War and AI doubts have fueled an unprecedented divergence between stock prices and earnings estimates

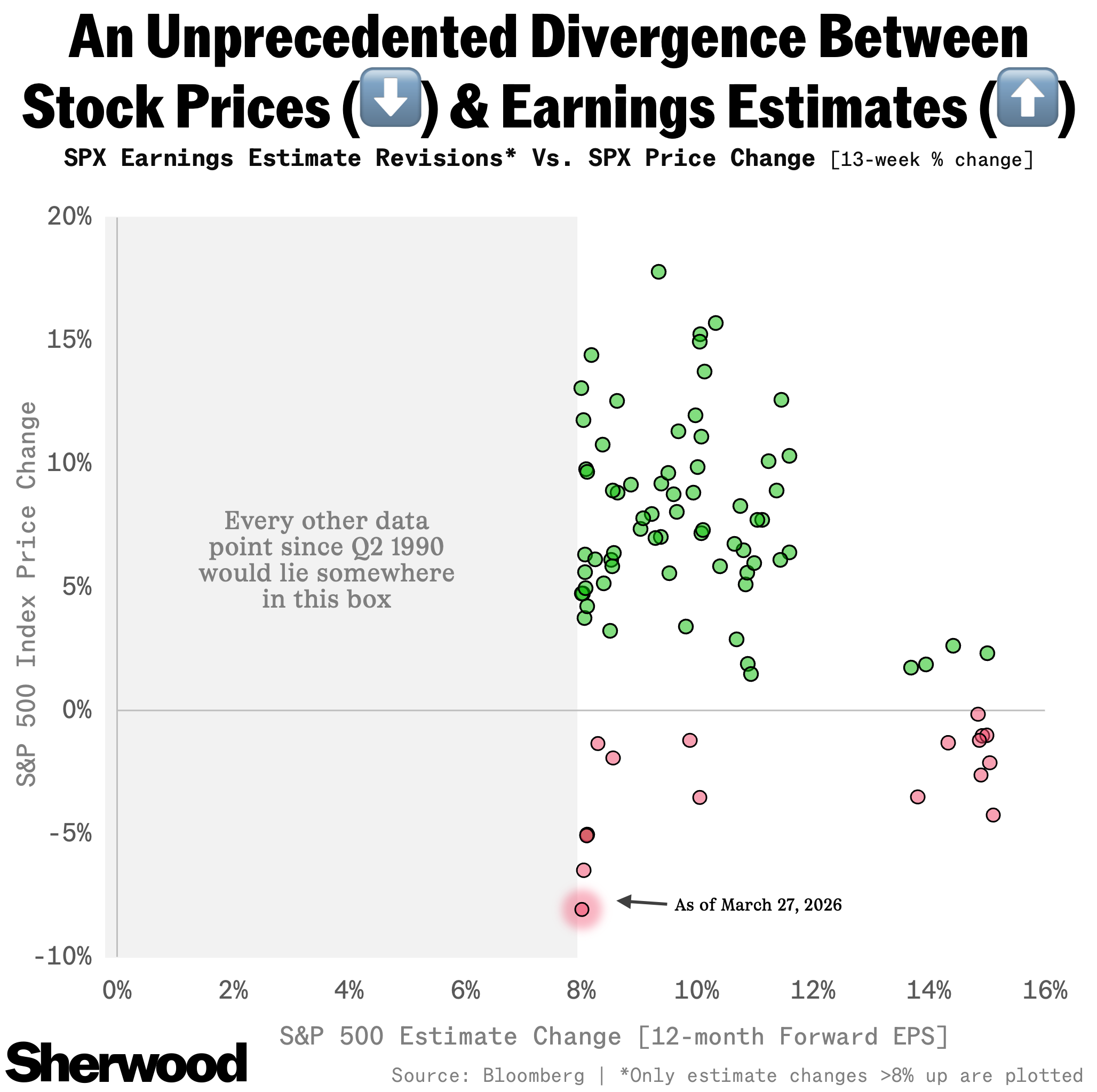

The S&P 500 has never been down this much when earnings estimates have risen by this much, based on data going back to Q2 1990.

Over the long term, earnings drive stock prices.

