People are smoking more weed than ever, so why have pot companies been such lousy investments?

Weed stocks are reaching their lowest point, but some think the market can only get higher.

Cannabis stocks reached new lows in 2024 as the regulatory landscape in the US failed to get friendlier and no new states legalized recreational use, despite a general trend consistently pointing toward greater acceptance of marijuana and people overall smoking more pot.

AdvisorShares Pure US Cannabis ETF, the largest weed ETF by market cap, is down over 40% this year. Companies like Tilray and Canopy Growth are each down nearly 40% as well.

“The year was not gentle to US cannabis investors,” analysts at ATB Capital Markets wrote in a December research note.

Weed stocks got a bump after the Department of Justice announced in late April that it would recommend reclassifying marijuana from a Schedule I drug (like heroin and LSD) to a Schedule III drug (like Tylenol and testosterone). But that was about the only bit of good news they got this year, and the process of making that proposal a reality has dragged on.

In November, voters in Florida failed to pass an amendment that would have made recreational marijuana legal in the country’s third-most-populous state. While over 55% of the state voted in favor, Florida requires a 60% majority to ratify new amendments. The industry expected that amendment to be adopted and had their balance sheets geared toward growth to prepare to enter a new market, said Morgan Paxhia, managing director of Poseidon Investment Management, a cannabis hedge fund.

“That left a lot of investors thinking, ‘Where is growth going to come from?’” he said.

More legal cannabis consumption ≠ more profit for pot companies

Running a legal weed company isn’t easy. Finding banking and capital is difficult because marijuana is still illegal on a federal level. Tax bills are high because unlike most companies, they can’t deduct business expenses. And, while these companies are selling higher volumes, the retail price keeps falling down.

Particularly in more mature markets, the supply of weed has caught up to the amount of retail demand. In Oregon, which legalized recreational pot more than a decade ago, the wholesale price per pound of marijuana went from $1,750 in 2017 to less than $600 in 2023, according to the state’s Liquor and Cannabis Commission. But the retail price for a gram of weed also dropped by about half during that period, keeping the profit margins basically the same.

Legal weed companies also have to compete with the illicit market and new hemp-derived products like Delta-9, which offers a similar high and operates in a legal gray area. Those competitors don’t face the same costs that come with being a compliant weed business.

Under those pressures, few cannabis companies are consistently profitable and most are heavily in debt. Many have not made it through 2024 scot-free. MedMen filed for bankruptcy in April. Several others — including StateHouse, Herbl, Blue Arrow, and RevClinics — have gone into receivership.

Paxhia said the industry expects more bankruptcies and defaults before the regulatory landscape gets friendlier. “It’s a survivor’s game for sure right now,” Paxhia said.

If you hit rock bottom, the only way to go is up. Right?

There are some glimmers of optimism that don’t appear to be priced in at the moment.

