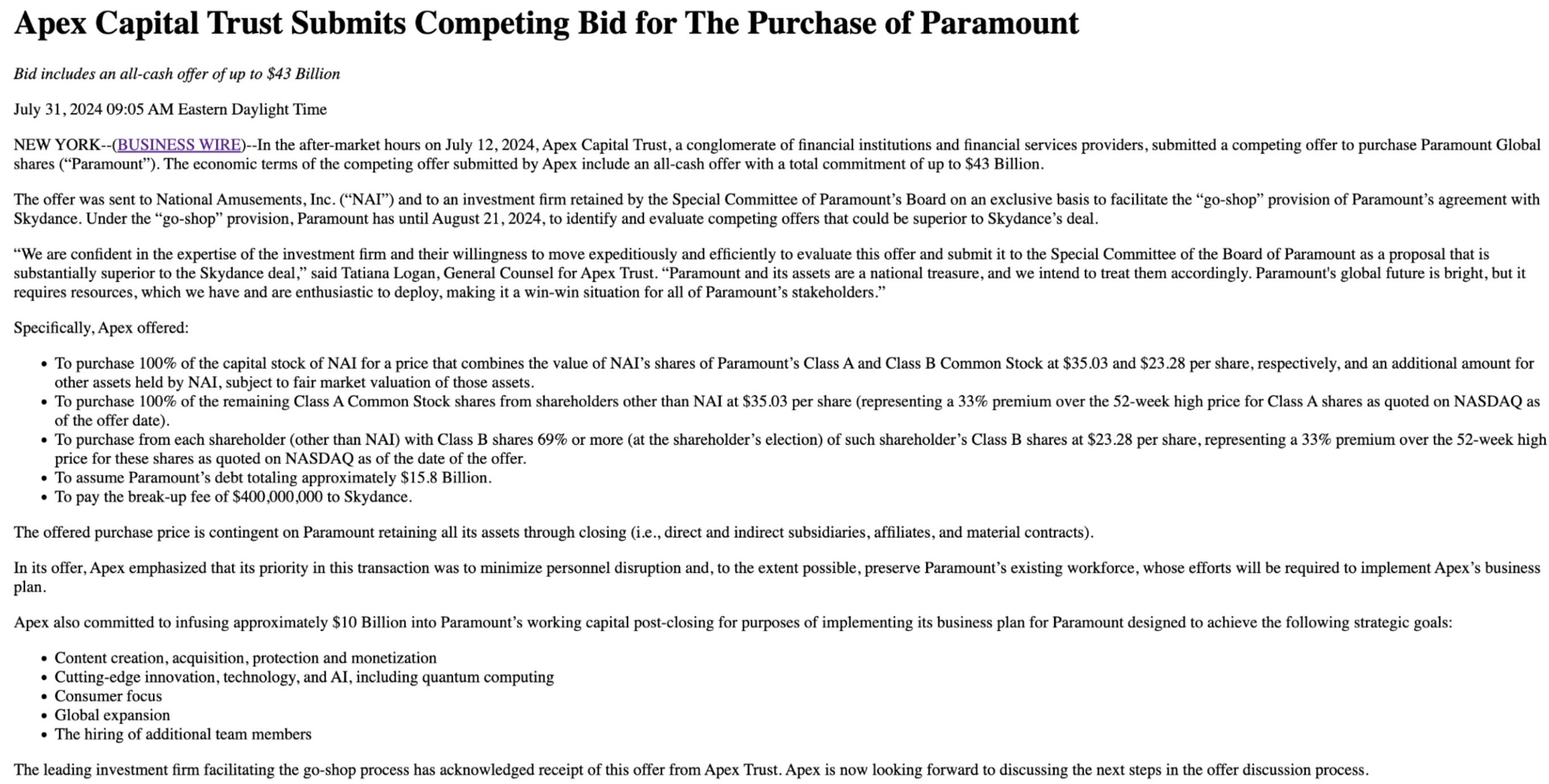

However, before the deal closes, Paramount has a 45-day “go-shop” window, allowing the company to evaluate other takeover offers until August 21. On July 31, a press release came across Business Wire that said a company called “Apex Capital Trust” made an upsized offer to acquire Paramount, but later that afternoon, Business Wire pulled the bid announcement, raising questions about the legitimacy of Apex’s offer.

Lucky for you, we were able to secure a screenshot of the supposed bid, and it is certainly… interesting. Here’s the full release from Business Wire:

To highlight some of the more interesting points from this “proposal”:

First, Apex submitted an all-cash offer of up to $43 billion (!!!), which is 54% higher than Paramount’s $28 billion enterprise value in the Skydance deal. Specifically, Apex offered $35.03 and $23.28 per share for Paramount’s Class A and B shares, 52% and 55% higher than Skydance’s offers, as well as infusing $10 billion to Paramount’s balance sheet (vs the $1.5 billion from Skydance).

Why is Apex willing to upsize Skydance’s offer by $15 billion?

