Technology giants don’t look like they used to, as the asset-light era fades

Oracle and Meta are now some of the most capital-intensive businesses in the S&P 500, spending more than energy giants. I guess data really is the new oil?

Spin up a website; throw a few bucks at a server; buy some Facebook ads; get a million downloads for your app; and then kick back and enjoy the fruits of the super-lean business model. The economics of tech have been alluring for decades, in part because they haven’t required huge swaths of investment.

As the viral posts on social media might tell you: Airbnb owns no hotels, Uber doesn’t have any cars (still true-ish), and DoorDash doesn’t have ovens to make a pizza or woks to whip up a pad thai. Spend a little to make a lot.

AI throws all of that into question, as the power-guzzling, water-wanting data centers sucking up every spare investment dollar and watt of electricity change everything from how we work to how we connect.

Software ate the world. It’s still hungry.

So, Marc Andreessen was right: software did indeed eat the world. But our appetite for AI-enhanced software is expected to be so voracious that we’re building data centers the size of cities to keep up with the compute demands.

Indeed, Big Tech’s AI infrastructure build-out is so enormous that some of America’s most valuable tech companies, like Oracle and Meta, now screen more like energy companies.

Here’s a list of the most capital-intensive companies in the S&P 500 Index, ranked by Wall Street’s estimates for their sales divided by their capital expenditures (both over the next 12 months). Can you spot the odd ones out?

Oracle is the most startling name here, with Wall Street anticipating that the company will spend $56 on capex for every $100 it makes in revenue over the next 12 months, as it looks to the debt markets to fund its remarkable binge. That splurge is all in the interests of delivering on its end of an eye-watering contract with OpenAI, worth $300 billion to Oracle over the next five years.

OpenAI, which — for now — remains a private company, would be completely off the deep end of the above table, considering that it’s signed something north of $1 trillion worth of infrastructure deals.

Meta isn’t far behind Oracle, with Wall Street anticipating that $45 out of every $100 that comes through its doors will be spent on chips, servers, data centers, and more. Interestingly, this afternoon, news broke that Meta was looking at cutting back some of its spending on the metaverse and virtual reality — investors loved it and the stock leaped higher. But did they love it because it means less spending overall, or more cash freed up for AI capex?

Even the firms categorized as real estate companies on the above list, Digital Realty and Equinix, are in the data center business. That means that of the top 25 most capital-intensive businesses in the S&P 500, 100% of them are either utilities or are focused on building out data centers.

