Hey Snackers,

Turkey season is back, but zooming out, it looks like consumers have been falling out of love with the big bird for decades. Since its 1996 peak, turkey consumption has dropped 25%, while chicken, pork, and beef now dominate Americans’ protein choices. Ironically, despite shrinking appetites for turkey, the birds themselves have kept growing, with today’s supersized turkey weighing nearly double what it did in 1960. We charted America’s long, slow breakup with turkey.

The S&P 500, Nasdaq 100, and Russell 2000 all climbed higher despite Nvidia being one of the index’s worst performers. Energy was the worst-performing sector ETF, as oil prices fell on news of a possible Ukraine-Russia peace deal. The AI trade bifurcated today for reasons we’ll get into below.

Google jumps, Nvidia and AMD fall on report that it’s in talks to sell “billions of dollars” of its custom AI chips to Meta

Google rose yesterday while Nvidia and Advanced Micro Devices dropped upon the revelation that the search giant may be muscling in on the chip designers’ turf.

Per the report, Meta is in discussions with Google to spend “billions of dollars” to use its AI chips in the social media company’s data centers starting in 2027, and to begin renting access to Google chips from its cloud business next year.

Google’s AI chips — TPUs, or tensor processing units — are having a moment. These semiconductors were used to train its latest GenAI model, Gemini 3, which has received rave reviews, and are cheaper to use than Nvidia’s offerings.

Google has also aimed to make its JAX software easier for developers over time by making its TPUs operable via open-source software tied to PyTorch (invented by Meta), overhauling how errors are reported and introducing an extension that makes it easier to write custom code, among others.

Historically, Google has rented access to these chips through its cloud business rather than supplied them directly to third parties. The report suggests that insiders think a more direct foray could allow the company to grab a market share in chips amounting to about 10% of Nvidia’s annual revenue.

According to The Information, Meta is even mulling using TPUs for training, considered a much more demanding task, rather than just inference alone.

Shares of Nvidia dropped, and AMD, which sells GPUs for use in data centers, fell 4%. Broadcom, the custom chip specialist that partnered with Google to design these TPUs, finished up 2%.

The Takeaway

During Nvidia’s conference call last week, CEO Jensen Huang was asked about the competitive threat posed by custom chips. He responded by talking up the difficulty of inference (“How could thinking be easy?”). That’s a not-too-subtle nod to the idea that his company’s GPUs will be the more effective solution compared to more cost-effective options.

Wall Street Wants In on Private Investing. You Can Get In, Too.

Kevin O’Leary is a paid spokesperson for StartEngine. See his 17(b) disclosure, here.

Charles Schwab and Morgan Stanley made headlines with their recent private market acquisitions.

Why? Everyday investors are demanding access to the private markets, and the old guard doesn’t want to be left behind.

StartEngine has been building that access for years.

This leading alternative investment platform provides a comprehensive gateway into private markets, including exposure to dynamic, pre-IPO offerings1 from companies like Kraken, Perplexity, and Stripe.2

These offerings have attracted strong investor interest — and record financials. StartEngine became profitable in H1 2025 with $4.9M GAAP ($11.9M adjusted EBITDA).3 After reaching $48M in annual revenue for 2024, they posted $70M revenue in the first half of 2025, up 3x YoY.4

Now, as Wall Street pays up to join the party, you can learn more about investing in StartEngine directly and own a piece of the platform with a track record of unlocking pre-IPO offerings.5

What will happen if bitcoin and ethereum hit key liquidation levels

Since October, bitcoin has ranged from above $126,000 to as low as $80,500, while the price of the second-largest cryptocurrency, ethereum, rose to nearly $4,900 in August before dropping to a low of $2,800 this month. The volatility powered massive wipeouts in leveraged positions, with October 10 taking the crown for the largest liquidation event ever in a 24-hour period.

Liquidations occur when a trading platform’s risk engine forcibly closes a trader’s leveraged position because an asset’s price reaches a certain level and their margin account balance is insufficient to cover the open position. A handful of liquidated positions barely moves the market, but if thousands of positions with similar liquidation prices are closed, the effect on the asset’s market price can be substantial, creating a “cascading effect.”

These levels matter for non-leveraged investors, too. Large liquidation clusters can create abrupt spikes or drops that bleed into spot markets, revealing where crypto prices may snap lower or higher.

Sinking prices also affect spot ETFs — for example, BlackRock’s iShares Bitcoin Trust ETF, which has seen $2.3 billion leave the fund so far in November. And spot ETF outflows can amplify falling prices, too. Citi Research, cited by Bloomberg, found that this feedback loop sees a ~3.4% price drop for every $1 billion pulled out from bitcoin ETFs.

So exactly what happens at different levels and what are those key price points?

We broke it down for both bitcoin and ethereum in the best of times… and the worst of times.

The Takeaway

There have been a lot of comparisons thrown around lately to the last crypto winter, which kicked off with the catastrophic demise of the “algorithmic stablecoin” TerraUSD and entered freefall with the collapse of FTX. But while we’re hearing phrases like “hasn’t seen a price decline like this since 2022” a lot, the space does have some material differences that may help avoid the worst-case scenarios.

