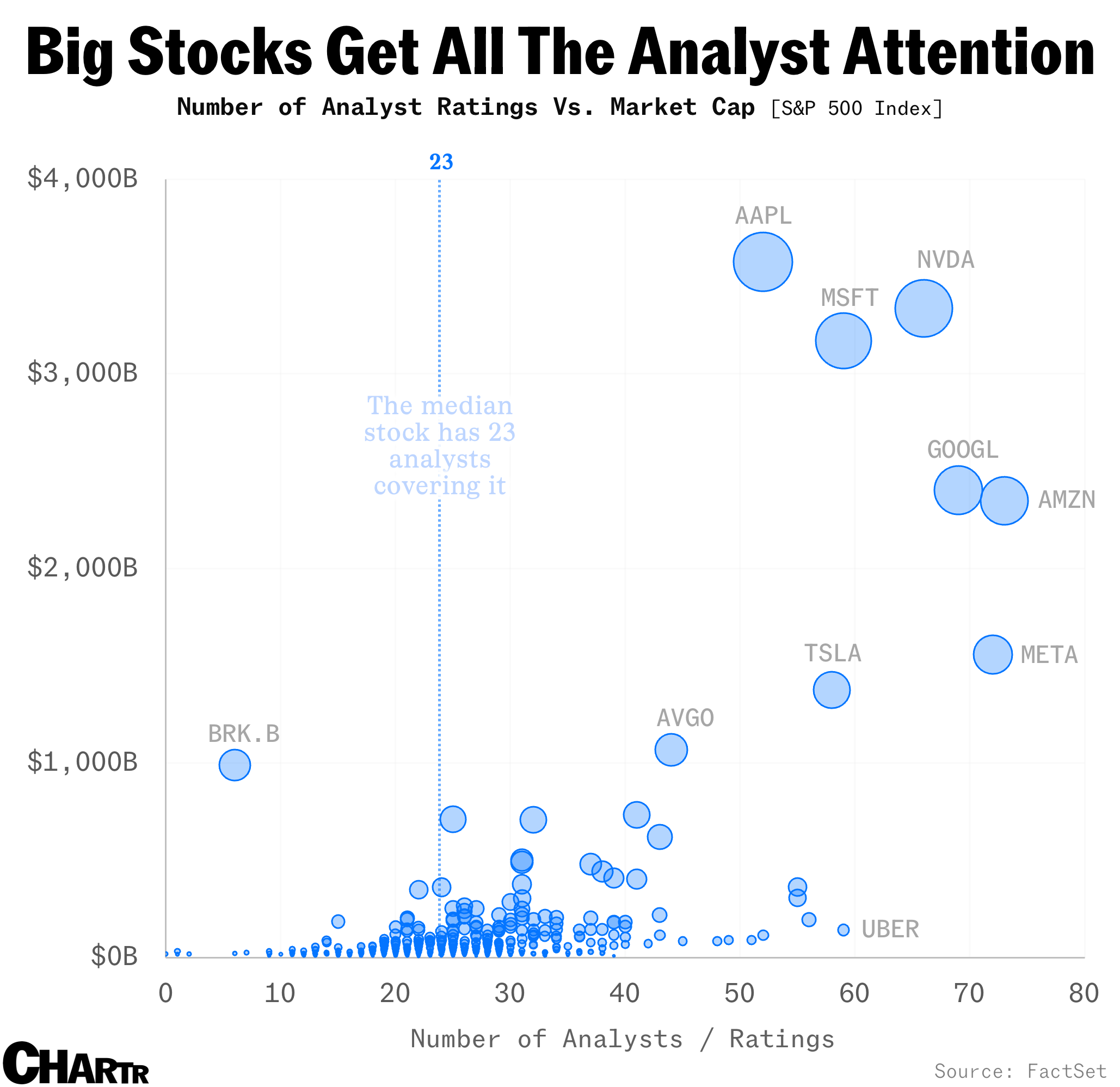

73 Wall Street analysts cover Amazon, there are 72 on Meta, and 66 write about Nvidia — how many do we need?

Most of them have the same opinion, by the way (that you should buy those stocks).

In the 1990s, one of the most highly sought after jobs on Wall Street was stock research analyst.

Crunching some numbers, chatting to a few experts in the industry, and then writing (typically bullish) reports about stocks, in the hope that your insights would encourage investors or companies to do business with the financial institution you were employed by, was a great gig. The pay could be sky-high — some analysts made upward of $15 million a year in the glory days, per Bloomberg — and the CEOs of the companies in your remit wanted to talk to you. Crucially, analysts don’t personally have any skin in the game. Told everyone to buy a stock and it whiffed on earnings? You might lose face, and maybe some clients don’t take your calls, but you won’t lose any money. Onto the next one.

However, by the time I wandered wide-eyed into an investment bank’s research division in 2014 as an intern, the game had changed. By then, regulation quite rightly required a strict firewall between research and banking, blunting the conflict of interest between the two — and turning off the money hose for star analysts at big banks. Furthermore, as trading margins were squeezed, regulation tightened in Europe (MiFID II), AI emerged, and passive investing scooped up assets at breakneck speed, the headcount at research departments shrunk. As written in this great Bloomberg piece, published on January 8:

“Compared with their post-financial crisis peak, it’s estimated that the biggest banks globally have slashed the ranks of equity analysts by over 30% to lows not seen in at least a decade. Those who remain often cover twice, or even three times, as many companies.”