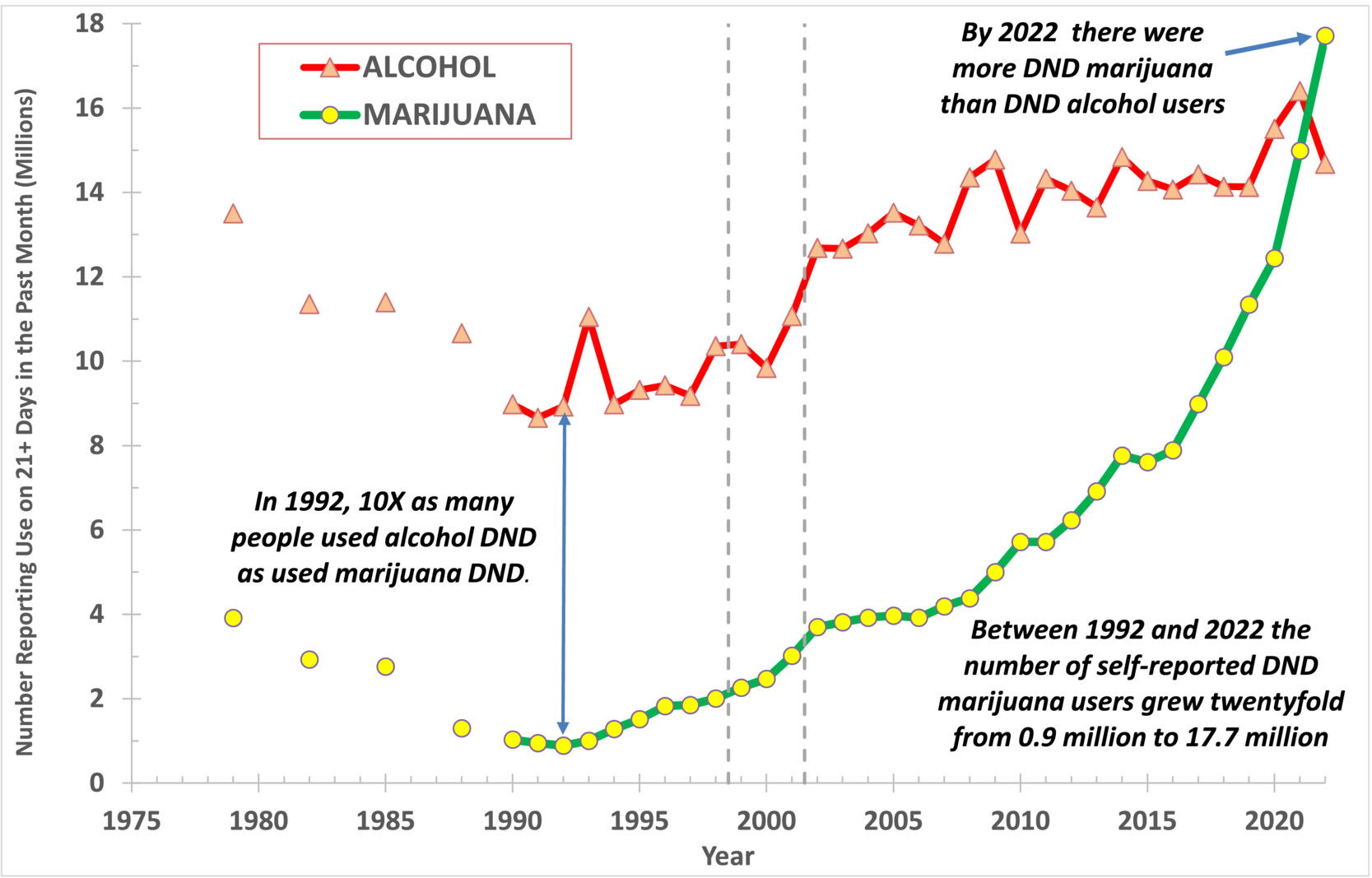

First, as far as consumer trends go, marijuana is better positioned in the long term than traditional booze companies. According to the US National Survey on Drug Use and Health, as of 2022, more people reported using cannabis on a daily or near-daily basis than alcohol.

Both ATB Capital Markets and Paxhia think the weed bears may be overpricing bad news.

“The market is aggressively overweighting near-term regulatory setbacks and underweighting the long-term trend of an industry that will (maybe slowly but surely) march towards full legalization,” ATB wrote.

A few things may happen in the next year that could trigger a price surge:

The federal government may finalize its rescheduling of marijuana.

Pennsylvania lawmakers are again attempting to legalize marijuana for recreational use, adding another market.

The incoming administration brings uncertainty, which some see as more promising than the stalemate under the current administration.

In a recent interview with The Dales Report, Canopy Growth CEO David Klein gave his pitch for cannabis stocks, including his company:

“If you are an investor — and I appreciate the frustration, trust me, I very much share it myself — if you believed in investing in the industry and in Canopy in 2017 and 2018, you should love the ability to invest in it today where you now have a clean business, a clean balance sheet, a solid operating environment, with a strong foothold in the markets that matter, and a beat-up stock. This is the opportunity time.”

In his view, weed stocks are cheap and the fundamentals are there they’re just missing something to spark the fire, so to speak.