“We are confident in the expertise of the investment firm and their willingness to move expeditiously and efficiently to evaluate this offer and submit it to the Special Committee of the Board of Paramount as a proposal that is substantially superior to the Skydance deal,” said Tatiana Logan, General Counsel for Apex Trust. “Paramount and its assets are a national treasure, and we intend to treat them accordingly. Paramount's global future is bright, but it requires resources, which we have and are enthusiastic to deploy, making it a win-win situation for all of Paramount’s stakeholders…”

Apex also committed to infusing approximately $10 Billion into Paramount’s working capital post-closing for purposes of implementing its business plan for Paramount designed to achieve the following strategic goals:

Content creation, acquisition, protection and monetization

Cutting-edge innovation, technology, and AI, including quantum computing

Consumer focus

Global expansion

The hiring of additional team members…

So, this Apex Capital Partners is willing to pay a 50%+ premium, as well as Skydance’s breakup fee, and inject $10 billion to Paramount’s balance sheet to, among other things, help the struggling entertainment company make a push into quantum computing. It’s an ambitious move, if nothing else.

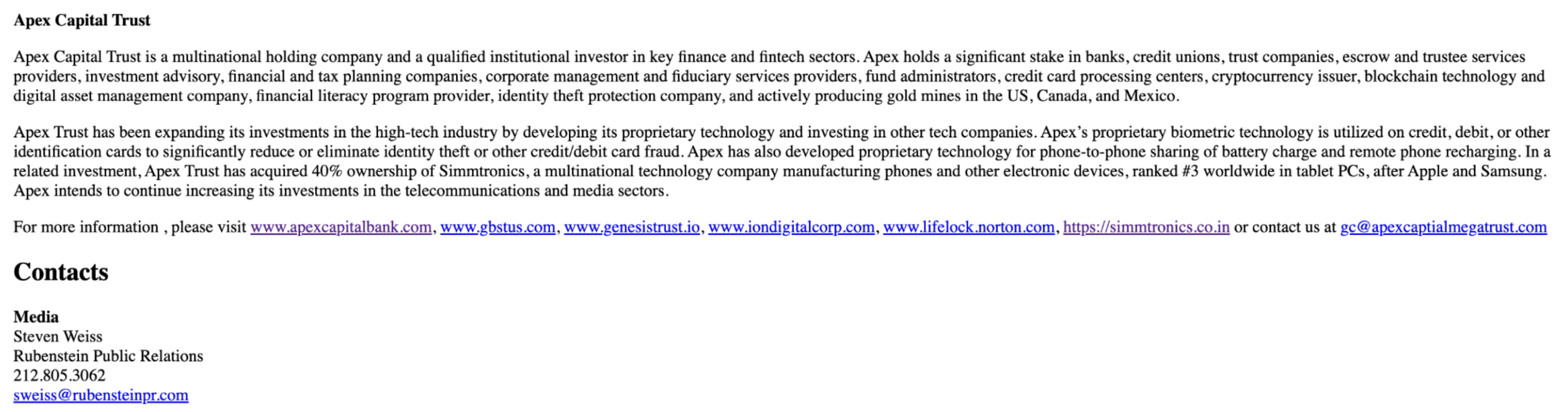

Second, $43 billion is a lot of money, especially for a company that we’ve never heard of. So what, exactly, is Apex? Well, Reuters spoke to Apex’s general counsel, Tatiana Logan (who, according to LinkedIn, took that position in July of this year):

Logan alleged Apex Capital Trust holds multiple subsidiaries, including operating gold mines whose reserves were valued at $256 billion and credit card processing centers that she said had billions of dollars a month in transactions.

"Nobody knows about these companies because they are not consumer facing, but that does not make them less real," Logan said. She declined Reuters’ request for documentation to support her claims about valuation of these subsidiaries and did not provide the location of the businesses…

Logan declined to identify the individual or individuals behind the Apex Capital Trust Transaction or if it had partners, saying, “our owners want to be able to go to Whole Foods, pick up children and pick up their grandkids” without being recognized.

Third, Apex Capital Bank’s website, linked at the bottom of the press release, is bare bones. It’s basically a WordPress site with a few stock images of people sitting in front of computers, as well as bulleted lists detailing the company’s services, such as checking, savings, private wealth, and private client. Apex Capital Bank also claims to be a “sovereign bank” that charges customers a “one-time fee of $350,” but it declines to say what that fee is for. You also can’t click anything on the website except for a contact form. However, Logan’s explanation for this is that “the website was created for the bank recently as part of Apex Capital Trust’s desire to make its offer public.” Basically, the website isn’t relevant to the company’s business.

Fourth, Apex claimed to own 40% of Indian electronics manufacturer Simmtronics, “a multinational technology company manufacturing phones and other electronic devices, ranked #3 worldwide in tablet PCs, after Apple and Samsung.” While it appears that Simmtronics did sell a tablet called the “XPad” in 2013 and 2014, it’s no longer available on Amazon or Indian e-commerce site Flipkart, and it certainly isn’t “#3 worldwide in tablet PCs.”

My intuition suggests that there’s just no way this is real, but Reuters reached out to Steven Weiss of Rubenstein Public Relations (a legitimate communications agency), whose contact information was included at the bottom of the Business Wire piece, and he confirmed via email that, “Yes, this is real,” and Logan said that Apex was willing to place $50 billion in escrow to show that it has the means to complete the transaction.

The most likely outcome is that this is, in fact, an illegitimate offer. However, there is a non-zero chance that a shadow entity named “Apex Capital Partners,” which operates credit card processing centers and mines with more gold reserves than Switzerland and Germany combined and has a “sovereign bank” with a broken website, actually decided to make a $43 billion offer for a debt-saddled entertainment company. And if Apex were to deposit $50 billion in escrow to prove it had the capital, it would be hard for Shari Redstone to turn down the $15 billion increase, no? To be clear, I don’t think any of this will happen, and it’s probably vaguely tied to a crypto project, but I do hope the entire thing is legit.