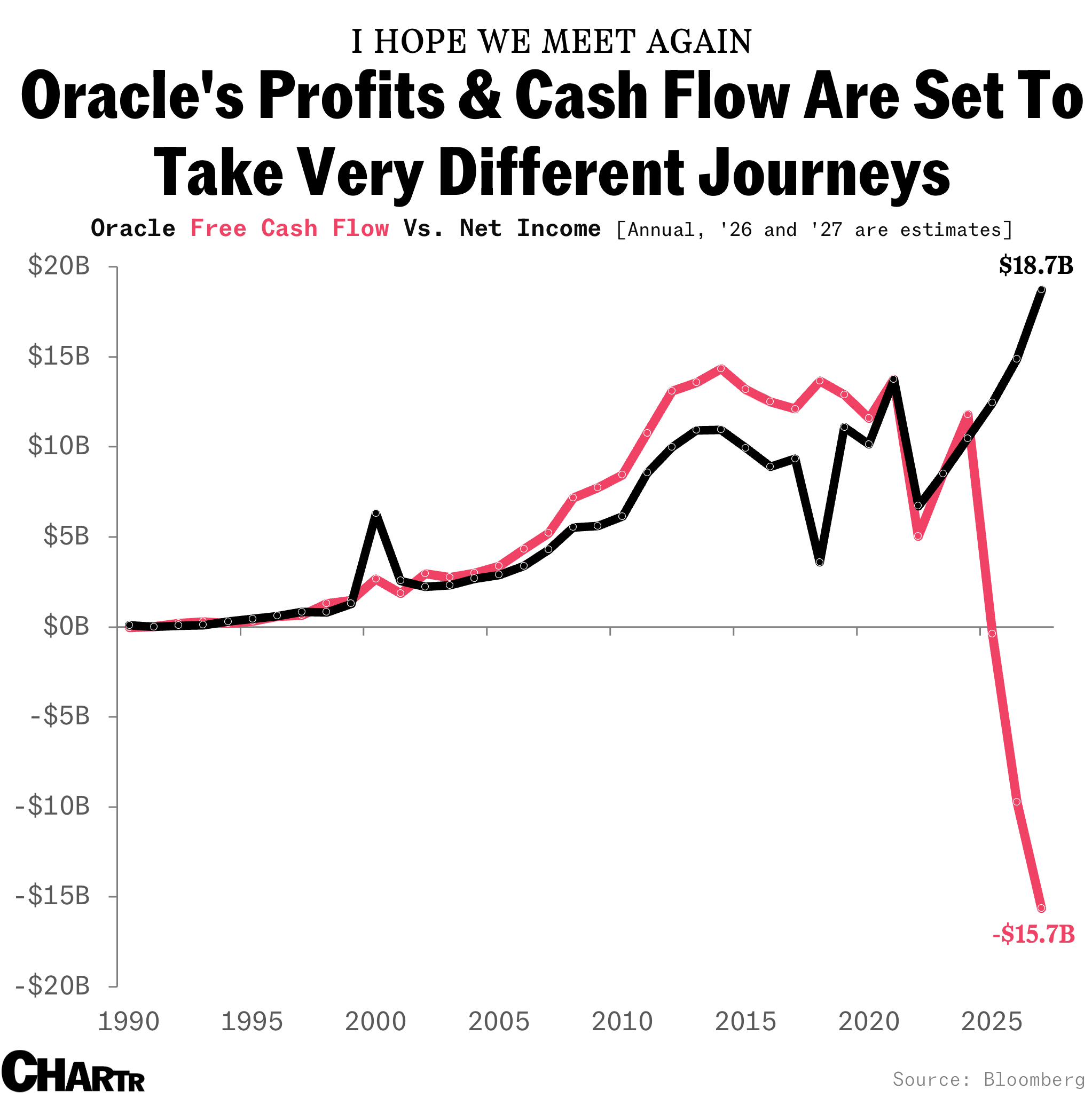

Meanwhile, Wall Street thinks Oracle is going to have a wildly profitable year in 2027, making more than $18 billion in profit — but it’s going to end the year with nearly $16 billion less cash than it started with. No wonder some investors are getting jittery about its debt.

To be clear, none of these accounting distortions are illegal. Or even remotely shady. Free cash flow and net income routinely diverge. What’s so eye-catching about this is simply the scale.

When Meta spends $1 million on Nvidia chips, the company books that as a capital expenditure. It doesn’t directly affect Meta’s bottom line until the next accounting period, when bookkeepers start to reduce the asset’s value through depreciation for however many years they think those chips will be useful. Nvidia, however, doesn’t have to wait; it gets to book the $1 million as revenue straight away. So rampant capex spending actually boosts earnings in aggregate — in the short term, at least.

The tune being sung by the bears of Wall Street — with Michael Burry of “The Big Short” fame arguably their loudest voice — is that the useful lifespan of these chips is being overestimated. That means that when the depreciation really kicks in next year and the year after, it’s going to be underestimating the true economic cost.

There is a decent haul of early evidence to suggest there may still be life in an AI chip after a few years, with analysts at Bernstein, led by Stacy A. Rasgon, Ph.D., writing in a note from November that “GPUs can profitably run for ~6 years, and that the depreciation accounting of most major hyperscalers is reasonable.”

However, as Sherwood News Markets Editor Luke Kawa notes, Nvidia’s Blackwell chip ramp-up was delayed because of heating issues — which could impact longevity. We just won’t know for certain for a while.

Either way, Wall Street is penciling in for costs to rise: estimates for depreciation expenses for America’s nine largest tech giants have all soared.

In absolute terms, a depreciation and amortization bill of $293 billion and change in 2027 is scary. But all of this AI investment is also meant to be driving incremental revenues, which is why it’s mostly meaningless without some context — here are the same nine companies, this time with D&A as a percentage of revenue for each.

Amazon’s D&A as a share of its revenue was just 2% in 2011. By 2028, it’s expected to be 11%. Microsoft, meanwhile, will have seen its rise from 4% to 18% over the same time frame, while Meta’s will hit 15% and Oracle’s will be 14%. These are not the super asset-light business models of the tech era from yesteryear.

Apple, which has dipped its toe in the AI pool rather than diving headfirst, is a notable outlier. As is Tesla, which is spending a fraction of its peers to achieve its self-driving and AI robot ambitions. Critics say this is evidence that it’s not a serious player, but Tesla bulls argue that it only screens low on capex intensity because it has a fleet of cars paid for by its customers doing a lot of the work for it. As Gavin Baker wrote on X in response to Jim Chanos (emphasis ours):

“Yesterday, @RealJimChanos posited that Tesla’s relatively low capex meant that they were not a serious competitor in real world AI and Robotics.

This is *exactly* the wrong way to look at it and the implications of this fact are actually positive for Tesla IMO.

Tesla’s inference definitionally happens in the car so their customers are effectively paying for the inference compute ‘capex,’ which is now probably the majority of hyperscaler capex spend.”

But most remarkable of all are Nvidia and Broadcom. Thanks to soaring sales and substantial investments in previous years, both companies see their D&A drop substantially as a share of their revenue. Nvidia’s is actually set to be close to ~1% by 2028, a fraction of its BATMMAAN peers.

Of course, asset-heavy business models aren’t necessarily bad — and investing up front isn’t a stupid idea. As we’ve written before, the stock market is littered with tech companies that the media made fun of because they lost money for a long time.

We’ve just never seen anything even close to this scale before.