So, equity research has shrunk, and yet we still have 73 analysts — the highest number of any stock in the S&P 500, per FactSet data — all publishing price targets, building financial models in Excel, and writing reports about Amazon. How did that happen?

One explanation is that we have fewer analysts covering more companies in less depth. Another is that data aggregators like FactSet are collating more estimates and ratings from outside of the traditional 15 to 20 largest banks, including people working for boutique research houses, their own independent consulting companies, or smaller brokerages. Just 10 years ago, there were only 46 analysts covering Amazon.

But the simplest reason is that, due to Amazon’s sheer size and complexity, the $2.3 trillion behemoth is drawing the collective brainpower of both buy-side and sell-side analysts into its orbit. If you’re a fund manager, you need to understand Amazon and the rest of Big Tech because they make up more than one-third of the entire S&P 500 Index. And, if you’re an analyst who wants to make a name for themselves, it’s a lot easier to do so writing about stocks like Amazon, Meta, or Nvidia. While it’s an obvious correlation, it’s no less true: big stocks tend to get more attention.

Now that we have stocks that are bigger than ever before, with eight companies over the $1 trillion market-cap threshold, it follows that analyst coverage remains incredibly concentrated on those names.

Indeed, Big Tech equities are the serious outliers, with their 50-plus analysts. The typical stock in the S&P 500 Index has just 23 analysts maintaining recommendations and forecasts on it, per FactSet data. Another outlier, Berkshire Hathaway, has just six analysts, because as a conglomerate, buying Berkshire Hathaway is really like buying a portfolio of other stocks and companies, plus a boatload of cash. (See: “So you invested in Berkshire Hathaway: What did you buy?”)

With 73 eyeballs on Amazon stock, and this many people analyzing the same amount of information, surely we should end up with a wonderful diversity of opinions? That, however, is not the case.

Of the 73 who cover Amazon, a whopping 69 — or some 95% — of them have positive recommendations on the stock, i.e. that you should buy (or be “overweight,” relative to a benchmark portfolio) the security. Out of the remaining analysts, three have a neutral view, and just one has an outright “sell” recommendation. The story isn’t that different for the rest of the BATMMAAN stocks either, Tesla aside.

Indeed, it turns out that a majority of the experts tend to subscribe to one overarching idea: that the eight Big Tech stocks, which drove so much of the market’s return last year, will (mostly) keep crushing it in 2025.

According to FactSet data, 95% of analysts covering Microsoft and Amazon, respectively, offer positive ratings for the two stocks — marking the companies with “overweight” or “buy” ratings — while 92% give the same judgement on Nvidia and 86% say the same for Broadcom. Meta has two analysts with “sell” ratings, Apple has four, and Tesla has a whopping 14, which is perhaps a reflection of the stock’s growing disconnect with the company’s fundamentals — a fact that some analysts think just doesn’t matter.

Why do we get this herding effect? I’ll summarize a few potential reasons that have been posited over the years, none of which are particularly satisfactory on their own.

The analysts are stupid.

There’s certainly some truth to this some of the time (I have had many ideas about markets that have been very, very wrong), but it’s not a compelling argument in aggregate.

The analysts are smart.

Stocks usually go up. Ergo, if you were an alien who knew nothing else about markets and you got a job at fictional bank Citi Morgan Sachs as an analyst, your default recommendation would probably be: buy.

It’s in our nature to herd.

Study after study shows that we humans find it very hard to come up with original ideas when everyone has the same opinion or views things the same way. See: conformity experiments.

It’s in our nature to fear embarrassment.

Being loud and right is great work if you can get it — but being loud and wrong, when everyone else was saying the opposite, is a gamble many are not willing to take. Even if you have a different view, voicing it loudly can feel risky.

It’s not in the financial interests of the company that pays them.

This one stretches the practical limit of our regulations. By the letter of the law, banking and research departments shouldn’t know what the other one is working on anymore. However, research analysts know how their bread is buttered — if they have a huge red SELL sign hanging on a stock, it makes the jobs of their rainmaking banker colleagues trickier. Saying to the CEO of a company, “Hey, you should let us advise you on that huge merger you’re doing for fat fees,” is an uncomfortable pitch to make when someone else at your bank is saying that the company’s stock is about to tank.

The companies they cover will be mad at them.

Related to the one above, after you tell everyone you hate the stock, don’t expect the CEO to swan into your conference and shake your hand. In rare cases they will even threaten, or take, legal action. Some analysts build reputations on things as straightforward as corporate access (throwing great conferences, giving “market color” after an analyst breakfast, and simply being experts on the mechanics of the businesses they cover), which can be threatened by pissing off the companies they cover.

Throw all of those biases into a blender — and I’m sure many others that I’ve missed — and what do we get? We get 73 experts with an opinion on Amazon’s stock, 69 of which say: buy.