But in the here and now, we’re experiencing an unprecedented divergence between the S&P 500’s earnings estimates and the performance of the benchmark US stock index, driven by skittishness about the return of oil shipments through the Strait of Hormuz and the long-term ROI for the hundreds of billions in AI capex.

Over the three months ended March 27, analysts have ratcheted up their projected bottom-line results for the largest US publicly traded companies by 8%. Over the same time, those stocks are down 8%. Stocks have never been down this much when earnings estimates have risen by this much, based on data going back to Q2 1990.

The closest such episodes to the present environment were in mid-2010 amid fears of a double-dip recession following the financial crisis, and in 2018 following a short-lived blowup in volatility markets.

For what it’s worth, every S&P 500 downturn of at least 14% from a bull market high since the financial crisis has only bottomed after forward earnings estimates start to come under the knife.

Oil price spike not recession fuel (yet)

The world in which these earnings estimates are realized is incompatible with a long-lived oil disruption that sparks a US economic downturn. Oil price spikes are infamously a drag on other parts of consumers’ spending; accordingly, durables and household personal products are the worst two industry groups in the S&P 500 since the end of February.

But as a general matter, markets do not appear to be pricing in elevated recession risk. For all the conniptions in private credit, public high-yield credit isn’t screaming. Spreads in US junk bonds (excluding energy!) are still below their average level since the start of 2015.

Heck, even the oil markets haven’t shown the same degree of alarm (even at the front end!) despite a more meaningful supply shock than what followed Russia’s invasion of Ukraine. Stock markets have the luxury of being more forward-looking than commodity markets, because commodity markets must clear in spot: oil has to be delivered to a certain place at a certain time at this agreed-upon price. WTI oil futures for delivery in May have to reflect supply/demand dynamics in May, not a rose-colored view of a future where we’ve gone from conflict to kumbaya. That’s the danger associated with imagining $150-per-barrel oil to be as unlikely and impractical as 150% tariffs on Chinese imports.

Megacaps, Megapain

Of course, this unprecedented divergence between earnings (higher) and stocks (lower) is over three months; the war has only been going on for one. The unwillingness to buy into megacap AI stocks — especially hyperscalers, but also Nvidia — despite rising earnings estimates predates the Mideast conflict. Risk-off sentiment has weighed on stocks generally, but the Magnificent 7 have lagged since the attacks commenced.

For some time now, investors have been of the view that 2026 earnings don’t really matter for the hyperscalers and have more creeping doubts on whether this capex binge will prove worth it in the long run — or whether the most meaningful impact on these companies will be the destruction of their free cash flow generation amid these aggressive build-outs. And Nvidia’s fate has been tied to the perception of its biggest customers.

The war started off as a major rotation trade. Three major trades that had been tumbling — software vs. semiconductors, US stocks vs. the rest of world, and the Magnificent 7 vs. S&P 500 equal weight — all enjoyed some nascent reversals in the early days of the war. Of those three, Mag 7 versus equal weight is the only one that’s given up all of that rebound and then some.

No Trump card?

In some respects, the current market situation is similar to 2025. The Q1 peak in stocks came when Walmart, a major component in momentum indexes, issued a poor full-year outlook and once high-flying stocks got clobbered. It started as a momentum-centric rather than tariff-centric sell-off.

This time around, the difference is that many parts of the AI trade (especially the megacaps) didn’t have any momentum coming into this. A theme that investors had already been souring on is continuing to unwind.

“Trump Always Chickens Out” (or TACO) is a popular explanation for why markets haven’t reacted more negatively to the prospect of significant negative economic impacts from this oil supply shock.

It’s also worth remembering that a game of chicken involves two sides barreling toward each other at high speed, and that the chicken only ducks conflict when presented with imminent, catastrophic loss.

Both investors (and the president) have been increasingly conditioned to react late when faced with (or bringing forward) negative market catalysts.

And President Trump isn’t the only party with a vote on this matter. While he can change his mind on how much military action in the Middle East is appropriate as the facts on the ground (and market conditions) evolve, that doesn’t mean leaders in Iran (or Israel) will be moving in lockstep.

None of the market fundamentals, the most impacted asset, or the stock market price action have caused a white-knuckle moment just yet.