What does the Fed have to do with the bounce in momentum stocks? Absolutely nothing.

The performance of momentum-linked names has been rate agnostic.

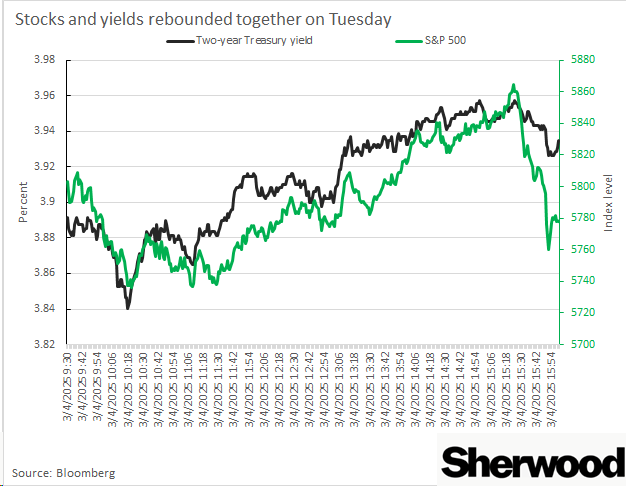

Here’s the first problem with trying to draw any link between the bounce in stocks off the lows on Tuesday and the market’s pricing of Federal Reserve policy: stocks and short-term bond yields traveled in the same direction, nearly all day!

The point in time when the market was pricing in the most easing was also the point in time when the stock market was the lowest. The point in time when the stock market was the highest was when yields were also the highest. It’s simply not cogent to suggest that cut odds going up were a factor behind stocks recovering when the amount of Fed easing priced in was going down the entire time stocks were rebounding.

This dynamic — stocks and bonds being negatively correlated (or stocks and yields being positively correlated, if you prefer) — has been a prominent feature of the investment backdrop over the past month. It’s another way of saying the “good news (about the economy) is good news (for the stock market),” and vice versa. This relationship is also an indication that investors are more worried at present about downside risks to growth than upside risks to inflation.

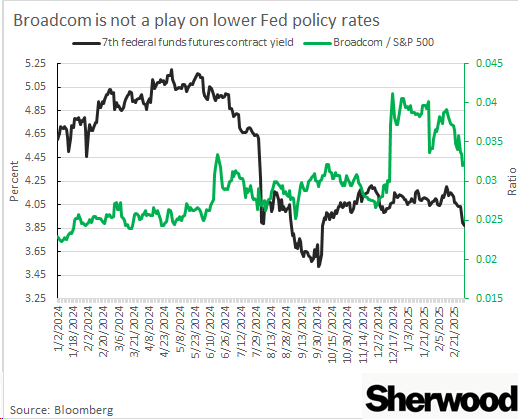

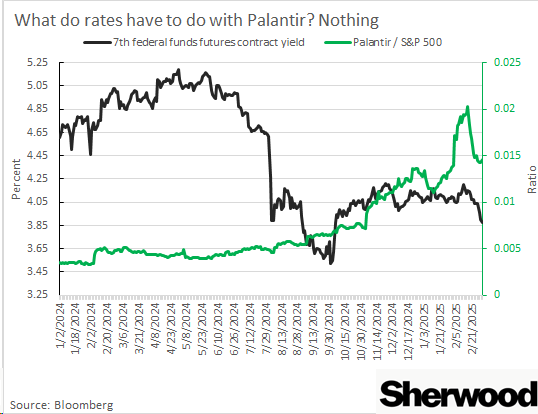

Let’s zoom in on Broadcom and Palantir, a couple stocks highlighted as “great performers over the last year when the market was pricing in and absorbing rate cuts from the Federal Reserve.”

A not-even-that-close examination of the performance of these stocks during the AI boom shows that their relative returns have been rate agnostic, to be charitable.

Broadcom substantially outperformed the S&P 500 in the first half of 2024, a period of time when traders were pricing in less, not more, easing from the Federal Reserve over the following six months. Then, from mid-June through the end of September, expectations for where the policy rate would be in about six months’ time fell a whopping 150 basis points. The chip designer underperformed the S&P 500 during this stretch. Broadcom has also been substantially lagging the market since mid-February of this year, a period during which expectations for where the Fed’s policy rate would be in about six months’ time have gone down by about 40 basis points.

It’s also not too hard to make the case for why Broadcom’s revenue growth isn’t too sensitive to the rate outlook. We know that the so-called hyperscalers loading up on advanced chips are cash-rich. By and large, this capex binge is not being funded by debt; it’s being funded by the incredible cash-generating machines attached to megacap tech companies.

For Palantir, it’s a similar but different story. Palantir has outperformed with rates going down a lot. It’s also outperformed with rates going up a lot. It’s even outperformed with rates going sideways! But again, the most recent stretch during which rates have been dropping sharply has been a period of massive underperformance for the AI defense software company.

Long story short, the notion that the outperformance of these companies is a Fed- and rate-driven phenomenon is devoid of any supporting evidence. Otherwise, these stocks should have been crushing it since mid-February, and they’ve been doing the precise opposite.

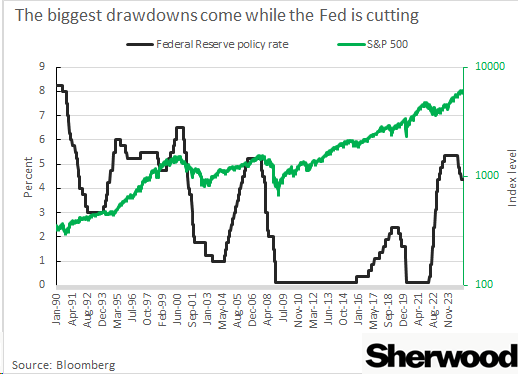

As for the idea that “don’t fight the Fed” is some kind of first commandment of the stock market, that’s certainly not something we would say. Every big market drawdown in my lifetime except for one (2022’s generationally high inflation) has come during a period when the Federal Reserve is aggressively cutting interest rates.

When the Fed is frantically fighting to revive a downturn in economic activity — and losing that battle! — is precisely when investors suffer the most pain.