In 2022, there were no spot ETFs; now, BlackRock’s IBIT holds more bitcoin than mega-holder Strategy. In 2021, Tesla was one of a very few public companies that held bitcoin on its balance sheet (it still does, for better and probably, in the short term, for worse), and now there’s a whole “pivot to bitcoin” narrative. That’s not to say these diversifications in holders and institutional investment will staunch bitcoin’s (and ethereum’s) bleeding, but the ecosystem is no longer a self-contained crypto-dome. That could also be bad, as Bloomberg’s Matt Levine points out!

The Best Thing We Read Today

Exclusive: Pfizer’s CFO on building a post-Covid future and how it won the fight for Metsera

Sherwood News Business Reporter J. Edward Moreno sat down with Pfizer CFO Dave Denton, who told us how 2025 became a “watershed” moment for the pharmaceutical giant and how its Metsera deal fits into the company’s post-Covid plan. He also discussed how AI can aid drug discovery and why he believes Pfizer’s future growth depends on two key tracks.

Snacks Shots

🦃 NFL: Green Bay at Detroit is shaping up to be the closest matchup on Thanksgiving, with the market* giving Detroit the edge with a 58% chance of victory. Kansas City is favored to beat perennial Thanksgiving contender Dallas with a 62% chance of winning, while the evening game of Cincinnati at Baltimore gives the Ravens a 74% chance of victory over the visitors.

🏈 SNF: The ascendant New England Patriots — who have managed to speedrun their fall and rise — are heavy favorites on Sunday, with a 77% chance of victory.

*Event contracts are offered through Robinhood Derivatives, LLC — probabilities referenced or sourced from KalshiEx LLC or ForecastEx LLC.

Off The Charts

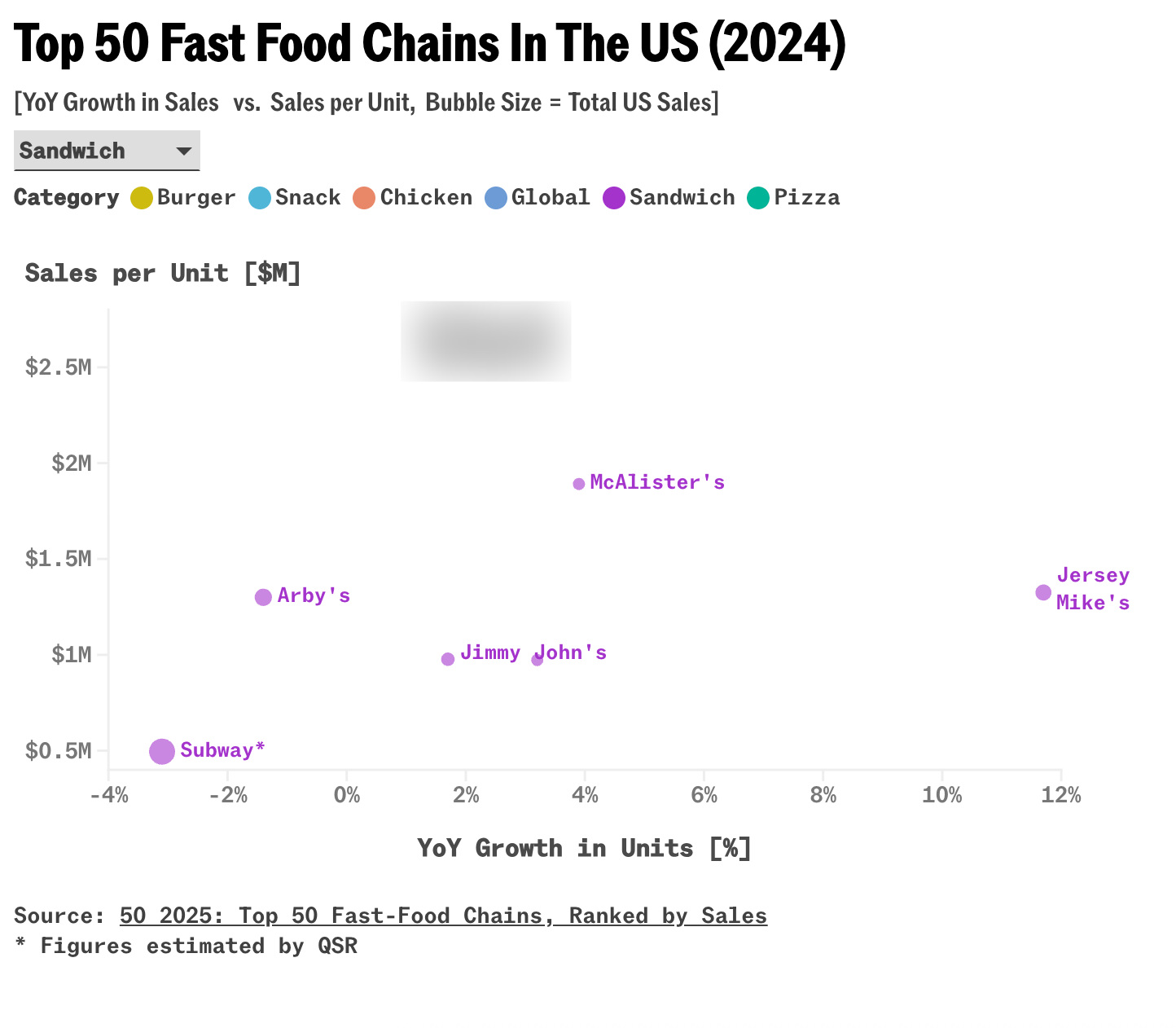

Which sandwich chain last week announced that it would be revamping its menu (starting with lettuce) as revenues have slipped since peaking in 2023?

Target Exposure Across the AI Semiconductor and Quantum Opportunity

The Global X AI Semiconductor & Quantum ETF provides global exposure to companies advancing semiconductor and quantum technologies – the foundation of the next generation of computing.

By capping individual holdings at 10%, CHPX seeks to provide investors with differentiated exposure across both established industry leaders and emerging innovators powering the evolution of AI and high-performance computing.

What Else We're Snackin'

Teens are upset that they can’t speak to Character.AI chatbots anymore

Kohl’s, Abercrombie & Fitch, and Best Buy all reported strong earnings and a very optimistic outlook on this year’s holiday sales

How much it sucks to be close to OpenAI right now, in one chart

Snack Fact Of The Day

Sandisk will join the S&P 500 on November 28, replacing advertising giant Interpublic Group.

This Week's Earnings

Earnings expected from John Deere

1 Any IPO timing is unknown and general steps to be accepted for an IPO have to be undertaken. There is no guarantee that an actual IPO will occur. Some companies may remain private, be acquired, or cease to exist.

2 The companies listed on StartEngine Private are not involved in or endorsing this investment, and have not approved StartEngine Private LLC or its affiliates.

Rather, when you invest through StartEngine Private, you are buying an interest in a separate Series of StartEngine Private LLC, not stock directly in the companies listed. The Series may hold shares directly or through a special-purpose vehicle (SPV). Your interests may differ from the companies’ stock in both rights and value, and there may not be a one-to-one economic parity between the value of Series interests and the underlying shares. The Series also bears its own costs (such as transaction and administrative expenses), which may reduce investor returns.

This offering is made under Regulation D, Rule 506(c), through StartEngine Primary LLC (member FINRA/SIPC), and is available only to accredited investors. These investments are speculative, illiquid, and high risk, and you should be prepared to hold them indefinitely and to bear the risk of losing your entire investment.

StartEngine and its affiliates do not provide financial, investment, legal, or tax advice. This update may include information from third party or public sources that has not been independently verified and may be incomplete or inaccurate. Before investing, review the full offering documents on the offering page and consult your advisors.

3 We define Adjusted EBITDA as net income (loss) calculated in accordance with GAAP adjusted to exclude interest expense, interest income, income taxes, depreciation, and amortization, and stock based compensation. We present Adjusted EBITDA because it is a key measure used by our management team to evaluate our operating performance, generate future operating plans and make strategic decisions. We believe Adjusted EBITDA provides useful information to investors regarding our operational performance and our ability to generate cash flows. Non-GAAP information should be considered as supplemental in nature and is not meant to be considered in isolation or as a substitute for the related financial information prepared in accordance with GAAP. In addition, our non-GAAP financial measures may not be the same as or comparable to similar non-GAAP financial measures presented by other companies.

Please see the tables on page 4 and page 26 of our Q2 2025 10-Q to reconcile net income (loss), the most directly comparable U.S. GAAP measure, to Adjusted EBITDA for the periods presented.

There is no assurance that we will be consistently profitable in the next three years or generate sufficient annual revenues to pay dividends to the holders of our shares. We have not yet generated yearly profits, and may not do so in the near future.

4 Based on our Q2 2025 Form 10-Q/A. This revenue growth has been driven by StartEngine Private, a new product line that offers funds in late stage companies. This product line has driven over $34.1 million of the $39 million in revenue from Q2 2025. To understand the impact on margins, see financials. Past performance may not be indicative of future performance.

See page 4 of the Q2 2025 Form 10-Q for the H1 2025 and H1 2024 total revenues. See page 35 of the offering circular and Management’s Discussion and Analysis of Financial Condition and Results of Operations for 2024 annual revenues.

5 This is a paid advertisement for StartEngine’s Regulation A+ offering. For more information, please see the most recent Offering Circular and Risks related to this offering.

This Reg A+ offering is made available through StartEngine Crowdfunding, Inc. No broker-dealer or intermediary is involved in the offering. In addition, as described in the Offering Circular, the Company retains the right to continue the offering beyond the Termination Date, in its sole discretion.

Investing in private company securities is not suitable for all investors. This investment is highly speculative, illiquid, and involves a high degree of risk, including the possible loss of your entire investment. It should only be considered a long-term investment. There is no guarantee that a market will develop for such securities.